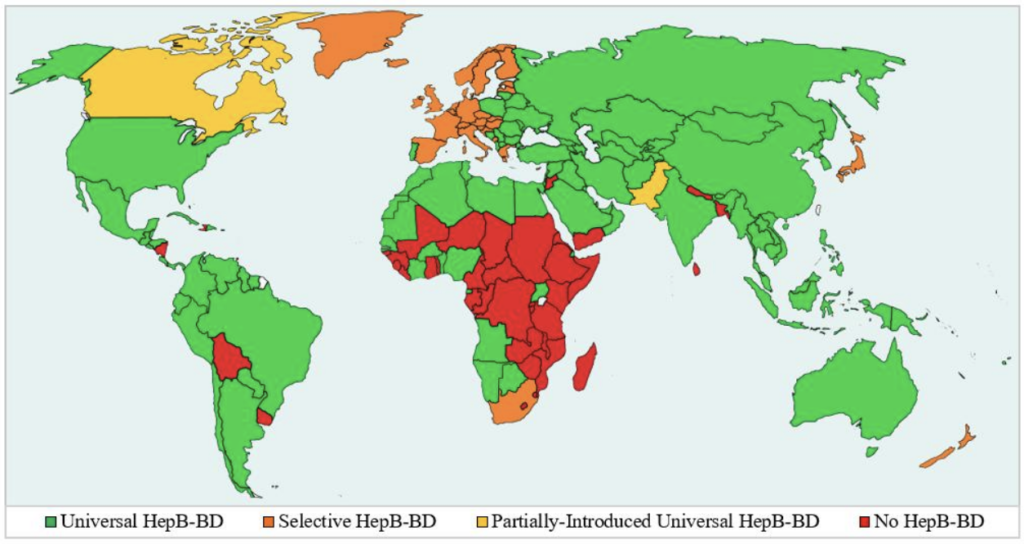

On Dec. 5 the CDC Advisory Committee on Immunization Practices voted to rescind the long-standing universal newborn hepatitis B birth‑dose recommendation, advising that mothers who test negative discuss vaccination with clinicians and that initial doses for infants not given a birth dose be delayed until no earlier than two months. The decision — by a reconstituted ACIP appointed by HHS Secretary Robert F. Kennedy Jr. — departs from a policy in place since ~1991 that coincided with a decline from an estimated 200,000–300,000 annual infections pre-vaccine to roughly 14,000 cases today; CDC data cited include ~640,000 adults with chronic infection (about half unaware), 90% risk of chronic infection for infected infants and ~25% eventual premature mortality among those infants. For investors, this is chiefly a regulatory and political development that could change vaccine demand dynamics and public‑health risk perceptions but is unlikely to produce significant near‑term market moves.

Market structure: The ACIP policy shift chiefly re-allocates timing of ~3.6M US infant vaccine administrations rather than destroys demand — at an estimated wholesale price of ~$15–25/dose that implies a maximum fiscal transfer of roughly $50–90M/yr away from hospital newborn channels (<<0.1% revenue for MRK/GSK). Winners are logistics/cold-chain providers if doses re-route to outpatient pediatricians; losers are hospital newborn-service lines and niche vaccine lot manufacturers that depend on predictable perinatal ordering cadence. Macroeconomic cross-asset impact is negligible; expect no material move in IG credit spreads or FX, but small-cap biotech/healthcare equities may see headline-driven volatility (+/-10–30% intramonth). Risk assessment: Tail risks include a localized outbreak forcing emergency procurement (plausible probability ~5–10% over 12–36 months) or a legal/regulatory reversal if federal courts/CDC reassert previous guidance (~10% within 12 months). Short-term (days–weeks) volatility will be driven by headlines and state-level guidance; medium-term (3–12 months) risk is policy whipsaw and litigation; long-term (2–5 years) epidemiologic effects depend on prenatal screening improvements and state uptake. Hidden dependencies: state public-health budgets, prenatal screening rates, and hospital discharge policy can either blunt or amplify demand shifts. Trade implications: Avoid making material fundamental bets on MRK/GSK (impact <0.05% of sales); instead trade volatility. Tactical trades: hedge healthcare beta with 1–2% notional 3-month put spread on IBB/XBI, short small-cap vaccine names likely to gap on headlines (e.g., DVAX) sized 0.5–1% with stop-loss, and modestly trim pediatric hospital operators (HCA) by 1–2% to capture small operational risk. Entry: implement hedges within 1–5 trading days; reassess on first formal CDC guidance document or any state-level mandate within 30–60 days. Contrarian angles: The market overestimates material commercial impact on big pharma — this is a logistic/timing shock, not demand destruction. A likely underappreciated outcome is state-level divergence: several states may keep birth-dose as standard, preserving local demand and creating regional winners; that implies idiosyncratic alpha in state-focused hospital operators and distributors. Historical parallels (vaccine schedule shifts) show policy reversals are common when disease signals rise — price small-cap option positions accordingly rather than large directional bets.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.00