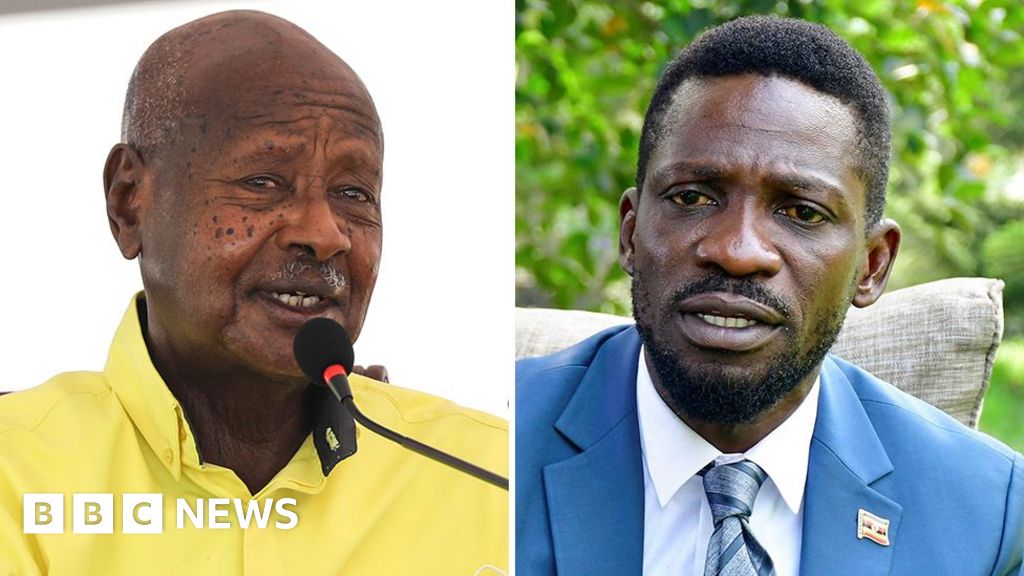

Uganda holds a presidential election on 15 January with 21.6 million registered voters; incumbent Yoweri Museveni, 81, is seeking a seventh successive victory against main challenger Robert 'Bobi Wine' Kyagulanyi amid allegations of repression and disrupted opposition rallies. The economy—marked by high youth unemployment, infrastructural deficits and a corruption ranking of 140/180—features prominently in campaigning; a candidate needs >50% to win outright with results legally due within 48 hours (by 17 January). Persistent concerns about electoral integrity, potential internet shutdowns and a climate of fear increase political and sovereign-risk premia for investments in Uganda and warrant a cautious, risk-off posture for asset allocation exposure to the country.

Market structure: A contested Ugandan election materially favors hard-currency assets and short-term safety plays while pressuring Uganda-specific risk (sovereign FX, local banks, consumer-facing names). Direct losers: Uganda sovereign USD and UGX local debt, Ugandan banks and domestic-focused retail/tourism; potential winners: regional FX havens (KES/USD), USD cash, and contractors tied to security/infrastructure. TotalEnergies’ (TTE) Lake Albert oil timeline is an exposure vector for energy project delays. Risk assessment: Tail scenarios include a disputed result with internet blackout and >10% one-week UGX depreciation, or violent post-election unrest that widens Uganda sovereign spreads by 100–300bps and triggers donor funding freezes. Time horizons: immediate volatility peak Jan 15–17; short-term (30–90 days) political risk premium; long-term (years) governance deterioration that reduces FDI and raises country risk premia. Hidden dependency: donor aid and oil project financing are swing factors that can amplify FX and fiscal stress. Trade implications: Near-term (days–weeks) favor tactical hedges: sell UGX/long USD, buy sovereign protection, and reduce frontier Africa equity beta. Over 1–3 months, selectively buy dislocated African assets if spreads overshoot; energy contractors tied to onshore projects are binary plays around stability. Options can cost-effectively express event risk; size trades conservatively (1–3% portfolio per trade) given high idiosyncratic risk. Contrarian angles: Consensus expects disorder; that may be overdone if Museveni secures quick, uncontested victory—UGX could mean-revert 5–8% in 1–3 weeks. Historical parallels: contested African elections often see sharp short-lived FX moves and protracted policy drift rather than full sovereign default. A disciplined trigger-based re-entry after a 10–20% uniform price dislocation will capture value without taking open political tail risk.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.42