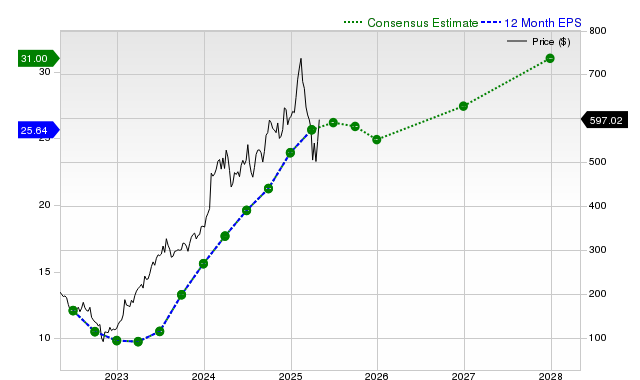

Meta Platforms (META) has recently underperformed the broader market and its industry, yet exhibits robust fundamental strength with significant positive revisions in consensus earnings estimates, including a 12.7% increase for the current quarter and 9.4% for the current fiscal year over the last 30 days. The company also boasts strong revenue growth forecasts and a consistent history of beating estimates. Despite these positive indicators, Meta holds a Zacks Rank #3 (Hold), implying near-term market-in-line performance, and is currently valued at a premium relative to its peers.

Meta Platforms (META) presents a mixed picture, characterized by robust fundamental growth indicators clashing with recent market underperformance and a premium valuation. Over the past month, the stock has declined 2.9%, lagging both the S&P 500 composite and its Internet-Software industry peers. Despite this, sell-side analyst sentiment is improving, with the consensus earnings estimate for the current fiscal year rising 9.4% over the last 30 days to project 17.9% year-over-year growth. This is supported by strong revenue forecasts, with expectations of a 19.1% increase in the current fiscal year and 15.7% in the next. The company has a strong execution track record, having beaten both revenue and EPS consensus estimates for the past four consecutive quarters, including a notable 22.47% EPS surprise in the last report. However, these positive factors are tempered by a Zacks Value Style Score of 'D', indicating the stock is trading at a premium to its peers. This combination of strong fundamentals and high valuation culminates in a Zacks Rank #3 (Hold), suggesting the stock is likely to perform in line with the broader market in the near term.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.35

Ticker Sentiment