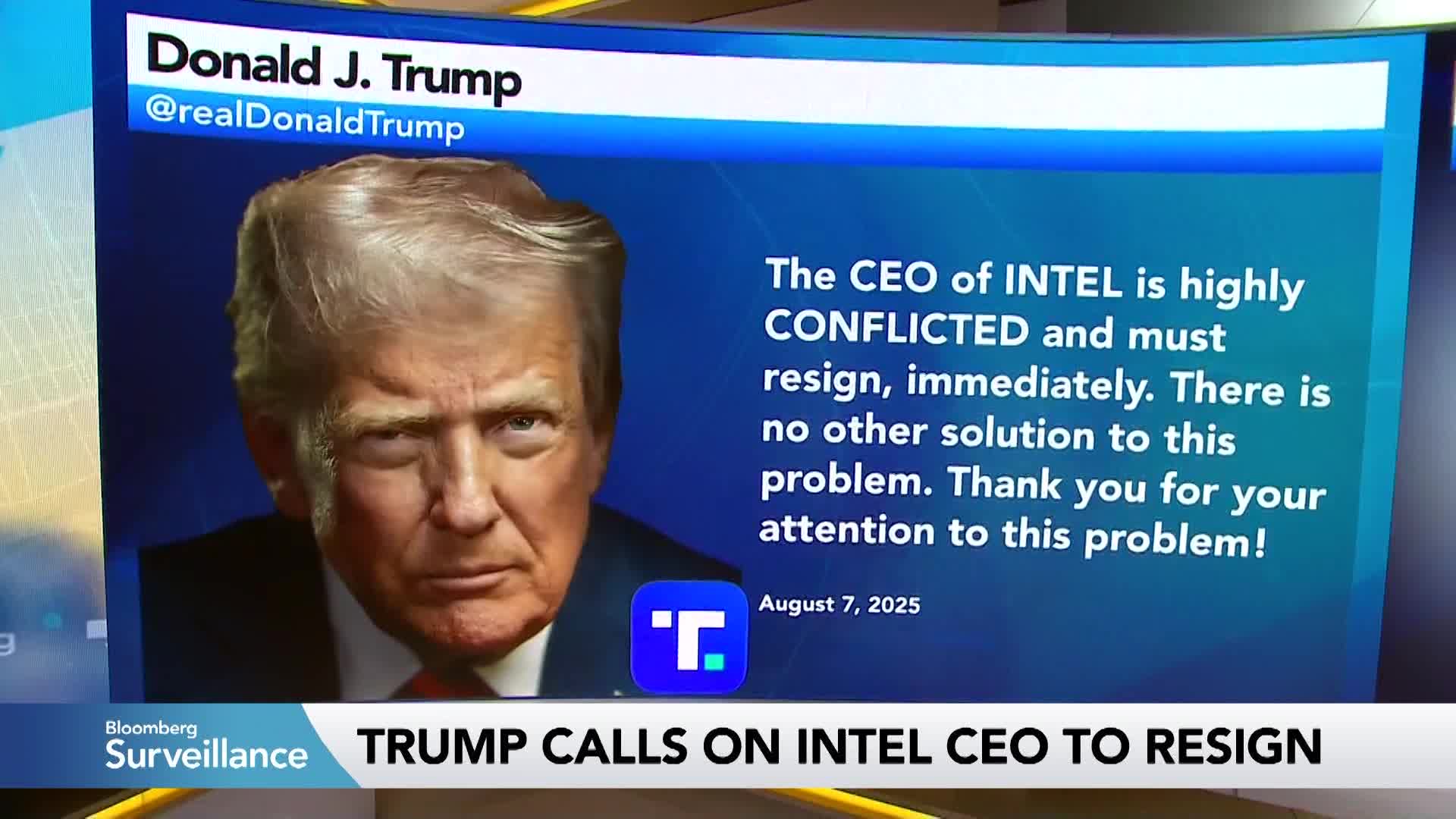

Recent financial headlines reveal a softening U.S. labor market, with continuing jobless claims hitting their highest level since November 2021. Corporate news includes Apple's $600 billion U.S. investment, reportedly influenced by prior tariff threats, while political figures continue to weigh in on corporate leadership and Federal Reserve appointments. Concurrently, the U.S. is weighing sanctions on Russian oil, a development with potential implications for global energy markets.

The current market landscape is characterized by a confluence of challenging macroeconomic data and significant, company-specific developments driven by political factors. A notable indicator of economic softening is the rise in U.S. continuing jobless claims to their highest level since November 2021, which supports a strategist's view of limited upside in U.S. markets. This backdrop is complicated by political uncertainty, including deliberations over the next Federal Reserve Chair and potential new sanctions on Russian oil, which carry implications for monetary policy and energy markets, respectively. At the corporate level, there is a sharp divergence in sentiment. Apple (AAPL) exhibits strong positive momentum (sentiment score: 0.8) following its announcement of a $600 billion investment in the U.S., reportedly linked to prior tariff threats. Conversely, Intel (INTC) faces a significant governance headwind and highly negative sentiment (-0.9) due to a public call from a political figure for its CEO's resignation, highlighting the direct impact of political discourse on corporate stability.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.50

Ticker Sentiment