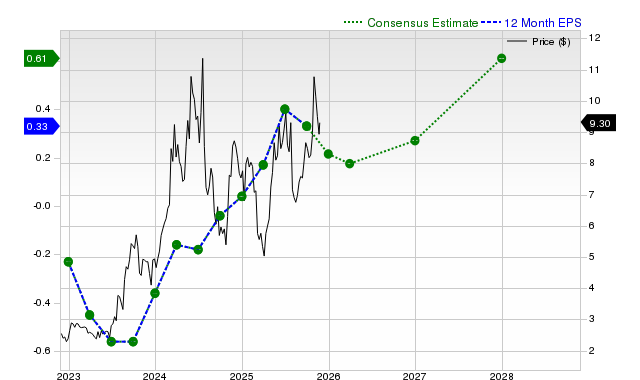

Orion Marine Group (ORN), a heavy civil marine contractor, has seen analysts sharply raise EPS forecasts: the current-quarter consensus is $0.05 (-68.8% YoY) with the 30‑day consensus up 133.33%, and the full-year EPS consensus is $0.19 (+26.7% YoY) after a 350% increase in revisions over the past month. The upgrades have pushed ORN to a Zacks Rank #2 (Buy) and shares have risen roughly 6.8% over the past four weeks, suggesting improving earnings visibility and positive investor momentum.

Market structure: Rising estimate revisions for Orion Marine (ORN) chiefly benefit ORN, its equipment suppliers (dredging/steel/fuel) and regional heavy-civil contractors who can win higher-margin port/coastal work; high-cost small subcontractors and overlevered peers are at risk as ORN gains pricing power. The 133% one‑month lift in the next‑quarter consensus and 350% full‑year bump (driven by a single raise) suggests demand improvement but is concentration‑dependent — expect modest spread tightening in high‑yield paper for stronger contractors and a 3–6% downward move in ORN implied vol if the beat continues. Risk assessment: Key tail risks are a reversal of the lone analyst revision (estimates fall >20%), contract delays from weather/regulatory holds, or a 200–500bp margin squeeze from rising input costs; any of these could trigger >30% downside. Timeline: immediate (days) = momentum; short (weeks–months) = earnings/contract announcements will validate revisions; long (12–36 months) = depends on sustained infrastructure funding conversion and backlog conversion rates. Hidden dependencies include customer concentration, seasonality, and working‑capital funding needs that can force dilution if cash flow lags. Trade implications: Tactical: establish a modest long (1–2% portfolio) in ORN with a 12–15% stop and a 30–50% upside target over 6–12 months if EPS revisions hold; finance with a 1–2% trim of long-duration tech exposure (e.g., reduce NVDA weight). Options: buy a 9–12 month call spread ~10–20% OTM to cap premium (max loss = premium) or buy cheaper 3‑month calls ahead of earnings only if IV < historical 90‑day realized vol + 20%. Pair trade: go long ORN and short small‑cap construction benchmark (IWM) size‑matched to isolate company outperformance. Contrarian angles: Consensus underestimates fragility — the recent revision came from one analyst so upside is binary: if ORN posts a sequential miss >$0.03 EPS or consensus falls 20% in 30 days, unwind immediately. The market may also be underpricing the upside: sustained backlog growth >15% and a 200bp margin expansion would justify re-rating; conversely, aggressive bid pricing to chase share could compress margins and force equity raises (dilution risk >10%). Historical parallel: 2017 contractor reratings post‑infrastructure headlines that reversed on margin slips — treat ORN as event‑driven, not secular, until two consecutive quarters validate the trend.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.35

Ticker Sentiment