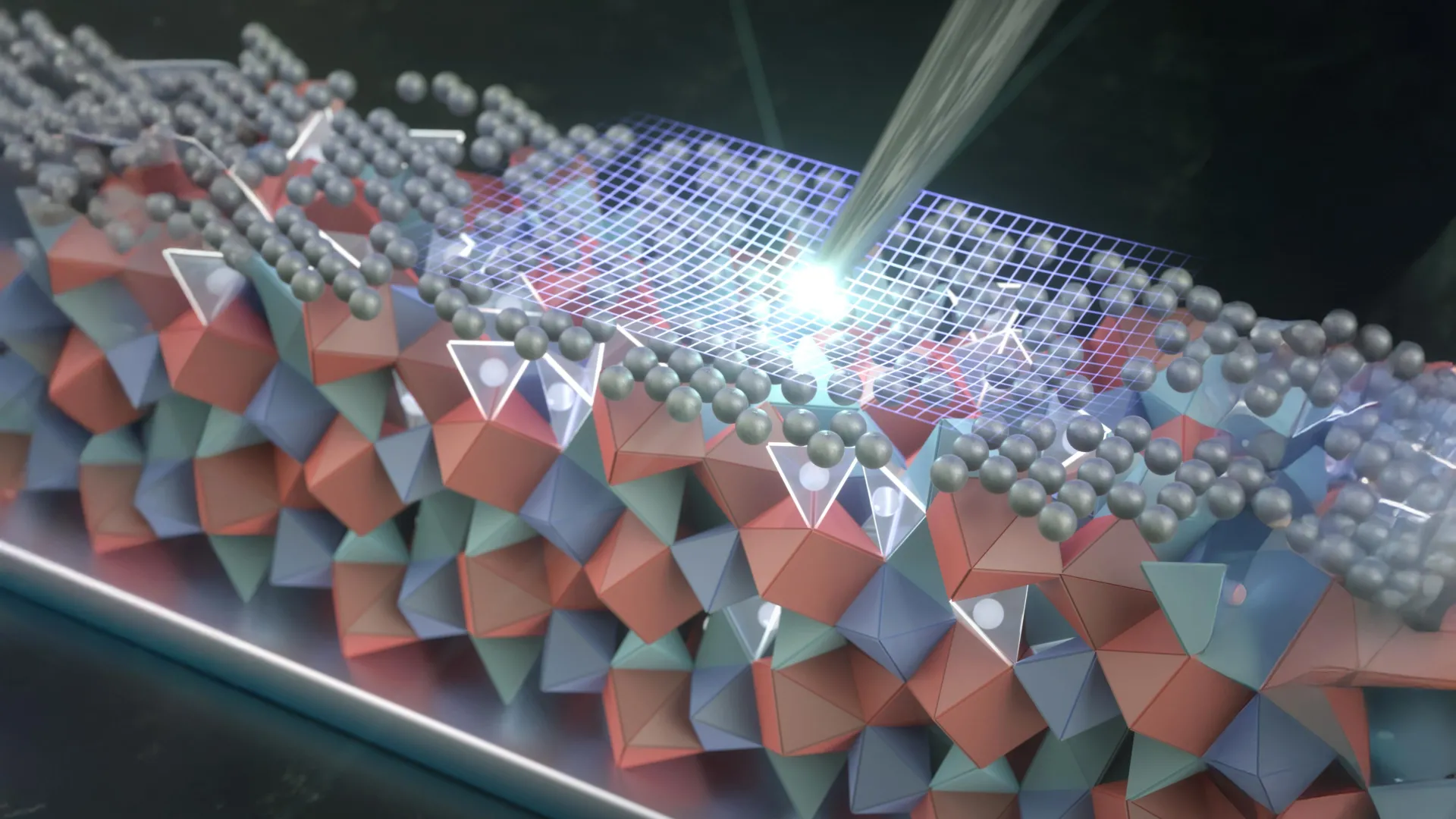

Stanford researchers report in Nature Materials (Jan 16, 2026) that a 3-nanometer Ag+ nanoscale coating, heat-treated to 300°C and penetrating 20–50 nm into LLZO solid electrolyte, makes the surface nearly five times more resistant to mechanical cracking and blocks lithium intrusion—key failure modes for solid-state lithium-metal batteries. The approach promises higher-energy, faster-charging, safer cells with potential application to EVs and sodium batteries and could ease lithium supply-chain pressure, but results are currently limited to small-area tests and scalability, integration into full cells and long-term cycle stability remain unproven.

Market structure: This nanoscale Ag+ coating is a disruptive enabler for ceramic solid electrolytes (LLZO class) that directly benefits solid‑state battery developers (e.g., QS, SLDP), advanced coating/equipment suppliers (VECO, AMAT), and specialty silver producers (PAAS, AG). Incumbent liquid‑electrolyte value chains (separator, graphite suppliers) risk slower demand growth if adoption accelerates; pricing power will shift to firms that control scalable coating IP and ALD/thermal processing at wafer‑scale. Near‑term supply/demand impact on silver is marginal; adoption at scale (EV fleet share >20% by 2030) could add low‑single‑digit % to silver demand annually, but manufacturing capex and ceramic raw materials (La/Zr) are the nearer constraints. Risk assessment: Primary tail risks are technical scaling failure (lab result not reproducible at cell level), adverse electrochemistry when Ag+ interacts with real cathode/anode stacks, and IP/licensing disputes that bottleneck commercialization. Time horizons: immediate (days) — negligible market move; short (3–12 months) — partner announcements, pilot cells and patent filings; long (2–7 years) — potential commercial EV/consumer rollout. Hidden dependencies include stack pressure management, manufacturability of 3 nm uniform coatings across large-area cells, and recycling/end‑of‑life chemistry; a silver price >30% YoY would meaningfully raise per‑kWh cost if coating mass scales. Trade implications: Size disciplined, asymmetric bets: favor equipment suppliers (VECO, AMAT) and selected solid‑state developers (QS, SLDP) via limited exposure — use long‑dated options to cap downside. Consider small tactical silver exposure (PAAS) as a low‑conviction hedge only if pilot scaling signals appear within 12 months. Sector rotation: reduce cyclical exposure to graphite/standard separator OEMs if multiple manufacturers announce commercial solid‑state pilot lines in 12–24 months; shift toward materials‑processing, semiconductor‑style capital‑equipment names. Contrarian angles: Consensus will overestimate silver raw‑material importance and underestimate manufacturing scale and IP barriers; market may be underpricing multi‑year integration risk (software of materials). Historical parallels: ceramic electrolyte breakthroughs (2000s) promised fast moves but took >7–10 years to commercialize; unintended consequences include harder recycling streams, new single‑source suppliers and concentrated pricing power. Trade accordingly — small, option‑capped exposure pending reproducible cell‑level data (>=500 cycles at fast‑charge conditions) within 12 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.35