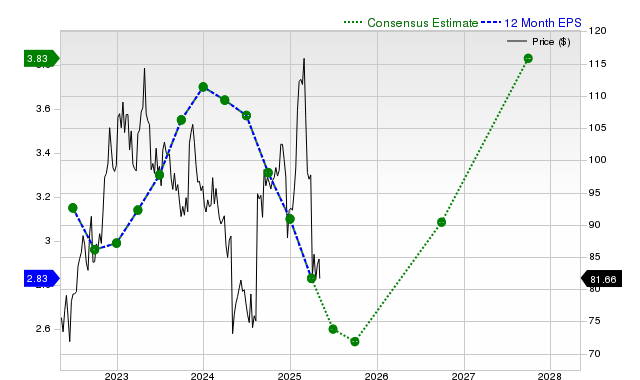

Starbucks is showing mixed near-term results but stronger medium‑term outlook: Zacks' consensus expects Q current EPS of $0.60 (‑13% year-over-year) with the 30‑day estimate down ~3.2%, while fiscal year consensus EPS is $2.40 (+12.7%) and next fiscal year $3.04 (+26.8%). Revenue estimates are $9.64bn for the current quarter (+2.6% yoy), $38.49bn for the current fiscal year (+3.5%) and $41.19bn next fiscal year (+7%); last quarter revenue of $9.57bn beat consensus by ~2.6% while EPS of $0.52 missed. Zacks assigns Starbucks a Rank #3 (Hold) and a Value Style Score of C, signaling the stock may perform roughly in line with the market absent further estimate revisions.

Market structure: Starbucks (SBUX) is the dominant quick-service coffee incumbent so it wins from urban foot‑traffic normalization and loyalty/digital mix — events that support low-teens EPS growth next fiscal year (consensus $3.04). Losers are smaller, low-margin casual‑dining chains that lack scale to absorb input inflation or invest in digital; commodity exposure (arabica) and labor cost pass‑through capacity will determine near‑term share shifts. Cross‑asset: a material SBUX shock would be idiosyncratic — modest spread widening in high‑yield consumer debt and a short‑term lift in equity options IV; macro FX/commodity moves are likely limited unless coffee prices spike >20% YoY. Risk assessment: Tail risks include a >10% demand drop in China/urban US (regulatory or COVID resurgence), material coffee‑bean price shock (>20%) and coordinated US labor action that compresses margins by 300–500 bps. Immediate risk (days) is earnings‑driven IV and headline volatility; short term (1–3 months) is estimate revisions and comps; long term (12–24 months) is store unit economics, international scaling and digital margin leverage. Hidden dependencies: same‑store sales mix (food vs drinks) and loyalty member churn drive margin nonlinearly; franchise vs company‑owned mix affects cash flow volatility. Trade implications: Direct: establish a size‑weighted 2–3% long SBUX position on an 8–12% pullback from today (or after a single‑quarter EPS miss) with a 12‑month target +15–25% and a hard 6% stop. Pair: long SBUX vs short casual‑dining ETF (e.g., RDN/PNL alternatives) to isolate premium urban coffee growth. Options: if holding into earnings, buy 3‑6 month 5% OTM puts (cost ~2–3% premium) as insurance or buy a 6‑month call spread (e.g., 0–+20% upside) to cap theta. Sector rotation: trim broader cyclical consumer exposure by 1–2% and redeploy to Staples (KO, PG) and select AI/semis (NVDA) where secular dynamics dominate. Contrarian angles: The consensus (Zacks Rank #3) overweights short‑term EPS revisions and underweights revenue resilience and digital margin optionality; a small EPS miss could be overpunished by 10–15% intraday despite intact fundamentals. Historical parallels: prior Starbucks selloffs (2014, 2018) saw multiple compression then rebound as marketing/channel fixes restored SSS — repeatable given trademark loyalty. Unintended consequences: aggressive cost cuts to meet quarterly EPS could erode brand pricing power and slow long‑run unit economics, turning a short‑term fix into long‑term value destruction.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.05

Ticker Sentiment