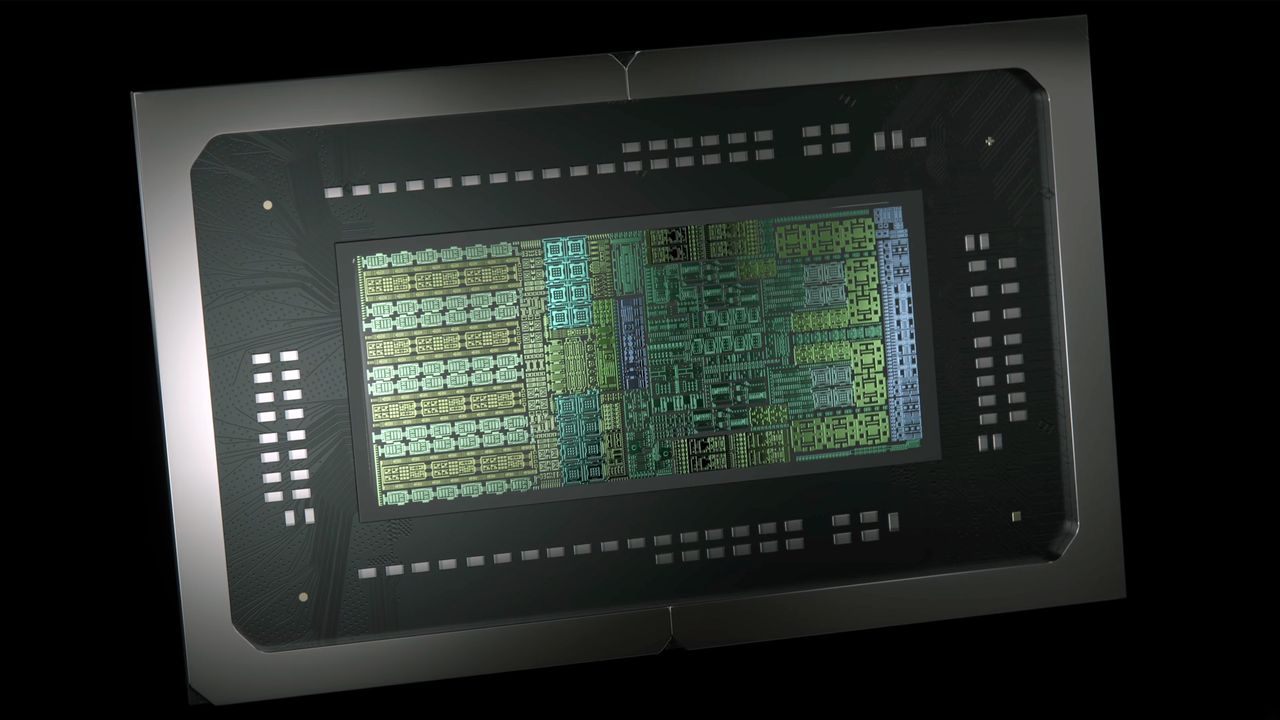

A leaked shipping manifest shows a Dell 16 Premium (later rebranded to XPS) listed with an “N1X ES2” engineering sample from November 2025, fueling speculation that Nvidia’s rumored N1/N1X ARM-based consumer chips — described as an RTX 5070-class GPU with 6,144 CUDA cores plus 20 Grace ARM cores and co-developed with MediaTek — may be deprioritized or cancelled for retail. The N1 silicon exists in enterprise form (GB10 Superchip in DGX Spark), but the apparent pullback or last-minute OEM rebrand suggests a strategic shift toward enterprise AI and partnerships (including Nvidia’s equity ties with Intel on x86 RTX SoCs), a development that matters for competitive positioning and OEM roadmap visibility but is unlikely to be market-moving in the near term.

Market structure: The apparent shelving/scaling-back of Nvidia’s N1/N1X product narrows the consumer ARM/GPU TAM and benefits incumbents focused on mobile SoCs (Qualcomm QCOM) and enterprise GPU/server chips (NVDA data-center SKU concentration). Dell (DELL) faces product-cycle execution risk and modest brand/retail sales pressure; Intel (INTC) could gain strategic leverage from its x86-RTX SoC partnership if OEMs pivot. Reduced consumer ARM GPU supply tightens near-term secondary-market pricing for discrete GPUs by ~5–15% and shifts incremental demand into data-center chips, supporting NVDA’s pricing power there despite headline weakness. Risk profile: Immediate (days) risk is sentiment-driven selloffs in NVDA/DELL; short-term (weeks–months) risk centers on product/partner disclosures (Jensen/Intel/Dell comments) and CES follow-ups; long-term (quarters–years) risk is structural — Nvidia reallocating N1 IP to enterprise could entrench server dominance but delay consumer diversification. Tail risks include regulatory scrutiny of Nvidia-Intel tie-ups and OEM defections to Qualcomm-led ARM platforms; a surprise Nvidia disclosure reversing cancelation would be a positive catalyst. Trade implications: Tactical opportunities include buying QCOM stock to play Windows-on-ARM momentum and hedging/shorting NVDA via options to express near-term disappointment while keeping exposure to its data-center franchise. Construct relative-value trades: long INTC vs short NVDA to capture potential OEM pivot to Intel x86 RTX SoCs; use 3–6 month horizons and explicit stop-losses. Manage size: keep directional positions small (0.5–2% of portfolio each) given high idiosyncratic risk. Contrarian view: The market may underappreciate that scrapping consumer N1X could improve NVDA margins if development reallocates to higher-margin data-center and AI IP — a path to stronger FCF in 2026–2027. Overreaction risk: a 15–30% NVDA dip would present a disciplined long entry aligned to data-center revenue growth; conversely, OEMs accelerating Qualcomm/ARM adoption is a slower, multi-year threat, not an immediate displacement.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25

Ticker Sentiment