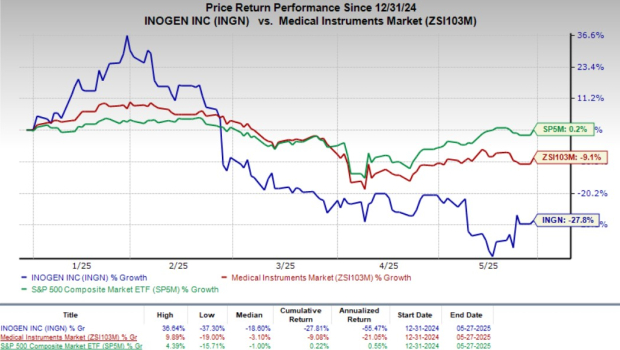

Inogen (INGN) is positioned for growth, driven by strong demand for portable oxygen concentrators (POCs), with the POC market projected to reach $22.63 billion by 2029, and strategic collaborations with Jiangsu Yuyue and Yuwell to expand its product portfolio and market presence, particularly in China. First-quarter 2025 revenues increased 5.5% year-over-year, with domestic and international business-to-business sales up 29.9% and 22.9% respectively; however, the company faces challenges from seasonality, increased advertising headwinds, and foreign exchange volatility, which negatively impacted international sales by 160 basis points in Q1 2025.

Inogen (INGN), a provider of portable oxygen concentrators (POCs) with a market capitalization of $205.9 million, is positioned for growth within the robust POC market, which is projected to expand at an 8.5% CAGR to $22.63 billion by 2029. The company's first-quarter 2025 financial results demonstrated positive momentum, with a 5.5% year-over-year increase in quarterly revenues, significantly driven by a 29.9% rise in domestic business-to-business sales and a 22.9% increase in international business-to-business sales, while adjusted gross margin improved by 20 basis points to 47.9%. Key strategic initiatives include the recent FDA clearance for its Simeoxin product in the U.S. and collaborations with Jiangsu Yuyue Medical Equipment & Supply Co. and Yuwell, aimed at broadening its product portfolio, enhancing innovation, and accelerating entry into the Chinese market. Despite these strengths, a Zacks Rank #2 (Buy) rating, a projected 7.2% earnings growth for 2025, and an attractive price-to-sales ratio of 0.6x compared to the industry's 2.6x, Inogen's stock has underperformed, declining 21.4% year-to-date. The company faces challenges including typical seasonal softness in its direct-to-consumer channel, anticipated advertising headwinds, and foreign exchange volatility, which negatively impacted Q1 2025 international sales by 160 basis points. Nonetheless, there is a positive trend in analyst estimates, with the Zacks Consensus Estimate for its 2025 loss per share narrowing by 9.4% in the past 30 days.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

strongly positive

Sentiment Score

0.75

Ticker Sentiment