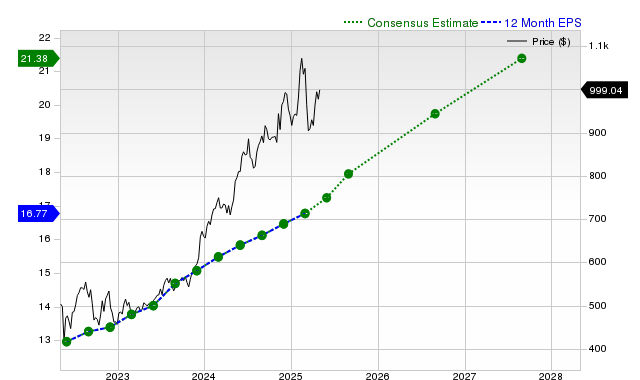

Despite recent underperformance, returning -1.7% over the past month against the S&P 500's +1.9%, Costco (COST) remains a trending stock with analysts forecasting robust earnings and revenue growth. The company is projected to see current quarter EPS rise 12.4% year-over-year to $5.79 and revenue increase 8.1% to $86.14 billion, with full fiscal year EPS estimates of $17.97 (+11.6%) and $19.84 (+10.4%) for the current and next periods, respectively, despite minor recent downward revisions to annual estimates. However, Costco holds a Zacks Rank #3 (Hold), suggesting near-term performance in line with the broader market, and its 'D' Zacks Value Style Score indicates it is trading at a premium compared to peers.

Costco (COST) presents a mixed outlook for investors, characterized by robust fundamental growth forecasts set against a premium valuation and recent stock underperformance. The company's shares have declined 1.7% over the past month, lagging both the S&P 500 composite's 1.9% gain and its peer group. Despite this, forward-looking estimates remain strong, with consensus projecting a 12.4% year-over-year increase in current quarter EPS and an 8.1% rise in revenue. Full-year fiscal estimates also point to double-digit EPS growth of 11.6% and 10.4% for the current and next fiscal years, respectively. However, these annual estimates have seen minor negative revisions of 0.4% over the last 30 days. This solid operational outlook, supported by a history of beating consensus estimates in three of the last four quarters, is counterbalanced by significant valuation concerns, as evidenced by a Zacks Value Style Score of 'D', indicating the stock trades at a premium to its peers. The resulting Zacks Rank #3 (Hold) suggests the stock is expected to perform in line with the broader market in the near term, implying the positive growth story may already be priced in.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

Neutral

Sentiment Score

0.00

Ticker Sentiment