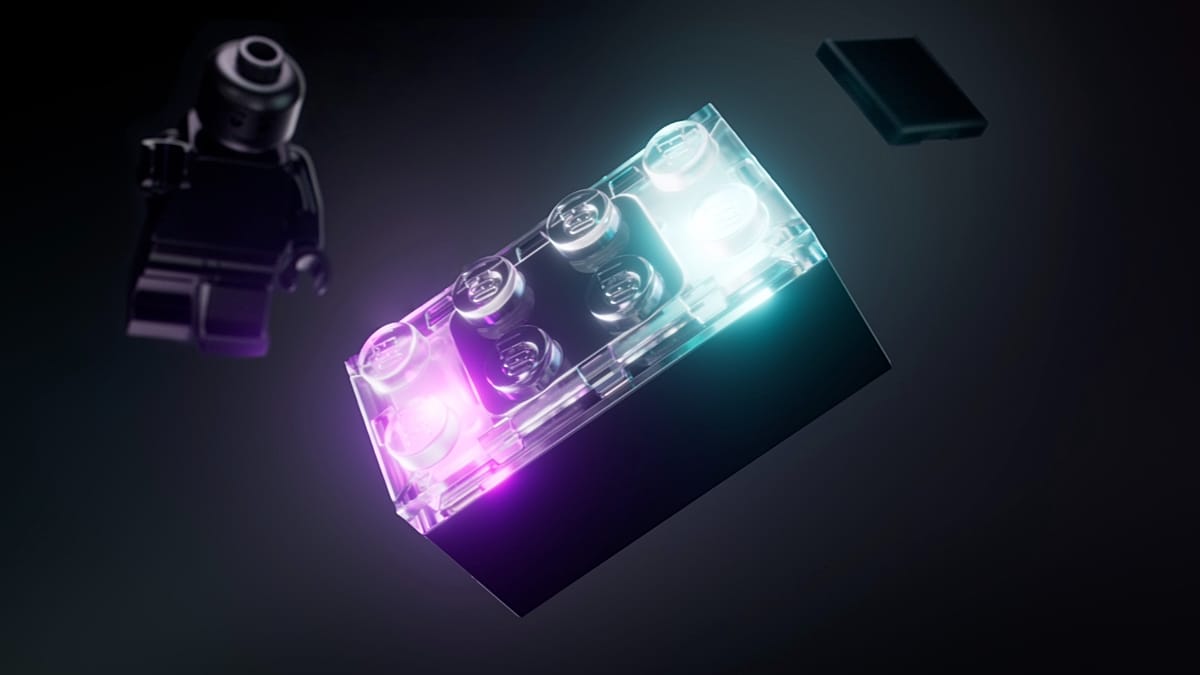

LEGO unveiled a reusable 2x4 "smart brick" at CES 2026 that embeds code to sense color, produce sounds and interact with other bricks and minifigures, and will be charged via a new wireless charger. The first commercial rollout targets the Star Wars line in March, with example SKUs priced at ~€70 for a 473-piece TIE Fighter (one Smart Brick, one Smart Tag) and ~€100 for a 584-piece X‑Wing (one Smart Brick, five Smart Tags, two Smart minifigures). The launch positions LEGO to upsell higher‑priced, tech-enabled sets and boost attach rates and average selling prices while retaining a screen-free play proposition, though it is unlikely to be market-moving for broader equities in the near term.

Market structure: LEGO’s smart-brick rollout (Star Wars sets in March) increases premiumization in the toy category — observed MSRP examples (€70 for 473 pcs, €100 for 584 pcs) imply ~30–50% ASP uplift vs comparable non-smart sets and greater pricing power for branded, IP-rich players. Direct winners: retailers with scale/fulfillment (AMZN, WMT, TGT) and semiconductor/haptics suppliers that service low-power sensing and wireless charging (NXPI, STM). Public toy incumbents (MAT, HAS) face increased competitive pressure on wallet share and may see mix shift away from undifferentiated mass SKUs to higher-margin branded sets. Risk assessment: Key tail risks include product safety/recall, COPPA/privacy regulation on interactive toys, licensing disputes with Disney/Lucasfilm, and component shortages or wireless-charging IP constraints; any of these could blow out costs or delay launches. Time horizons: immediate (days–weeks) for pre-order signals and retailer buy-in; short-term (3–12 months) for sell-through and FY2026 guidance impact; long-term (1–3 years) for ecosystem monetization (tags/recurring attach rates). Hidden dependencies: LEGO’s revenue upside depends on attach-rate for Smart Tags and reusable bricks, plus third-party licensing renewals. Trade implications: Tactical pair trades — short MAT and HAS (each 2–3% notional) vs long AMZN (1–2%) and NXPI or STM (1–2%) to capture retail/semiconductor upside and toy-share loss; enter now, reassess after March sell-through data. Options: buy 3–6 month MAT/HAS puts 10% OTM (size 0.5–1% portfolio risk) as downside hedge; alternatively use NXPI/STM 6–9 month call spreads to limit premium. Rotate modest weight from broad Consumer Discretionary into Retail and Select Semiconductors over 3–12 months. Contrarian angles: Consensus may underprice LEGO’s ability to create recurring hardware/software attach revenue (tags, wireless chargers) — if attach rate >15% of sold sets within 12 months, EBITDA margins for the toy category could re-rate. Historical parallel: Activision’s Skylanders showed initial exuberance then collapse when novelty faded — if LEGO fails to sustain novelty (consumer fatigue within 12–24 months), public peers could rebound, making shorts time-sensitive. Watch March retail sell-through, secondary market pricing, and Disney licensing commentary as make-or-break signals.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.32