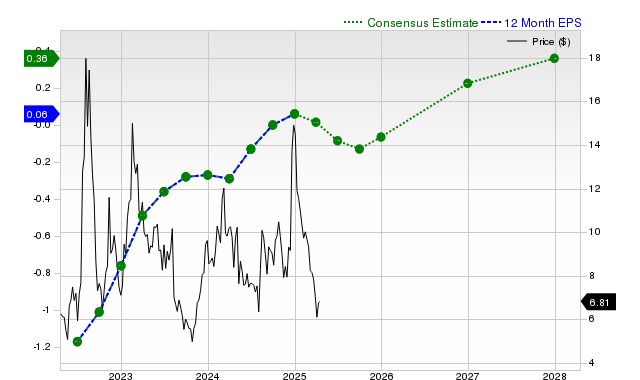

SkyWater Technology reported revenue of $150.74 million in the last quarter (+60.7% YoY) and EPS of $0.24 versus $0.08 a year ago, beating consensus revenue ($135.5m) by 11.25% and EPS by 241.18%. Analysts' consensus shows a small current-quarter loss of $0.01 but meaningful upward estimate revisions recently (current FY EPS $0.05; next FY $0.28) and sizable revenue growth expectations ($160m est. for the current quarter, +112% YoY; FY estimates $431.05m and $605.8m). Zacks assigns a Rank #3 (Hold) and a Value Style Score of C; the stock has underperformed the market over the past month (-13.6% vs S&P +0.4%, industry +6.5%), suggesting mixed near-term sentiment despite strong recent beats.

Market structure: SkyWater (SKYT) is capturing onshore foundry demand (defense, specialized analog/SiGe nodes) so beneficiaries include domestic specialty foundries and equipment suppliers while large offshore, high-volume logic foundries see less direct gain. SKYT’s reported +60% yoy revenue (last quarter) and consensus +26–41% FY growth imply constrained capacity and pricing power in niche nodes; expect higher booking leverage but elevated capex needs. Cross-asset: continued outperformance at SKYT would tighten credit spreads for small-cap capex financings, lift implied vol in SKYT options, and have limited FX/commodity impact outside higher semiconductor equipment orders.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.08

Ticker Sentiment