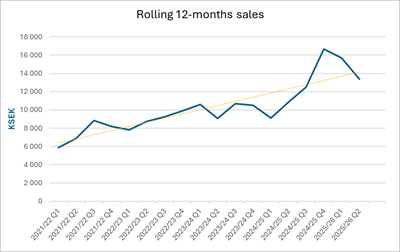

Phase Holographic Imaging reported weak Q2 2025/26 results with net sales of 306 KSEK (vs 2,977 KSEK prior year), EBITDA of -5,446 KSEK and a net loss of -7,761 KSEK; H1 (May–Oct) sales were 671 KSEK with a net loss of -16,303 KSEK. Cash and unused credit stood at 4,221 KSEK and the company says capital resources are approaching limits while the Board pursues a financing solution. Management cites a slower-than-expected sales transition from distributor Altium and customer wait for the new HoloMonitor Next Generation (launched 17 Dec after quarter end), while also expanding into veterinary IVF (trademark “HoloOocyte”) and referencing existing patent EP2446251A1.

Market structure: PHI’s results signal a classic small-cap medtech transition: weak near-term revenue (Q2 sales down ~90% vs prior comparable period) while investing in a product relaunch and new vertical (veterinary IVF). Winners in the short run are large, diversified lab-equipment OEMs (e.g., Danaher Ticker: DHR, Thermo Fisher: TMO) that can absorb demand volatility and compete on sales reach; niche IVF suppliers (Vitrolife: VITR.ST) gain optionality if veterinary IVF scales. Pricing power for PHI is limited—long 6–12 month academic sales cycles and cash constraints (4.2 MSEK available) mean adoption-driven revenue is lumpy and sensitive to financing events. Risk assessment: Immediate (days) tail risk is a dilutive equity raise or covenant breach — PHI states capital resources are near limits and board is “actively working” on a solution; any financing >20% dilution would likely trigger >30% share-price decline in small-cap peers. Short-term (weeks–months) risks include slower-than-expected Holomonitor Next Generation uptake and slow veterinary validation (pilot results likely 6–12 months). Hidden dependencies: sales conversion depends on grant cycles and re-onboarding former Altium channels (6–12 month timeline), and outsourced Swedish manufacturing concentration creates single-supplier risk. Key catalysts: financing announcement (30–90 days), first paid orders for Next Gen (0–6 months), veterinary pilot data (6–12 months). Trade implications: Avoid or short speculative small-cap medtech exposure ahead of a financing event; implement size-limited bearish positions (1–2% NAV) via put spreads on medtech/device ETF IHI (3–6 month expiries, 5–10% OTM). Establish defensive longs in DHR and TMO (1–3% NAV each) via 3–6 month call spreads to capture secular lab-equipment resilience if small players falter. For veterinary/IVF exposure, a small tactical long (1% NAV) in Vitrolife (VITR.ST) or Zoetis (ZTS) is appropriate, scaling up only after validated pilot data. Contrarian view: The market may over-discount PHI’s technology value—if Holomonitor Next Generation converts even 10–15% of PHI’s installed-base prospects within 12 months and financing is non-dilutive (debt <€1–2M equivalent), equity could re-rate materially. Historical parallels: niche imaging tools (early Cytiva/Bruker moves) showed 2–3x re-rates after reproducible clinical workflows were proven; however, execution and capital are binary. Unintended consequence: the veterinary pivot could dilute focus and slow clinical adoption, so only increase exposure on clear evidence of commercial traction or non-dilutive partnership contracts.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly negative

Sentiment Score

-0.55