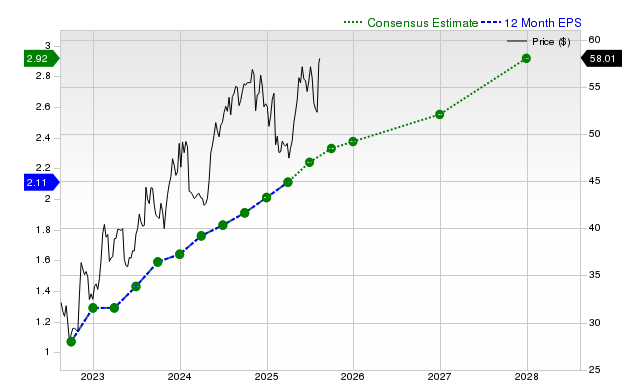

New York Times Co. (NYT) is experiencing robust upward revisions in earnings estimates, signaling potential continued upside. Analysts have pushed the current quarter's consensus EPS estimate up 10.2% to $0.54 (+20.0% YoY) and the full-year estimate up 6.16% to $2.28 (+13.4% YoY), driven by multiple positive revisions and no negative ones. This strong earnings outlook has resulted in a Zacks Rank #2 (Buy) for NYT and has already contributed to a 6.7% stock gain over the past four weeks, reflecting growing investor confidence.

The investment case for New York Times Co. (NYT) is currently underpinned by a strong and unanimous upward trend in analyst earnings estimates. Over the past month, consensus for the current quarter has risen 10.2% to $0.54 per share, representing 20.0% year-over-year growth, based on two positive revisions and no negative ones. Similarly, the full-year consensus estimate has increased 6.16% to $2.28 per share, a 13.4% rise from the prior year, with three analysts raising their forecasts. This positive sentiment has been a key driver of the stock's recent performance, which saw a 6.7% gain over the last four weeks. The culmination of these factors is a Zacks Rank #2 (Buy) designation, which the source material correlates with a history of outperformance, suggesting that the market is actively responding to the company's improving earnings outlook.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly positive

Sentiment Score

0.85

Ticker Sentiment