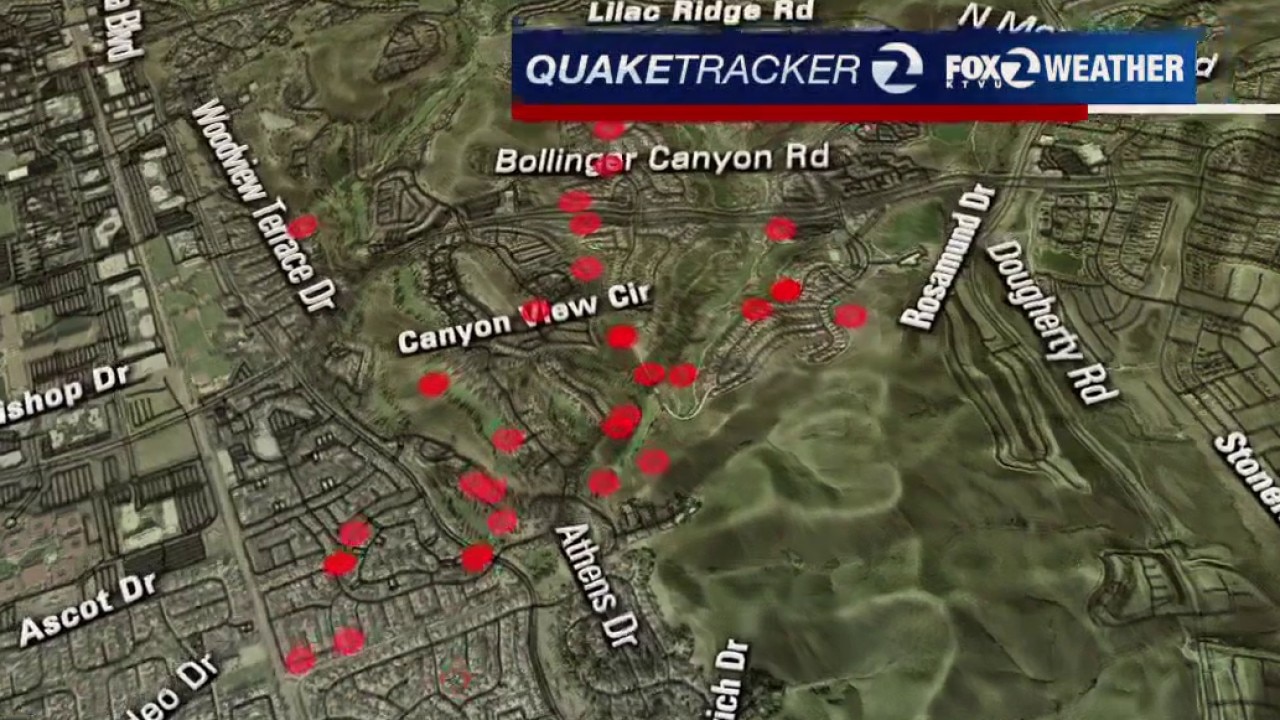

A swarm of at least 21 earthquakes struck San Ramon, Calif., on Monday morning with the largest measuring magnitude 4.2 at about 7:00 a.m.; other notable temblors included a 3.9, 3.7 and 3.3, and several smaller events around magnitude 2.0. The activity, attributed to the creeping Calaveras Fault which has produced roughly 300 quakes in the area since Dec. 1, 2025, produced widespread shaking across the Bay Area but no immediate reports of damage or injury. For investors, the episode is a localized geophysical risk that could affect property, insurers and infrastructure exposure regionally if the sequence escalates, but current impact appears limited and not market-moving.

Market structure: This swarm (largest M4.2, ~300 quakes in the zone since Dec 1, 2025) creates micro-demand winners — seismic retrofit/engineering firms (Jacobs J, AECOM ACM), construction-materials (Nucor NUE) and home-improvement retailers (HD, LOW) — who can capture short-to-medium term retrofit spend; losers are CA-concentrated property insurers and local REITs where indemnity costs or cap‑rate re‑rating can compress returns. Competitive dynamics favor specialist contractors with existing municipal/utility relationships; insurers with poor California diversification will face upward pricing pressure and reserve reviews. Cross-asset: immediate market impact is muted but expect small moves in insurer equity IV (+10–30% intraday on local losses), slight widening of CA muni credit spreads (~5–15bp if damage accumulates), and a modest bid to USD/UST as risk-off if a >M5.5 event occurs. Risk assessment: Tail risk is low-probability/high-impact — a triggered >M6.0 on a locked segment could produce multi-billion-dollar losses, a statewide regulatory retrofit mandate, and large insurer reserve hits; probability <5% in next 12 months but impact high. Time horizons: days — localized sentiment/stock IV spikes; weeks–months — insurer reserve repricing and retrofit contract awards; quarters–years — structural increases in building-code capital expenditure and insurance premiums. Hidden dependencies include tech-sector tenancy concentrations (office REITs) and mortgage servicing exposure to regional home-price shifts; catalysts are a >M5.5 quake within 30 days, official state emergency, or insurer loss-model updates. Trade implications: Tactical direct plays: small, disciplined positions — 1–2% long Jacobs (J) for 3–12 months to capture municipal retrofit contracts; 1% long HD or LOW for a 1–3 month trade capturing localized DIY/retrofit demand. Hedging: buy 3‑month 5% OTM puts on Travelers (TRV) and Allstate (ALL) sized 0.5–1.0% portfolio each to protect against a localized claims spike; consider a relative-value pair long NUE vs short VNQ (REIT ETF) to express construction demand vs property-cap-rate risk. Options: for a low-cost directional, buy J 3‑6 month 25–35% OTM call spreads sized to 0.5–1% portfolio exposure. Contrarian angles: Consensus will likely underprice cumulative swarm risk — markets treat this as one-off noise until frequency or magnitude steps up; if the swarm produces >10 quakes ≥M4.0 in 30 days or a single >M5.5, reprice could be sharp and persistent (insurer equity drawdowns 10–30%). The market may be slow to price regulatory fallout (mandatory retrofits), which benefits specialist contractors and harms broad REIT/insurance exposure; avoid large directional positions in national fixed income or equity indices until frequency/magnitude thresholds are tested. Historical parallel: post‑Loma Prieta code and retrofit spend unfolded over years — early, concentrated bets on engineering/retrofit contractors outperform generalized real‑estate long exposure over 12–36 months.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.00