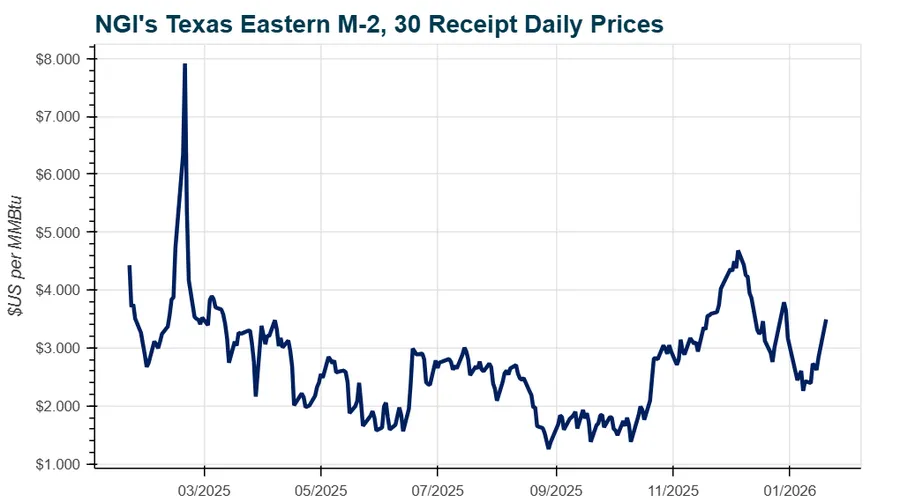

Frigid weather across the Lower 48 has driven a sharp rally in next-day spot gas and February Nymex natural gas futures as expectations mount for steep storage withdrawals and heightened heating demand; aggressive short covering helped push futures higher. The cold threatens production freeze-offs, pipeline disruptions and stress on power plants and LNG terminals, while Permian basin pricing briefly improved in 2025 before pipeline constraints returned deep discounts into the fall, signaling ongoing regional supply and takeaway risks into 2026.

Market structure: The immediate shock is a short-dated supply/demand squeeze — front-month Henry Hub-style spot (NYMEX) will likely trade in volatile bursts as freezing HDDs push heating demand and LNG feedgas draws higher. Winners: US LNG exporters (higher load factors → higher netbacks), pipeline operators with spare capacity (KMI, WMB) and power generators that can pass through fuel costs; losers: gas-weighted domestic E&P names in constrained basins (Permian basin producers facing basis collapse). Over weeks the key is takeaway capacity and storage withdrawals; if storage draws exceed the 5‑yr average by >10% for 2 consecutive weeks, the market re-prices longer-dated strips upwards by multiple 10s of percent. Risk assessment: Tail risks include prolonged freeze causing widespread freeze-offs/shutdowns at LNG terminals (operational) or a regulatory curtailment of exports (policy), which would invert current positions and cause sharp backwardation reversals. Time horizons separate sharply: days — volatility spikes and short-covering; weeks — storage draw trajectory and pipeline outages; quarters — capex and takeaway projects change balance (Permian basis relief or persistent discount). Hidden dependencies: power-plant coal-to-gas switching, industrial curtailment, and gas-for-power arbitrage can amplify draws; a warm spell or delayed LNG commissioning can reverse move quickly. Trade implications: Tactical front-month long exposure (futures or options) is appropriate to capture heating-driven squeezes; medium-term play is long US LNG (ticker LNG) to capture stronger global LNG margins, hedged against domestic producer weakness via short gas-weighted E&P (EQT or DVN) or short Permian exposure. Volatility-rich environment favors defined-risk option structures (debit call spreads or straddles for 2–6 week expiries) over naked futures; consider calendar spreads to monetize winter premium vs. summer strip. Cross-asset: expect modest upward pressure on US CPI and yields if gas-driven power prices persist, and CAD/NGD-sensitive currencies to firm if rally sustains beyond 30 days. Contrarian angles: The market may be overstating persistence — US production resiliency and the high probability of transient weather mean long-dated strips (beyond 6–12 months) could be overbought; buying short-dated strength and selling long-dated rallies (sell 6–12 month NG calls) can capture mean reversion. Historical parallels (2013/2014 cold snaps) show 2–8 week spikes that unwind as production and milder weather return; if front-month rises >+50% in <7 days, expect aggressive profit-taking. Unintended consequences: aggressive short-covering can cascade into basis squeezes hurting local producers and spark regulatory scrutiny that changes the calculus for exporters and pipelines.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.45