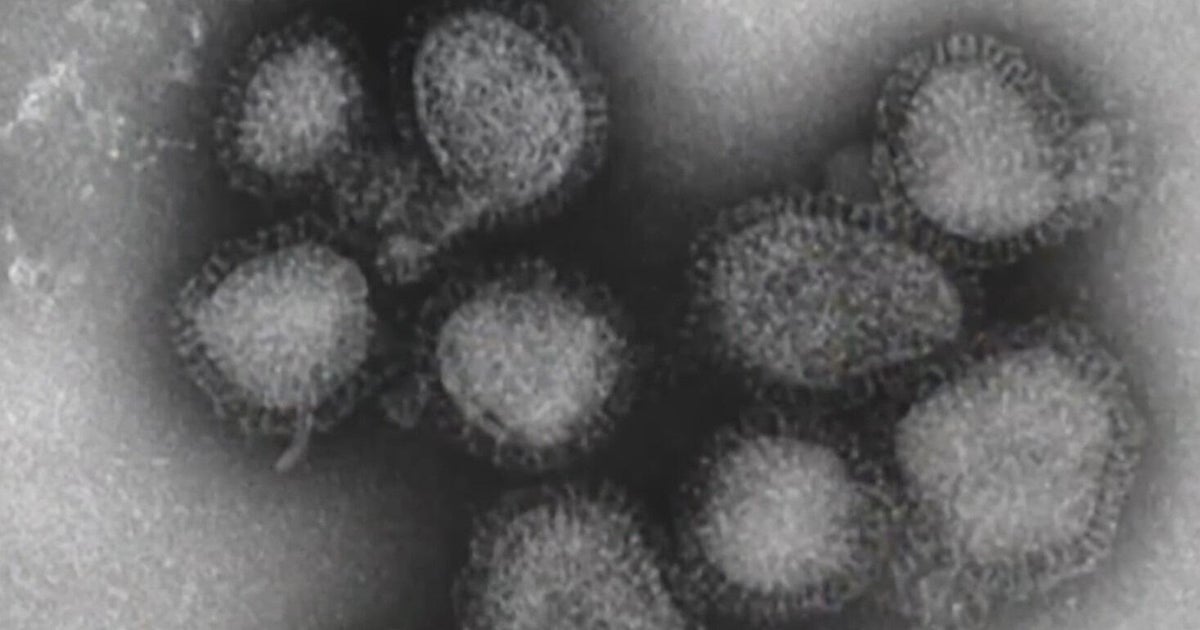

A rapidly spreading influenza subclade K is driving a potential post-holiday surge, with U.S. totals this season at about 4.6 million reported cases and nearly 2,000 deaths (including three children). Medical providers report emergency departments busy with RSV, norovirus and the dominant subclade K strain that may be evading population immunity, raising risks of regional healthcare strain and short-term labor and consumer activity disruptions; Chicago currently reports low activity but could see increases as crowds gather.

Market structure: Short-term winners are diagnostics and point-of-care testing providers (e.g., Abbott - ABT, QuidelOrtho - QDEL), retail pharmacies (CVS, WBA) and manufacturers of seasonal influenza vaccines/antivirals (Sanofi - SNY, GSK - GSK, Pfizer - PFE). Short-term losers are travel/leisure operators (airlines AAL/DAL, hotels MAR) and discretionary retail if holiday gatherings and travel decline; expect 1–5% relative performance drag on travel names during peak weeks. Supply/demand: testing and OTC/antiviral demand will spike over 2–8 weeks; vaccine dose supply likely sufficient but antiviral inventory and rapid-test SKU supply could tighten regionally, lifting prices and margins for suppliers. Risk assessment: Tail risk includes a larger-than-expected subclade wave that forces school closures or targeted procurement (2–8 week shock) or an unexpected antiviral shortage triggering emergency contracts and regulatory price/allocations. Time horizons: immediate (days) for diagnostics demand and travel impact, short-term (weeks–months) for vaccine uptake and retail pharmacy revenue, long-term (quarters) for changes in consumer behavior and telemedicine adoption. Hidden dependencies: concurrent RSV/norovirus surge can strain hospitals (HCA) and amplify diagnostics demand; elective procedure deferrals could temporarily depress hospital revenue. Trade implications: Direct plays—establish tactical longs in ABT/QDEL and CVS for 4–8 week plays; tactical shorts or hedges in AAL/DAL for same horizon. Options: buy 1–2 month call spreads on ABT/QDEL or 1–2 month put spreads on AAL with 10–20% OTM strikes to express asymmetric risk. Sector rotation: shift 3–5% from consumer discretionary into healthcare staples/diagnostics now and rebalance after 6–8 weeks or when CDC reports two consecutive week-over-week declines. Contrarian angles: Consensus may underprice rapid-test recurring demand — adoption accelerates if VE (vaccine effectiveness) is <40% versus subclade K; diagnostics earnings could beat by 5–10% off-season. Reaction to travel names may be overdone if flu peak is short (2–6 weeks) — avoid turning tactical shorts into structural positions. Historical parallel: 2017–18 severe seasons drove transient revenue boosts for vaccine and diagnostics but limited multi-quarter share gains; watch for supply-chain bottlenecks that could create temporary winners rather than durable market share shifts.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25