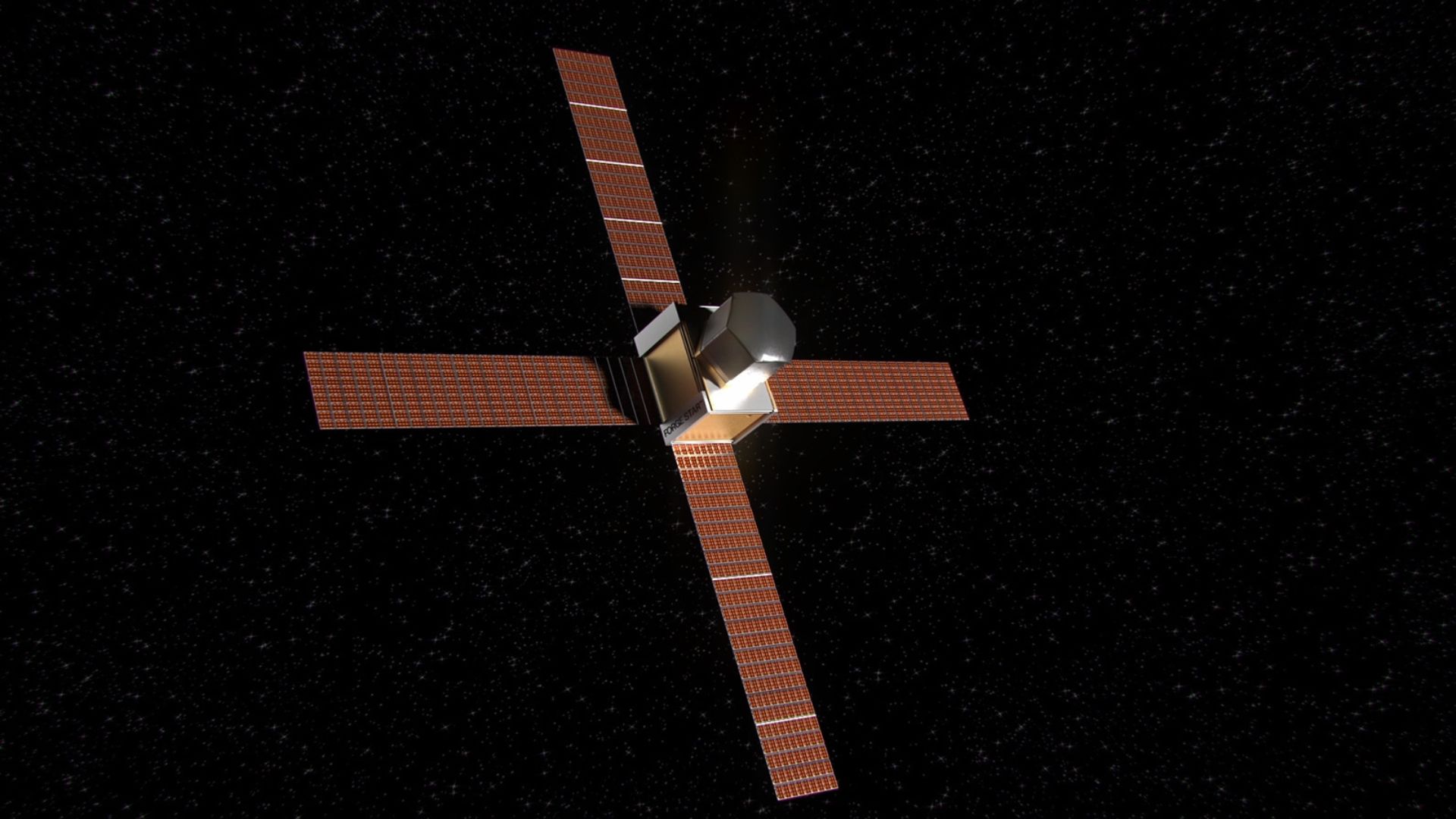

Cardiff-based Space Forge successfully powered a microwave-sized furnace to 1,000°C in orbit after launching its first satellite on SpaceX's Transporter-14 in June 2025, validating a key step toward in-space semiconductor production. The company claims space-built wafers could be up to 4,000x purer and plans a larger factory with capacity for 10,000 chips, but material supply, product return logistics and environmental costs from frequent launches remain significant commercialization risks.

Market structure: Successful furnace demos shift optionality toward launch, in‑space logistics and recovery specialists rather than incumbent foundries. Winners: launch providers (RKLB), satellite/platform integrators (MAXR, LHX) and specialized reentry/logistics suppliers; losers: marginal terrestrial niche fabs that rely on volume rather than specialty premiums. Expect pricing power for orbital services if launch cost-to-LEO falls below ~$1,500/kg (vs ~2.5–3k/kg today); meaningful market share shift likely 3–7 years, not immediate. Risk assessment: Tail risks are technical failure (catastrophic loss of prototypes), regulatory clamps (environmental or ITAR restrictions), insurance market shock and orbital debris rules — any could wipe valuations >50%. Immediate market impact: near‑zero (days); short term (3–12 months): binary tech demos and funding rounds matter; long term (3–7 years): commercial scale economics and launch cadence are determinative. Hidden dependencies: affordable round‑trip recovery, radiation/hardening yield degradation, and raw‑material feedstock supply chains. Trade implications: Tactical winners are small‑cap launch/integration names and space ETFs; avoid assuming terrestrial fabs (TSM, ASML) will be displaced — space chips are likely specialty with 2–5% share by 2030 under aggressive adoption. Options: use long‑dated call spreads to express asymmetric upside while capping premium burn; pair trades can isolate launch exposure vs legacy primes. Catalysts to watch: 3 successful production+reentry cycles within 12 months, or FAA/UK routine reentry approvals. Contrarian: Consensus overweights the technology novelty and underestimates logistics economics — the market is likely underpricing regulation and reentry cost. Historical parallel: early offshore oil/gas showed proof‑of‑concept for decades before material production; expect long gestation and selective winners. Unintended consequence: an environmental/launch moratorium would swiftly reprice all small‑cap launch assets down >40%.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.30