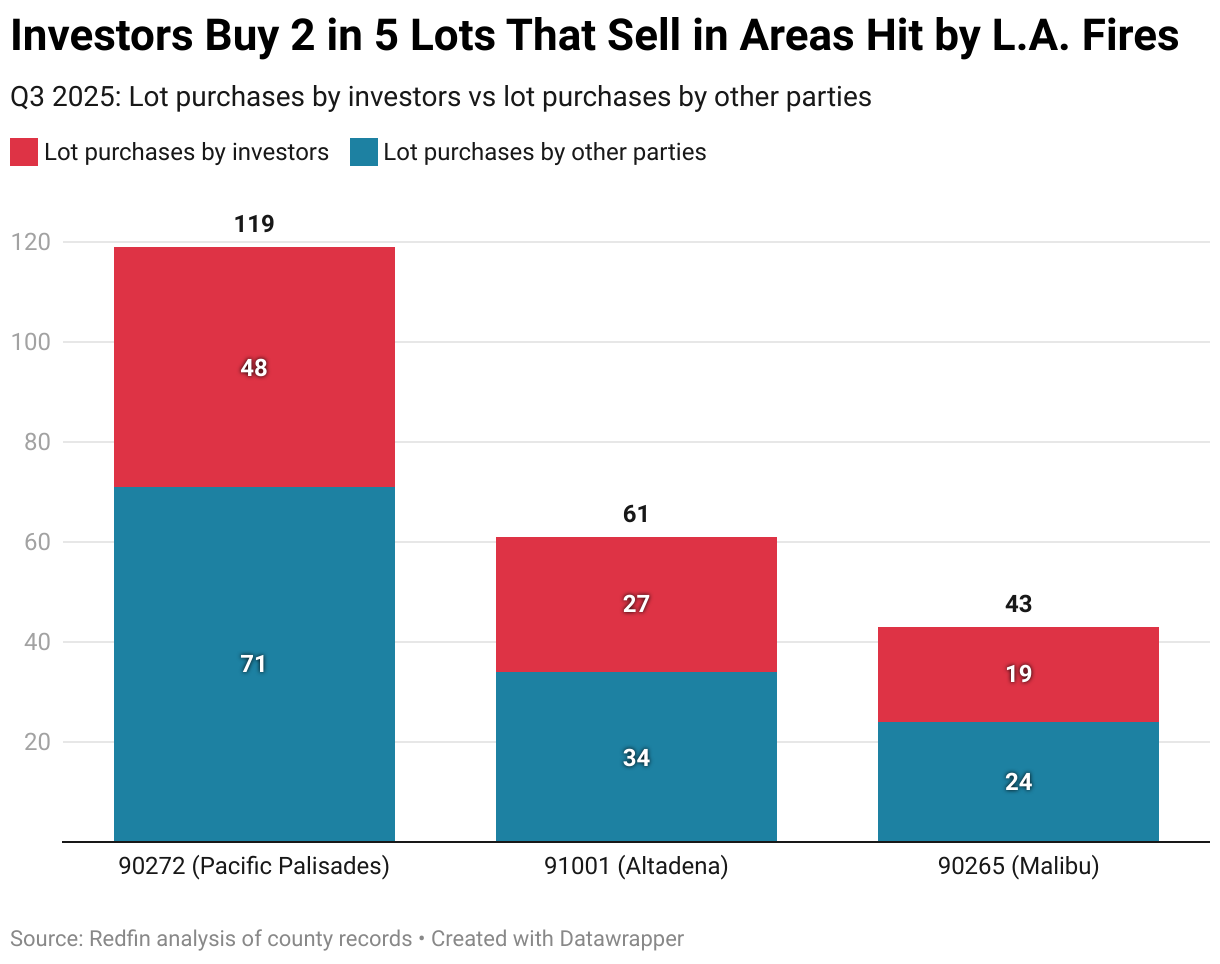

Investors have purchased roughly 40% of vacant lots sold in three Los Angeles–area zip codes hit by the January 2025 wildfires, with Q3 investor lot buys including 48 of 119 lots in 90272 (40.3%), 27 of 61 in 91001 (44.3%) and 19 of 43 in 90265 (44.2%); Redfin found about 80% of those lots previously hosted homes. Listings of vacant lots have surged year-over-year—Pacific Palisades 309 vs. 7 a year earlier, Altadena 225 vs. 2 and Malibu 214 vs. 125—putting downward pressure on prices and prompting cutbacks; typical recent lot sale prices were $1.6M (Palisades), $510k (Altadena) and $1.3M (Malibu). Single-family sales remain below pre-fire levels, insurers are tightening coverage with premiums up 35–50%, and many homeowners—particularly underinsured or elderly—are accepting lowball investor offers rather than rebuilding, creating localized distress and investor redevelopment opportunities.

Market Structure: Investors buying ~40% of lots in Pacific Palisades/Altadena/Malibu (Q3 2025) shift inventory from ruined SFRs to vacant-land supply, producing a localized glut (lot listings: Palisades 309 vs 7 YoY; Altadena 225 vs 2). Winners: building-material retailers (HD/LOW), modular/manufactured-home suppliers, and small-cap flippers that can execute fast rebuilds; losers: underinsured homeowners, local insurers facing rising claims and reinsurers exposed to CA wildfire risk. Price signaling: lot comps show 50%+ haircut versus intact-home basis (Altadena lot $510k vs replacement house >$1M), implying substantial value recovery depends on rebuild economics and insurance availability. Risk Assessment: Tail risks include regulatory action (insurance premium caps, moratoria on development, or government buyouts) and a renewed high-fire year that forces lenders to tighten mortgage/fire-coverage requirements; either could depress demand and create a 20–40% further mark-down in lot values within 6–12 months. Short-term (weeks–months): volatility around permit issuance and expiration of temporary rental coverage (which will force more sellers to transact). Long-term: chronic insurance de-risking could shrink buyer pool for risky coastal lots for years, converting some parcels to long-term distressed inventory. Trade Implications: Tactical plays favor suppliers and remediation beneficiaries (long HD/LOW, selective aggregates MLM/VMC) and hedges against insurers (buy puts on ALL/PGR, 3–9 month tenors). Pair trades: long building-supply retailers vs short large-cap personal-lines insurers to capture rebuild demand vs underwriting pain. Real-estate private-opportunity: selectively JV on Altadena lots priced <$600k where pre-fire home comps exceed $1M, target >18% IRR if permits within 9–12 months. Contrarian Angles: Consensus focuses on doom for local housing, but high-net-worth demand in Palisades shows resilience — wealthy owners are paying >$3M to reposition, supporting a two-tier recovery (luxury rebound vs middle-market squeeze). Historical parallel: post-disaster pockets (e.g., post‑Katrina high-end enclaves) recovered faster once insurance/reinsurance repriced; if CA insurers materially raise premiums (already +35–50%), capital will flow into rebuild plays not into owner-occupied SFRs. Unintended consequence: investor lot accumulation could create multi-year rental demand and construction pipeline, benefiting suppliers while capping lot price upside.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.40