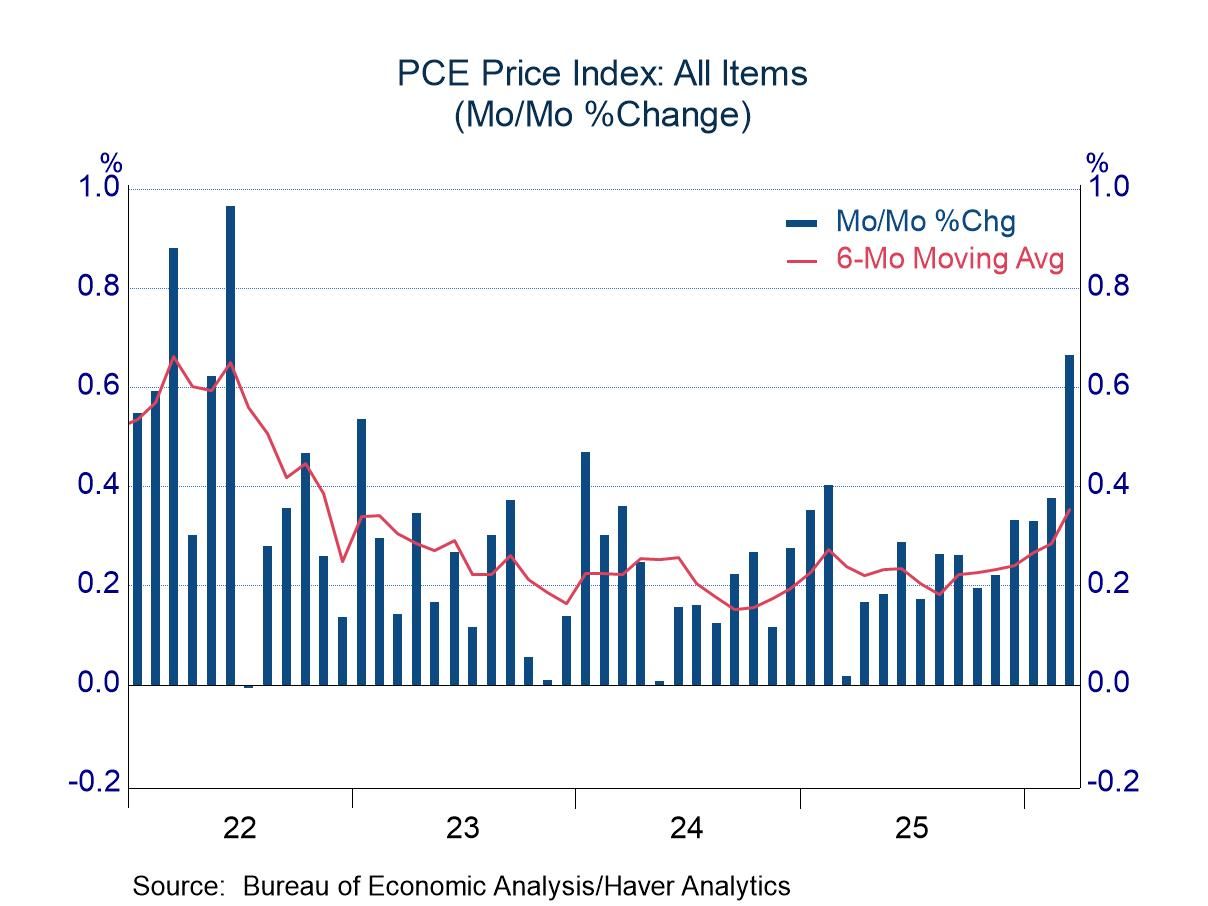

March PCE inflation jumped 0.7% m/m as energy prices surged 11.6%, lifting headline PCE to 3.5% y/y from 2.8% in February. Core PCE rose 0.3% m/m and accelerated to 3.2% y/y, remaining well above the Fed’s 2% target and reinforcing a hawkish policy backdrop. Personal consumption increased 0.9% m/m nominally, but real PCE rose only 0.2% after inflation.

This is a stagflationary mix that matters more for rates than for the next equity print: nominal spending is being flattered by an energy pass-through while real consumption is barely positive, which means household demand is not accelerating on a clean ex-energy basis. That tends to compress the window for the Fed to pivot toward easing and raises the bar for disinflation evidence over the next 1-2 CPI/PCE releases. In other words, the market should treat this as a higher-for-longer signal, not just a one-month noise event. The second-order loser is discretionary retail and any consumer-credit sensitive segment that relies on volume growth rather than pricing power. If real income is already slipping while gasoline and utilities are taking a larger share of wallet, the pull-forward in Q2 demand can fade quickly into lower-ticket weakness, worse mix, and more promotional activity. That is especially punitive for lower-income cohorts and for lenders exposed to near-prime revolving balances, where a small deterioration in real disposable income can show up first in delinquencies with a 1-2 quarter lag. The geopolitical overlay also matters: energy-driven inflation is the kind of shock that can be reversed abruptly if the conflict risk premium fades, so the right framing is not to chase a durable inflation regime shift, but to respect near-term upside in breakevens and rate volatility. For rates, the key risk is not just a sticky core print; it's that the Fed's reaction function becomes more asymmetric if energy keeps the headline elevated while real consumption softens. That combination is typically bearish duration until the market gets a cleaner labor or inflation break. JPM is not a direct loser from the data, but the mix is marginally negative for consumer credit quality and card spend growth over the next quarter if real incomes keep eroding. The more interesting implication is relative: banks with stronger trading and treasury exposure should outperform lenders with heavier unsecured consumer books if gasoline stays elevated and the macro tone turns more defensive. The consensus may be overfocusing on the headline inflation pop and underweighting the fact that real consumption is only barely holding up. If energy normalizes, the inflation scare can unwind quickly; if it does not, the more durable trade is not long inflation beta per se, but short consumer cyclicals and long rate volatility. The asymmetry favors fading complacency in front-end rates rather than making a big directional bet on broad growth.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.15

Ticker Sentiment