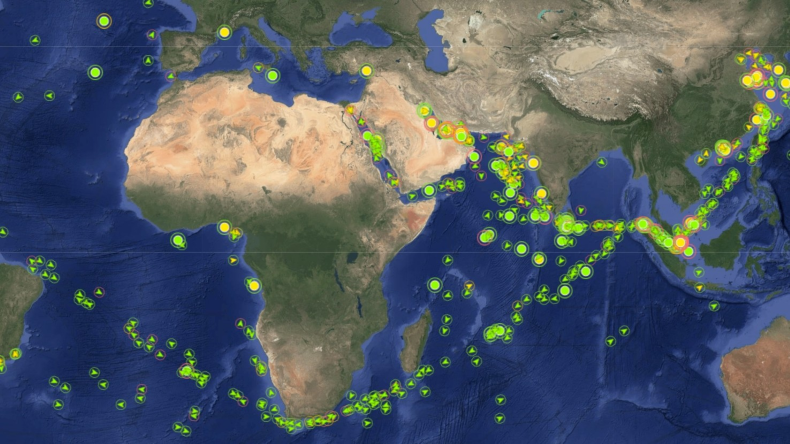

Seaborne crude exports excluding Iran jumped 15% week-on-week (+5.1m bpd) in the week to March 29, while Yanbu and Fujairah combined loadings reached 6.2m bpd (4.4m Yanbu, 1.8m Fujairah), roughly offsetting about half of Strait of Hormuz losses. Tanker rates are extremely elevated — the Baltic US Gulf–China VLCC index hit $167,120/day (+24% day-on-day, +59% since March 17) and MR product tankers are near $100,000/day — driven by a ‘scramble mode’ for cargoes. Key risk: if the Strait remains effectively closed demand destruction could follow; Deutsche Bank models imply Brent at $130–150/bbl if traffic normalises to 70% by June, or $170–190/bbl if not until November.

The immediate winners are those with direct spot exposure to VLCC/aframax earnings and flexibility to re-route (owners of modern, fuel-efficient VLCCs and MR product tankers). A non-obvious beneficiary class is pipeline-fed terminal operators and insurance brokers that extract fees from alternative loadings—these revenue streams scale with elevated replacement flows and are sticky once contractual policing and toll arrangements are embedded. Conversely, fixed-rate, long-term charter owners and asset-light logistics providers that cannot capture spot spikes will see underperformance versus spot-exposed peers as spread compression to replacement routes evolves. Timing and triggers cluster across two horizons. Over days-weeks, rate upside is sustained by routing frictions (canal transits, Panama bottlenecks) and last-mile speed premiums; over months the dominant driver flips to macroelasticity — sustained retail fuel pain will force refinery runs and cargo counts down. Key catalysts that would reverse the premium immediately are a credible, durable re-opening of Hormuz traffic or a diplomatic/insurance solution that materially lowers rerouting time; upside tail risks include escalation that knocks out both Hormuz and alternate chokepoints (Bab el Mandeb), which would extend the scramble phase and re-rate spot-dependent equities materially. Structurally, freight-market convexity favors owners who can both hoard vessels as floating storage and those with option-like exposure to spot (short-duration charterbooks, ownership of scrubber-equipped tonnage that trades at a premium). The consensus underweights the fragility of Atlantic uplift sustainability—Brazil/S. Atlantic liftings look margin-driven and likely to mean-revert within 6–10 weeks absent new upstream capex or policy shifts. That creates a window (1–3 months) where carefully sized directional exposure to freight and select names offers asymmetric upside, while downside is mean-reversion of rates tied to demand destruction beyond the 2–3 month mark.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mixed

Sentiment Score

0.00

Ticker Sentiment