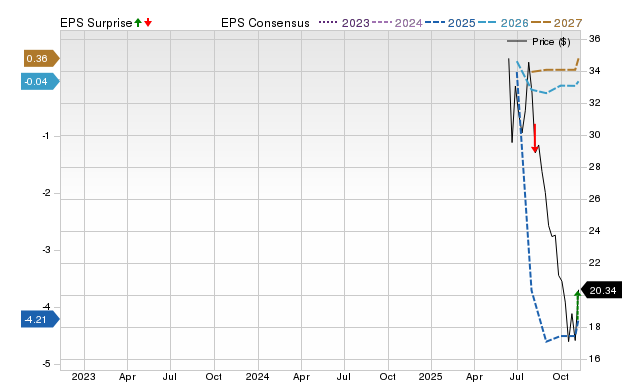

Chime Financial (CHYM) closed at $20.17 and the mean Wall Street price target is $30.47, implying a 51.1% upside, based on 15 short-term targets (standard deviation $7.86; range $17.00 to $40.00). Zacks notes a 4.3% upward revision to the current-year consensus EPS over the past month (three up, one down) and assigns CHYM a Zacks Rank #2 (Buy), signaling analyst optimism, though the piece cautions about the reliability of price targets and variability among estimates.

Market structure: A renewed analyst-led bid (mean PT $30.47, +51% vs $20.17) concentrates flows into CHYM and benefits fintech payment rails (V, MA) and cloud core banking vendors (FIS, FISV) via higher volumes; losers are smaller regional banks that compete on deposits if Chime re-accelerates user growth. The standard deviation $7.86 and 15-estimate spread (17–40) implies high positioning dispersion — expect choppy liquidity and periodic 15–30% intraday moves as sentiment shifts. Risk assessment: Tail risks include CFPB/regulatory enforcement, a funding shock if partner bank relationships fracture, or an earnings miss that reverts the +4.3% EPS revision trend; each could trigger >40% drawdowns. Time horizons: immediate (days) driven by sentiment/flows, short-term (3–6 months) driven by upcoming earnings and deposit metrics, long-term (>12 months) depends on sustainable NIM and CAC/LTV economics. Trade implications: For directional exposure prefer defined-risk structures (6–9 month call/debit spreads) to capture the consensus to $30 while capping downside; size initial exposure to 2–3% portfolio for longs and hedge with short-dated protection. Relative/value: pair long CHYM vs short legacy regional bank ETF (KRE) or debit-card-centric peer (AFRM) to isolate neo-bank execution vs macro margin compression. Contrarian angles: Consensus ignores unit economics sensitivity to rates and interchange repricing — a 50bps NIM contraction could erase near-term profitability and justify sub-$15 levels; conversely, conviction in product-led deposit growth would validate >$30. Historical parallels: past neo-bank re-ratings (SOFI, LU) show rapid reversals around regulatory headlines; don’t assume steady uphill path.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately positive

Sentiment Score

0.35

Ticker Sentiment