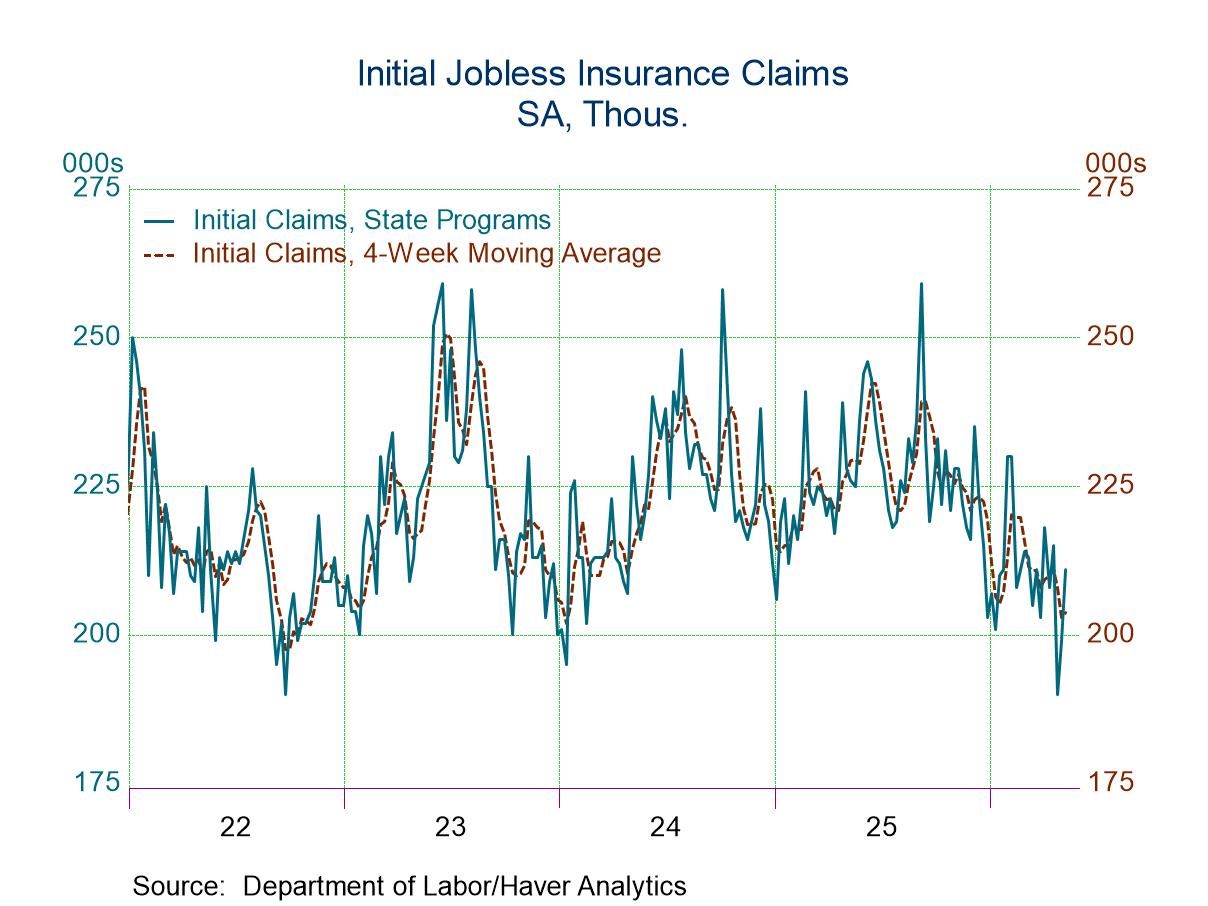

Initial U.S. unemployment claims rose by 12,000 to 211,000 in the week ending May 9, above the 205,000 consensus, while the four-week average increased to 203,750. Continuing claims also rose by 24,000 to 1.782 million, but the insured unemployment rate moved back up only to 1.2%, indicating a still-firm labor market. The report is mildly negative for growth expectations but is unlikely to be a major market driver on its own.

The real message is not that labor is weakening, but that the labor market is losing its ability to re-accelerate from a still-tight base. A modest rise in claims at these levels is usually benign for equities, yet the combination of higher initial claims and a higher insured rate suggests a slow leak in labor demand rather than a one-off noise event. That matters because equity multiples are still priced for an earnings landing that remains soft without turning into outright deterioration. The second-order effect is on Fed reaction function, not headline macro optics. If claims keep grinding higher for 4-6 weeks while continuing claims stay near cycle lows, the market will read it as “disinflation with intact employment,” which is the sweet spot for duration and quality growth. But if the weekly trend persists into a 6-8 week window, cyclical payroll-sensitive names and lower-quality consumer credits become vulnerable as the market starts to price a slower nominal growth path. For AIG specifically, the signal is mixed but slightly constructive on the P&C side and neutral-to-negative on specialty exposure tied to payroll-sensitive commercial activity. Softer labor typically reduces workers’ comp severity with a lag, but it can also pressure premium growth in small commercial lines if hiring freezes broaden. The contrarian point is that this is not yet a recession signal; it is a volatility suppressant until claims move materially above the low-200k range for multiple prints, so chasing defensive equity exposure here is probably late.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

-0.05

Ticker Sentiment