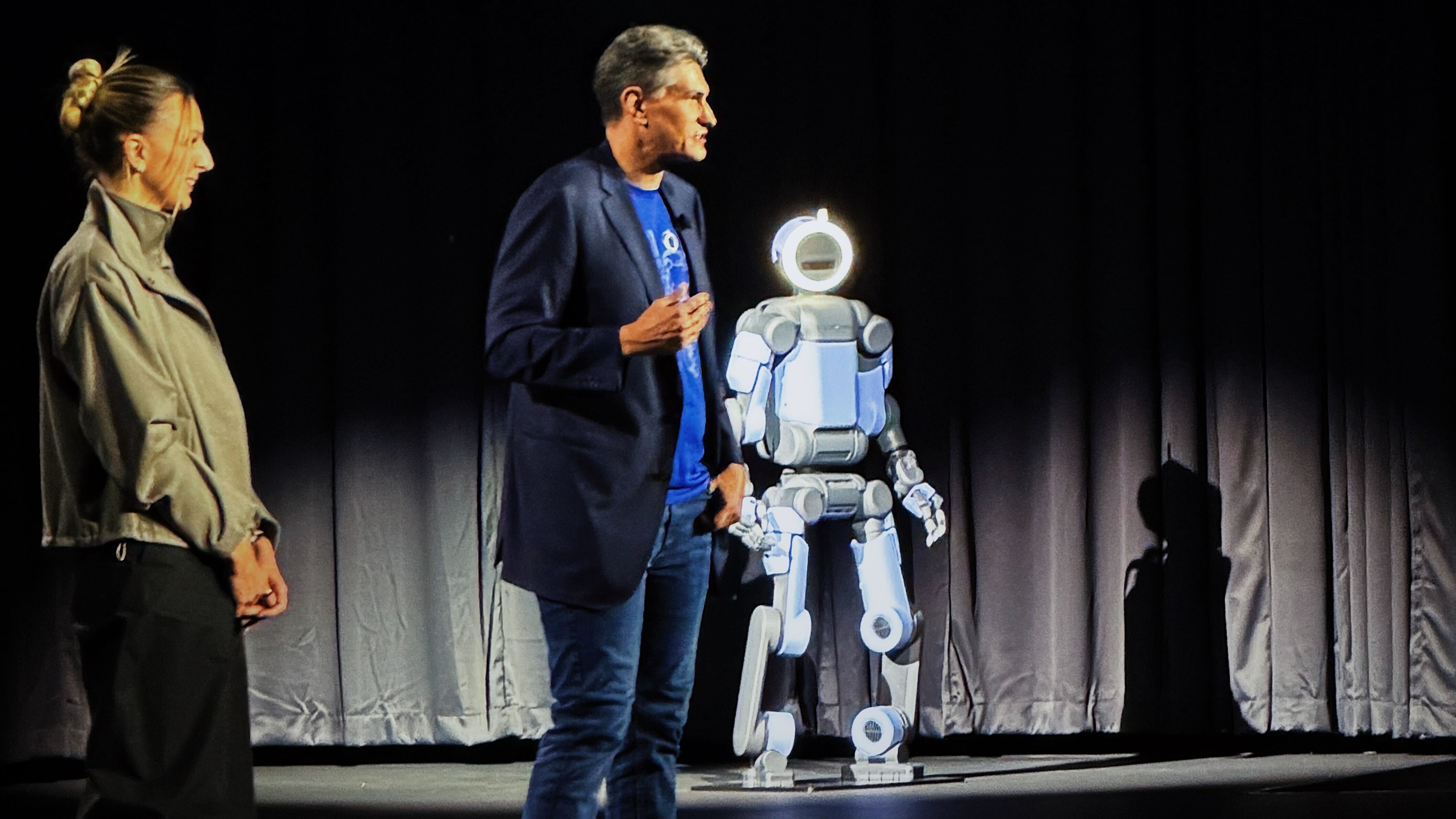

At CES 2026 Hyundai announced plans to begin using humanoid robots in its factories and is building a production system aimed at producing 30,000 robots annually by 2028. The initiative represents a major automation push that could alter Hyundai's manufacturing cost structure, drive incremental capital spending, and create a sizeable supply opportunity for robotics components and partners.

Market structure: Hyundai’s goal of 30,000 humanoid robots/year by 2028 creates a vertically integrated supplier that will (1) expand demand for semiconductors, sensors, motors and AI compute while (2) potentially undercut third‑party robot OEMs on price. Component winners include NVDA, ASML, KLAC and Nidec; potential losers are low‑end staffing firms (MAN) and niche robot resellers if Hyundai sells externally. The scale target is meaningful for a nascent humanoid market—enough to move component order books by mid‑2026 and depress ASPs for humanoid units by an estimated 10–30% by 2028. Risk assessment: Tail risks include regulatory limits (export controls or worker‑protection laws), high‑profile safety/cybersecurity incidents, and capex overruns that push ROI beyond acceptable ranges; each could reverse sentiment quickly. Immediate market moves will be muted (days), suppliers will reprice within weeks–months as purchase orders surface, and structural demand/efficiency effects will materialize over 2026–2028 as factories scale. Hidden dependencies: advanced chips, specialty motors and trained software stacks—chip shortages or sanctions (US/EU) would be acute bottlenecks. Trade implications: Favor semiconductor and equipment exposure (NVDA, ASML, KLAC) and industrial automation vendors with diversified customers (ABB). Reduce or short exposure to staffing/temp names (MAN) and smaller robotics pure‑plays that lack component control. Use option structures to express conviction: 12‑18 month call LEAPS on NVDA/ASML to capture ramping compute demand; small protective hedges on industrial longs given execution risk. Contrarian view: The market may overstate near‑term revenue from humanoids—Hyundai must prove per‑unit economics and reliability at scale; historical parallels (Foxconn’s automation promises) underdelivered. If Hyundai primarily internalizes robots for its own factories rather than selling them, robot OEMs’ revenue upside is limited while component suppliers still benefit; political backlash or safety incidents could slow deployments and create buying opportunities in beaten down suppliers.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.30