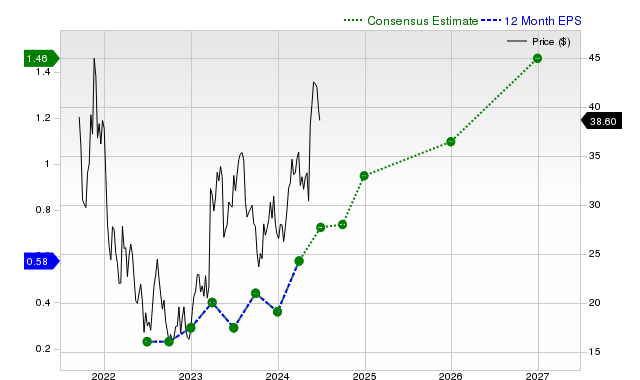

On Holding (ONON) shares have declined 7.5% over the past month, significantly underperforming the S&P 500, leading Zacks to assign a "Hold" rating (Zacks Rank #3). While the running-shoe and apparel company projects robust revenue growth, with current fiscal year sales estimated up 31.3%, and current quarter EPS up 50% year-over-year, its next fiscal year EPS estimate has seen a recent 2.6% downward revision. Furthermore, ONON's last reported quarter showed a revenue beat but an EPS miss, and its valuation is graded 'F' by Zacks, indicating it trades at a premium to peers.

On Holding (ONON) presents a conflicting profile of robust top-line growth against concerns over profitability and valuation. The company's stock has recently underperformed, declining 7.5% over the past month while the S&P 500 gained 5%. Despite this, revenue projections remain strong, with consensus estimates pointing to 33.4% year-over-year growth for the current quarter and 31.3% for the full fiscal year. This growth is supported by a history of beating revenue estimates in three of the last four quarters. However, this top-line strength has not consistently translated to the bottom line. The company missed its last EPS estimate by 4.17% and has surpassed EPS consensus only once in the past four quarters. Compounding this concern, the consensus EPS estimate for the next fiscal year has been revised downward by 2.6% in the last month, suggesting potential future margin pressure or decelerating profitability, even as current year estimates see a minor +1.8% YoY growth. The most significant headwind is valuation; the stock receives a Zacks Value Style Score of 'F', indicating it trades at a significant premium to its peers. This combination of high growth, inconsistent profitability, and a premium valuation underpins its neutral Zacks Rank #3 (Hold) rating.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.00

Ticker Sentiment