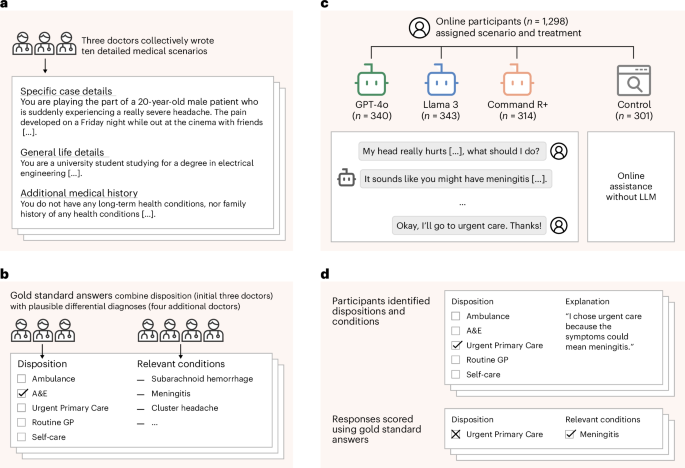

A preregistered randomized study of 1,298 UK adults across ten clinical vignettes found that GPT-4o, Llama 3 and Command R+ performed well when given scenarios directly (models suggested relevant conditions ≈94.9% and dispositions ≈56.3% on average) but participants using those same LLMs identified relevant conditions in under ~34.5% of cases and dispositions in under ~44.2%, no better than a control using usual home resources. The authors attribute the gap to human–LLM interaction failures and show that standard benchmarks and simulated-user tests poorly predict real-user performance, implying adoption, product-design and regulatory risks for firms deploying patient-facing medical AI without systematic human user testing.

Market structure: The study reallocates advantage to large, regulated cloud/AI incumbents (MSFT, GOOGL/GOOGL, META) and GPU suppliers (NVDA) that can offer validated, audited medical LLM stacks and human-in-the-loop tooling; consumer-focused LLM/telehealth players (e.g., TDOC, small-cap AI-health startups) face demand drag and higher compliance costs. Pricing power shifts toward providers who bundle safety, explainability and audit logs—expect 5–15% premium for enterprise-grade APIs vs. commodity offerings over 12–24 months. Risk assessment: Tail risks include rapid regulatory intervention (FDA/HHS/MHRA restricting direct-to-consumer diagnostic LLMs) or a high-profile malpractice suit that could force recalls—each could cut TAM for consumer medical LLMs by >30% in 6–12 months. Short-term (days–weeks) market moves should be muted; medium-term (3–9 months) volatility will rise around guidance/releases; long-term (12–36 months) winners are firms with validated clinical pipelines and indemnity frameworks. Hidden dependency: user-behavior failure modes mean model accuracy ≠ product utility. Trade implications: Favor long positions in large cloud/AI platforms and GPU exposure (MSFT 2–3% portfolio overweight, NVDA 1–2% overweight) for 6–12 months; hedge via short exposure to consumer telehealth/small-cap AI-health (TDOC 1–2% short or buy 3–6m put spread). Use pair trade long MSFT / short TDOC to capture structural share shift. Options: buy NVDA 6–9m calls (delta >0.6) on pullbacks; buy TDOC 3–6m put spreads to limit cost. Contrarian angles: Consensus underestimates demand for audited, deterministic conversational workflows—EMR/cloud integrators (ORCL) and insurers (UNH) that fund validated LLM pilots could be quietly undervalued. The market may be over-penalizing AI generally; a 10–20% pullback in NVDA or MSFT on regulatory headlines is a buying opportunity if core revenue guidance holds. Watch for consolidation opportunities among vetted clinical-AI vendors in 12–24 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35

Ticker Sentiment