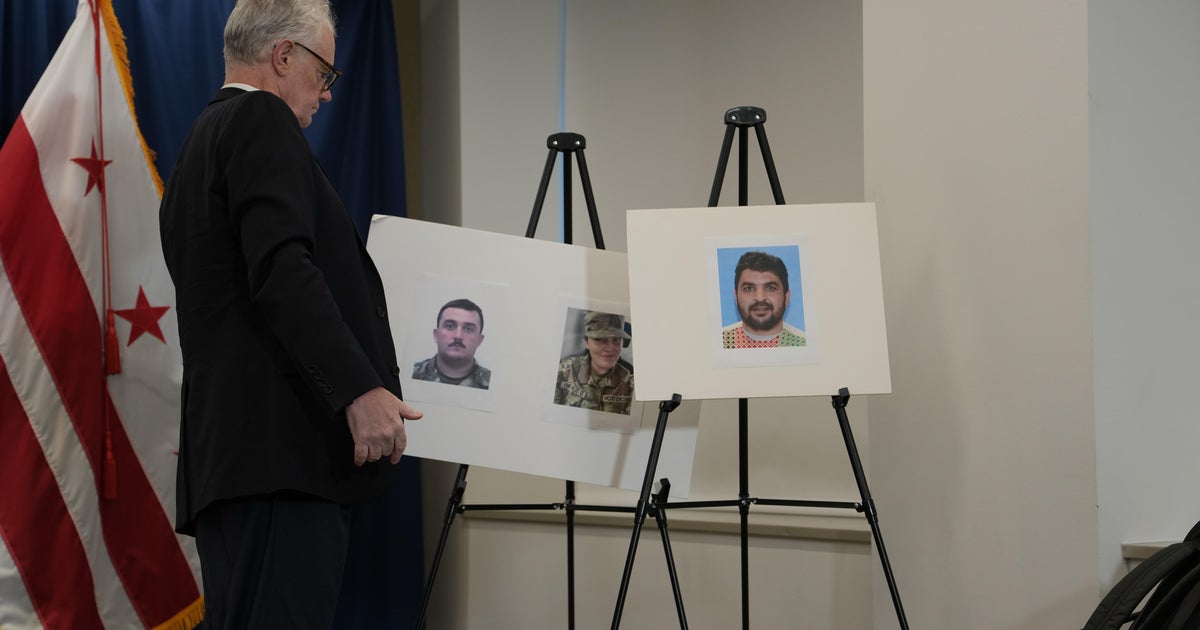

The Trump administration has ordered a "full-scale, rigorous reexamination" of all green cards for immigrants from a 19-country "country of concern" list (including Afghanistan, Cuba, Haiti, Iran, Somalia, Libya, Sudan, Yemen and Venezuela) after a Washington, D.C. shooting by an Afghan national paroled into the U.S. in 2021 under Operation Allies Welcome. DHS is reviewing asylum cases approved under the prior administration, has paused Afghan immigration processing, and the move signals a significant hardening of immigration enforcement and legal-review risk that raises regulatory and political uncertainty and could disrupt resettlement operations.

Market structure: A stricter immigration rescreening raises demand for homeland-security, surveillance and detention services (DHS integrators and contractors) while pressuring labor-intensive segments (hospitality, agriculture, construction) that rely on recent arrivals. Expect government procurement pricing power to increase over 3–12 months as agencies reallocate budgets; migrant labor tightness could push local wage inflation 2–6% in concentrated markets. Cross-asset: near-term risk-off should lift Treasuries (yields down 10–25bp) and USD slightly; equity implied volatility in small caps and regional banks will spike 10–30% intraday. Risk assessment: Tail risks include accelerated removals or mass litigation that disrupt supply chains (low-probability, high-impact) and political backlash that reverses policy within 3–6 months. Immediate window (days) = headline-driven volatility and trading opportunities; short-term (weeks–months) = contract awards and sector repricing; long-term (6–24 months) = structural labor substitution and automation investments. Hidden dependencies: potential spillover to H‑1B/Talent policies, local tax receipts, and state budgets that could amplify credit stress in municipal and regional-bank exposures. trade implications: Tactical longs: DHS-focused primes (LDOS, LHX) and select security suppliers; tactical shorts/underweights: hotel operators (MAR), casual dining (DRI), farm-equipment distributors exposed to labor substitution lag. Options: buy 30–90 day put spreads on small-cap indices (e.g., IWC) sized 0.5% NAV as hedge and buy 3–6 month call spreads on LDOS sized 1–3% NAV. Pair trade: long LDOS (2–3% NAV) vs short MAR (1–1.5% NAV), target 12–20% relative outperformance in 3–6 months. contrarian angle: The market may overstate breadth of impact — affected cohorts (~85k Afghans plus others) are small relative to US labor force, so any broad sell-off is likely overdone. Legal and operational frictions will slow removals, creating buy-on-dip opportunities in consumer names after 4–8 weeks when headlines subside. Historical parallels (post-9/11 security spend spike but limited long-term consumer impact) suggest a 3–6 month alpha window in security contractors versus cyclical consumer names.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35