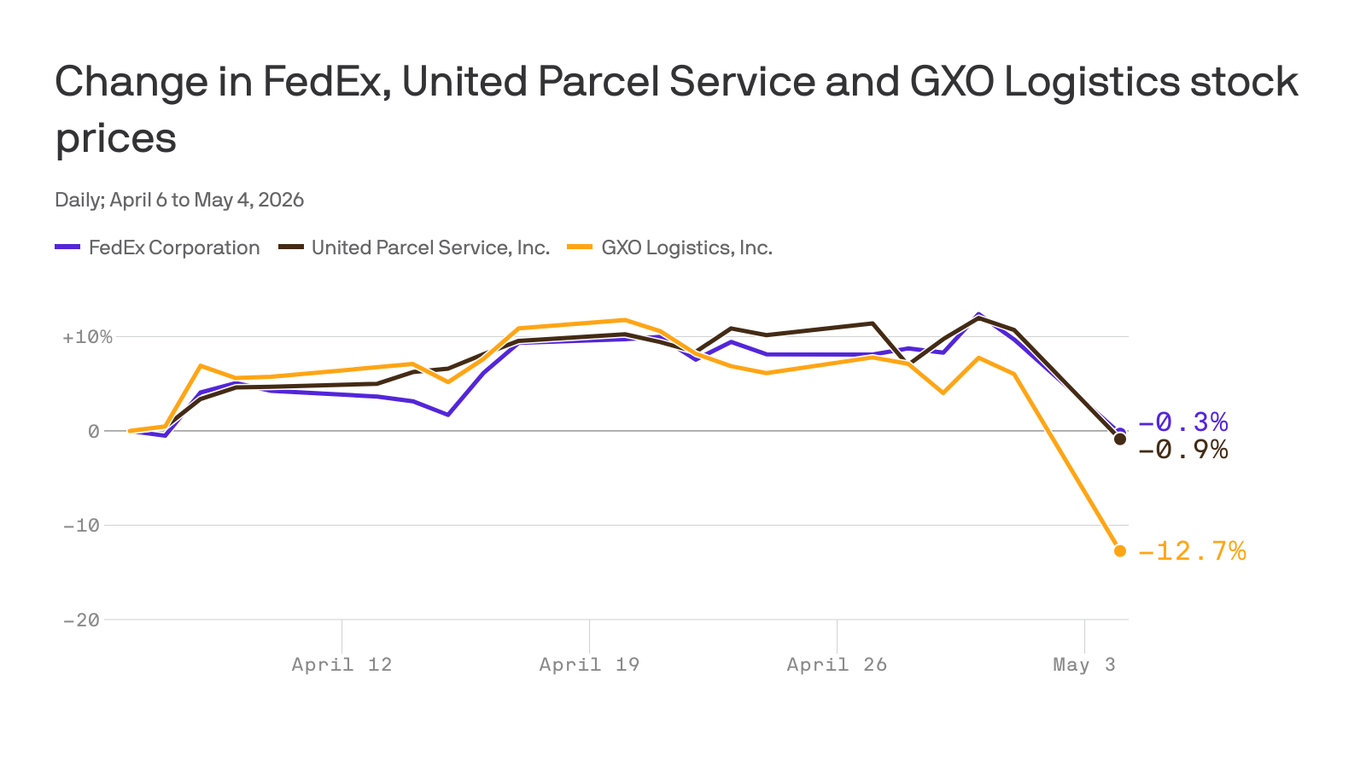

Amazon is expanding its distribution, parcel shipping, and fulfillment services to outside businesses, positioning itself as a direct competitor to UPS, FedEx, and other logistics firms. The move builds on Amazon’s existing network, which was already just behind UPS in U.S. parcels handled in 2024 and is projected to reach No. 1 by 2028. Shares of UPS and FedEx fell after the announcement, while Amazon rose 1.4%.

This is less a single-product launch than a strategic tariff on the logistics industry’s economics: Amazon is weaponizing density, routing data, and capital intensity to compress the serviceable margin pool in parcel delivery. The immediate share reaction in incumbents likely understates the second-order impact on contract renewal pricing, because shippers will now benchmark against a vertically integrated network that can cross-subsidize lower-margin freight with retail and cloud cash flows. That makes the threat more pronounced in e-commerce, SMB, and suburban final-mile lanes than in legacy enterprise or industrial freight. The key medium-term implication is not volume loss overnight, but mix erosion. UPS and FDX can probably defend headline parcel count for several quarters, yet the higher-margin portions of their networks are exposed if Amazon becomes the preferred architecture for businesses that value speed over brand neutrality. If Amazon can convert even a low-single-digit share of third-party shipper volume into its own stack over the next 12-24 months, it pressures yield, utilization, and labor leverage across the sector—especially in air express and time-definite services where fixed-cost absorption matters most. The counterpoint is that Amazon’s service will face trust, interoperability, and peak-season execution hurdles before it becomes a true universal logistics layer. Many non-marketplace shippers will hesitate to hand strategic distribution data to a direct competitor, and that friction could cap adoption outside of lower-sensitivity categories. So the selloff in incumbents may be too linear near term, but the strategic read-through is real: the multiple compression risk for asset-heavy logistics names has widened because the market is now pricing a longer runway of structurally lower pricing power. On positioning, the best risk/reward is relative value rather than outright momentum shorts, because Amazon’s monetization curve will likely be gradual while sentiment can overshoot. The setup favors owning the platform winner and fading the most exposed incumbents where e-commerce share and network overlap are highest; the cleaner the Amazon density, the worse the economics for competitors.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly positive

Sentiment Score

0.15

Ticker Sentiment