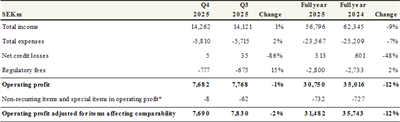

Handelsbanken reported Q4 2025 operating profit of SEK 7,682m (Q3: 7,768) and full-year operating profit of SEK 30,750m (2024: 35,016), with ROE at 13.0% and EPS 11.98 SEK (2024: 13.86). Margin compression from lower market rates weighed on net interest income, but the bank highlighted continued savings AUM growth, improved cost efficiency (expenses down ~7% year-on-year), and eight consecutive quarters of net credit loss reversals; CET1 stood at 17.6% and the Board proposes a raised total dividend of SEK 17.50 per share (2024: 15.00). The update signals resilient capital and credit metrics amid weaker earnings, supporting a cautious but stable investor view.

Market structure: Handelsbanken’s report points to winners being high‑quality, well‑capitalised retail banks (Handelsbanken: SHB A/B) and asset managers benefiting from AUM inflows; losers are smaller regional lenders with thinner CET1 buffers and higher NIM sensitivity. Short‑term margin pain from lower market rates is offset by rising fee income and lending growth in under‑penetrated UK/NL markets; expect modest market‑share gains in those geographies over 12–24 months if lending momentum continues. Cross‑asset: expect modest compression in Handelsbanken senior spreads and relative resilience in SEK; bank equities may diverge — high‑quality names outperform lower‑rated peers, while covered bond spreads stay tight. Risk assessment: Key tail risks include a UK/NL deposit run or CRE shock that erodes CET1 by >150–250bp, or regulatory hikes forcing capital conservation; set a hard watch threshold if reported CET1 falls below 16.0% (from 17.6%). Immediate (days): dividend confirmation and annual report releases; short (1–3 months): NIM trajectory and Q1 lending growth; long (12–36 months): sustainability of AUM inflows and return on equity with higher capital. Hidden dependency: fee growth is market‑sensitive — a 10% drop in equity/IR markets could cut AUM fees meaningfully and amplify NIM effects. Trade implications: Direct: establish a modest 2–3% net long allocation to SHB A/B (OMX: SHB A/B.ST) within 10 trading days to capture dividend (SEK17.50) and post‑report re‑rating, target 12‑month upside 15–25%, stop‑loss 12%. Pair: go long SHB vs short SEB (OMX: SEB A) or Swedbank (OMX: SWED A) 1:1 notional to play capital quality dispersion; rebalance after April 22 interim. Options: buy a 6–9 month call spread on SHB (long ATM, short +20%) to cap premium while capturing post‑report upside. Fixed income: buy 3–5y SHB senior bonds if 5y spread >40bp over government, target carry + spread tightening. Contrarian angles: Consensus may underprice sustained fee/AUM growth and overestimate permanent NIM erosion — history (post‑rate cuts) shows NIM recovers over 12–24 months with volume and repricing. Conversely, the market could underreact to the dividend hike as signalling capital return flexibility; if CET1 compresses under 16% the market will re‑rate downwards quickly. Unintended consequence: high capital targets cap long‑run RoE, so prefer structured equity (call spreads) to capture upside with defined risk.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.12