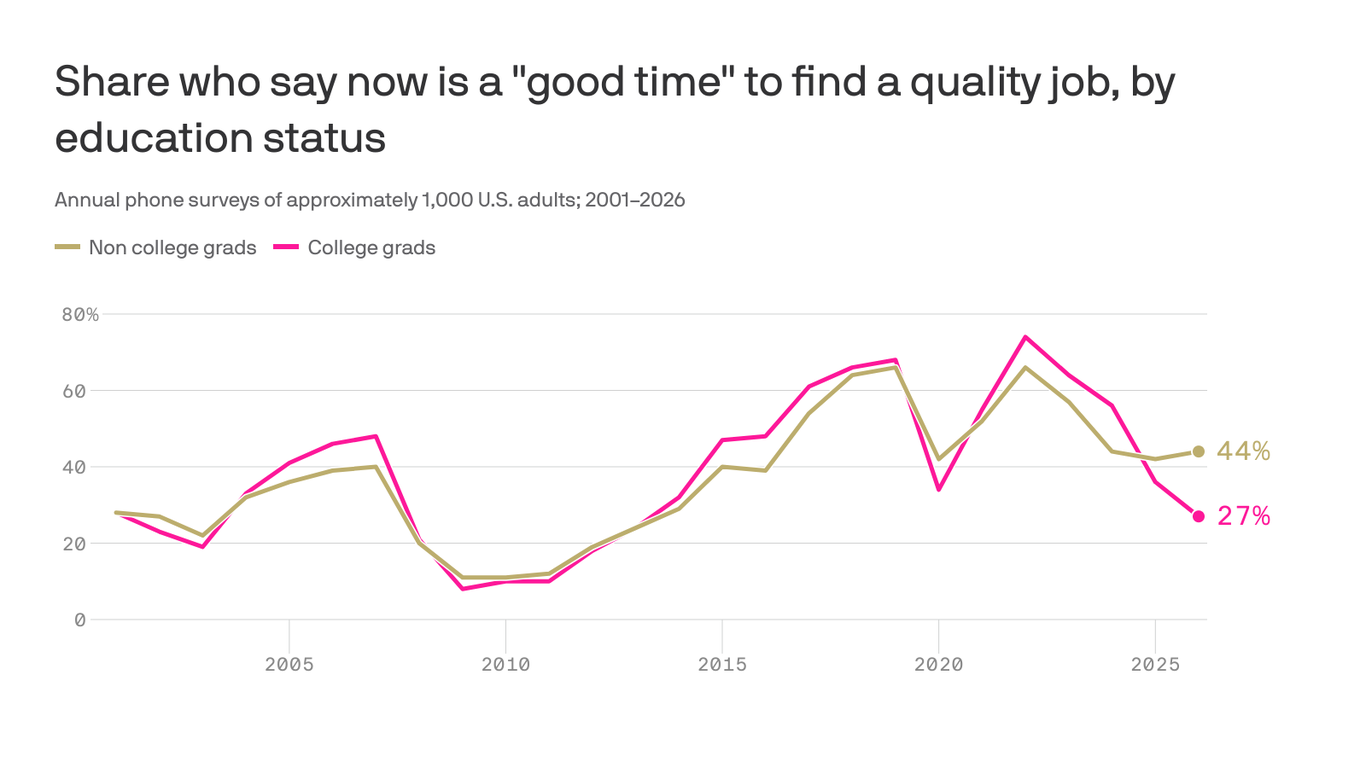

Key data: just 27% of college graduates say now is a good time to find a quality job vs 44% of non-graduates (widest gap on record); among workers only 19% of college-educated employees say it's a good time vs 35% for non-grads. Hiring has slowed materially — federal data show hiring at its weakest since 2013 outside the pandemic, with Indeed reporting 29% fewer software developer listings, 27% fewer marketing listings and 36% fewer media/communications listings vs pre-pandemic. Implication: deteriorating sentiment among educated professionals, combined with AI disruption, rising oil prices and private-credit stress, raises downside risk to employment and growth and could pressure tech/white‑collar sector performance.

Shifted sentiment among college-educated workers is a leading indicator for a structural slowdown in white‑collar churn rather than an immediate spike in layoffs. Reduced job‑to‑job mobility will compress wage growth in professional services and slow spending on discretionary, experience-based consumption that skews higher up the income ladder; expect a visible earnings hit to vendors that monetize hiring and B2B professional services over a 3–12 month horizon.

The bifurcation in hiring creates clear sectoral winners: healthcare staffing, industrial capex suppliers, and parts of manufacturing that are rehiring will see resilient cash flows and order books; losers will be recruiters and payroll-dependent SaaS exposed to enterprise hiring and marketing budgets, plus office landlords who rely on long‑dated professional tenancy. Private credit fragility amplifies this: smaller professional services firms reliant on non‑bank financing are the most levered to a tightening in liquidity, producing faster downside than headline corporate payrolls imply.

Reversal catalysts: a sustained rebound in job openings or a sharp policy response (targeted reskilling subsidies, a coordinated private credit backstop) could reflate demand for professional labor within 1–3 quarters. Tail risks include a compounded AI-driven demand destruction or a private credit shock that propagates to mid‑market capex and employment, which would extend the earnings reset into 2026–2027.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately negative

Sentiment Score

-0.45