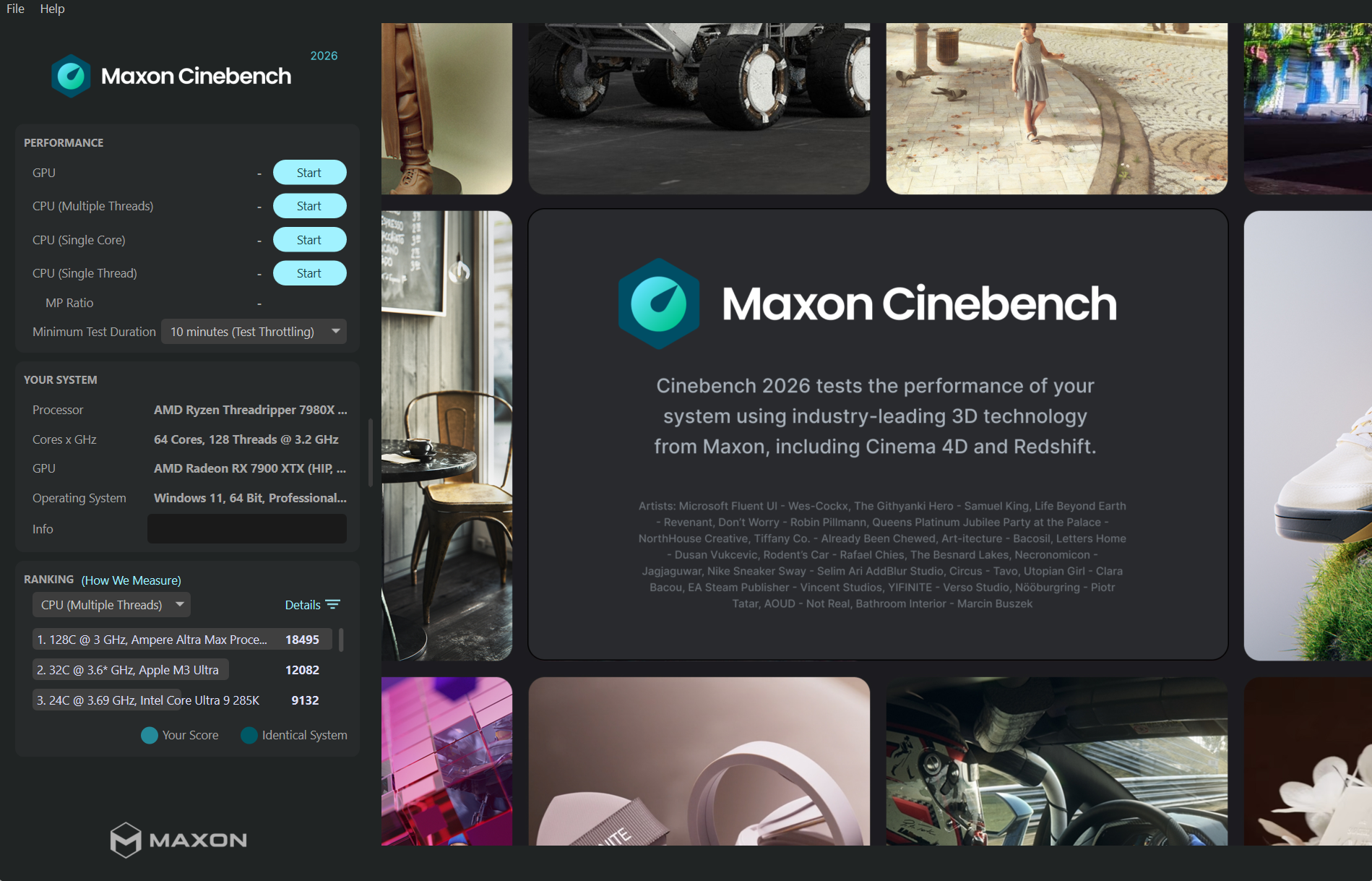

Maxon released Cinebench 2026, integrating the latest Redshift engine that the company says is roughly six times more demanding on multi-threaded tests versus the prior version, and adds a new SMT core test to evaluate SMT performance. The update expands hardware support (including Nvidia Ampere Altra, Hopper, Blackwell GPUs, AMD Radeon Pro, and Apple M4/M5 chips) but excludes Intel GPUs; GPU tests now require ≥8GB VRAM (16GB unified memory on M-series Macs), and supported OSes are Windows 10/11 and macOS 14.7+. The release improves real-world rendering parity for 3D workflows but is unlikely to be materially market-moving beyond niche hardware and software vendor relevance.

Market structure: Cinebench 2026 materially raises multi-thread and GPU VRAM thresholds (>=8GB GPU, 16GB unified on Apple), favoring vendors with high-end GPUs and workstation sales — primarily NVDA and AMD — and increasing pricing power on pro GPUs and memory components over the next 3–12 months. Intel is a clear near-term loser because Redshift omits Intel graphics, risking share loss in content-creation benchmarks and OEM workstation spec decisions. This should modestly lift ASPs for pro GPUs and VRAM-priced components, tightening supply/demand for 8GB+ cards in Q1–Q3 2026. Risk assessment: Tail risks include benchmark gaming/marketing distortions and a rapid industry pivot to cloud-rendering that would blunt hardware demand; supply shocks (VRAM shortages) could produce >10–20% price swings for cards in 1–6 months. Immediate effects (days–weeks) are review re-rankings; procurement and OEM refresh cycles drive the 1–6 month demand lift; structural CPU/GPU share shifts play out over multiple quarters. Hidden dependency: software support (Redshift) dictates platform competitiveness more than raw silicon for creators. Trade implications: Direct plays — overweight NVDA (2–3% portfolio) and AMD (1.5–2%) to capture pro GPU demand; small short/defensive on INTC (0.5–1%) to express lost GPU relevance. Options: buy 3–6 month call spreads on NVDA/AMD targeting delta ~0.35–0.45 and enter while implied vol <40%; buy a 3-month put spread on INTC if IV <30% to limit cost. Entry window: act within 2–6 weeks; trim/ reassess after two quarterly reports or a >15% move. Contrarian angles: The market may underprice Apple M‑series upside for CPU-only workloads despite unified memory hurdles; conversely, the VRAM/16GB bar could accelerate cloud-render adoption (reducing hardware TAM) — watch GPU used-market volumes and cloud rendering seat growth. Historical parallel: prior Cinebench engine jumps re-ranked CPUs short-term without changing long-term semiconductor CAPEX; don’t assume benchmark-driven ranking permanently shifts fundamentals without OEM demand evidence in next 2 quarters.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.27

Ticker Sentiment