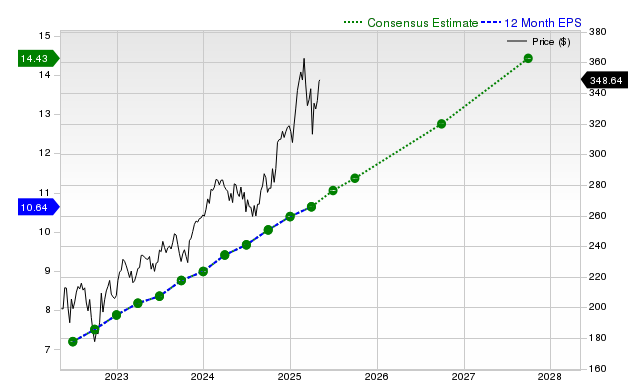

Visa (V) shares have underperformed the broader market and its industry recently, returning -1.3% over the past month. Despite this, the global payments processor is projected to achieve strong financial results, with current fiscal year EPS estimated at $11.43 (+13.7% YoY) and revenue growth of 10.9% to $39.84 billion, building on a track record of consistently beating consensus estimates. While analysts maintain a Zacks Rank #3 (Hold) suggesting in-line market performance, the stock's Zacks Value Style Score of 'D' indicates it currently trades at a premium relative to its peers.

Visa Inc. (V) presents a dichotomy between its recent market performance and its strong underlying fundamentals. Over the past month, the stock has underperformed, declining 1.3% against a 3.6% gain for the S&P 500 composite and a 2.6% loss for its industry. Despite this price weakness, the company's growth outlook remains robust. Consensus estimates project double-digit growth, with current fiscal year revenue expected to increase by 10.9% to $39.84 billion and EPS by 13.7% to $11.43. This forward momentum is supported by a strong track record of execution, as Visa has surpassed both revenue and EPS consensus estimates for the last four consecutive quarters, reporting a +3.11% revenue surprise and a +4.2% EPS surprise in its most recent quarter. However, two key factors temper this positive outlook: valuation and analyst sentiment. The stock's Zacks Value Style Score of 'D' indicates it is trading at a premium compared to its peers. Furthermore, its Zacks Rank #3 (Hold) suggests that while fundamentals are solid, the lack of significant recent upward revisions in earnings estimates points toward an expectation of near-term performance in line with the broader market, rather than significant outperformance.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.20

Ticker Sentiment