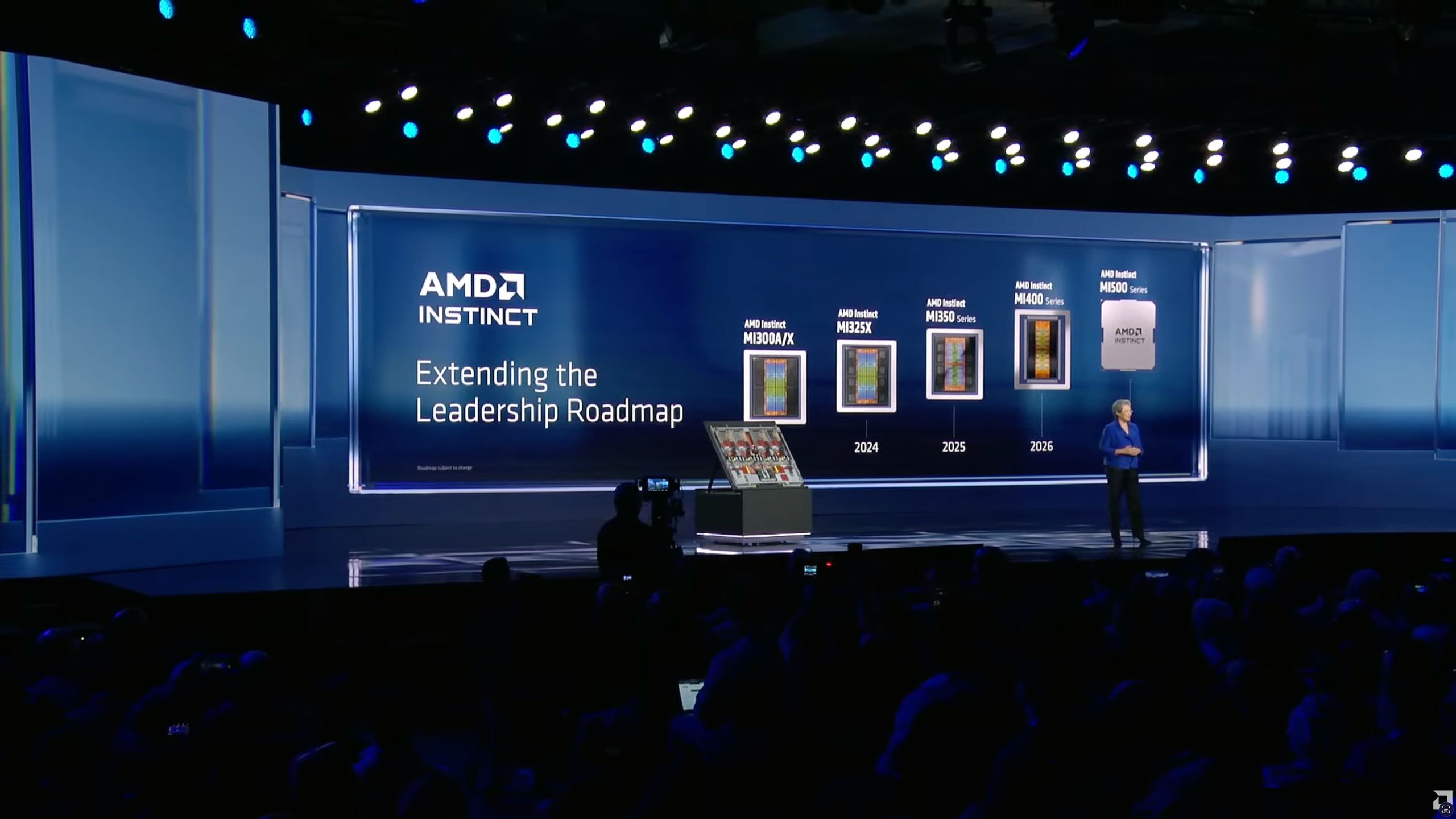

AMD disclosed the Instinct MI500X accelerator family slated for 2027, built on a next‑gen CDNA 6 architecture, manufactured on TSMC's 2nm (N2‑series) process and using HBM4E memory, and claimed up to a 1,000x AI‑performance uplift versus the MI300X without providing detailed benchmark definitions. The roadmap targets the coming multi‑yottaFLOPS data‑center demand and implies significant gains in compute density and performance‑per‑watt via new ISA, memory and process advances, but the long timeline and undefined comparison metrics limit immediate near‑term revenue or earnings visibility.

Market structure: AMD’s MI500 roadmap shifts value toward fab-capable ecosystems (TSM) and high-bandwidth memory suppliers; winners are AMD (AMD) if execution is clean, TSM (TSM) for N2 capacity, and HBM4E vendors. Losers: incumbents that rely on older nodes or software lock-in (customers tied to alternative accelerator stacks) may face pricing pressure; margin compression is possible for slow adopters. Demand signal: AMD’s 1000x claim implies a step-change in training/inference demand — plan for >2x annual growth in hyperscaler GPU spend 2027–2029 if claims hold, stressing foundry and HBM supply chains. Risk assessment: Tail risks include TSMC N2 yield shortfalls, US/China export controls restricting advanced node sales, or AMD failing software/ecosystem parity — any of which could halve upside. Immediate (days) reaction will be sentiment-driven; short-term (weeks–months) depends on bookings/partnerships; long-term (2027+) depends on TSMC allocation and software adoption. Hidden dependencies: HBM4E capacity, interconnect standards, and customer certifications; a single large hyperscaler deciding between vendors can swing share by ±20%. Trade implications: Direct long exposure to AMD and TSM is asymmetric: AMD captures product upside, TSM captures structural foundry pricing; prefer concentrated option-based exposure to AMD around 18–30 month horizons to cap downside. Pair trades: long AMD vs short NVDA (or long AMD/short incumbent accelerator ETF) to express share shift while hedging market beta. Cross-asset: stronger AMD/TSM execution supports commodity cycle for advanced substrates and raises tech credit spreads; short-dated bond yields may tick higher if capex guidance ramps. Contrarian angles: The market may be underpricing execution and supply constraints — the 1000x is likely marketing and will require selective workloads and memory configurations, slowing broad adoption. Reaction may be overenthusiastic near announcements and underestimates regulatory risk; history (GPU architecture transitions) shows multi-year share shifts, not instant flips. Unintended consequence: hyperscalers could consolidate on a single vendor to avoid integration cost, limiting multi-vendor upside for AMD despite product superiority.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment