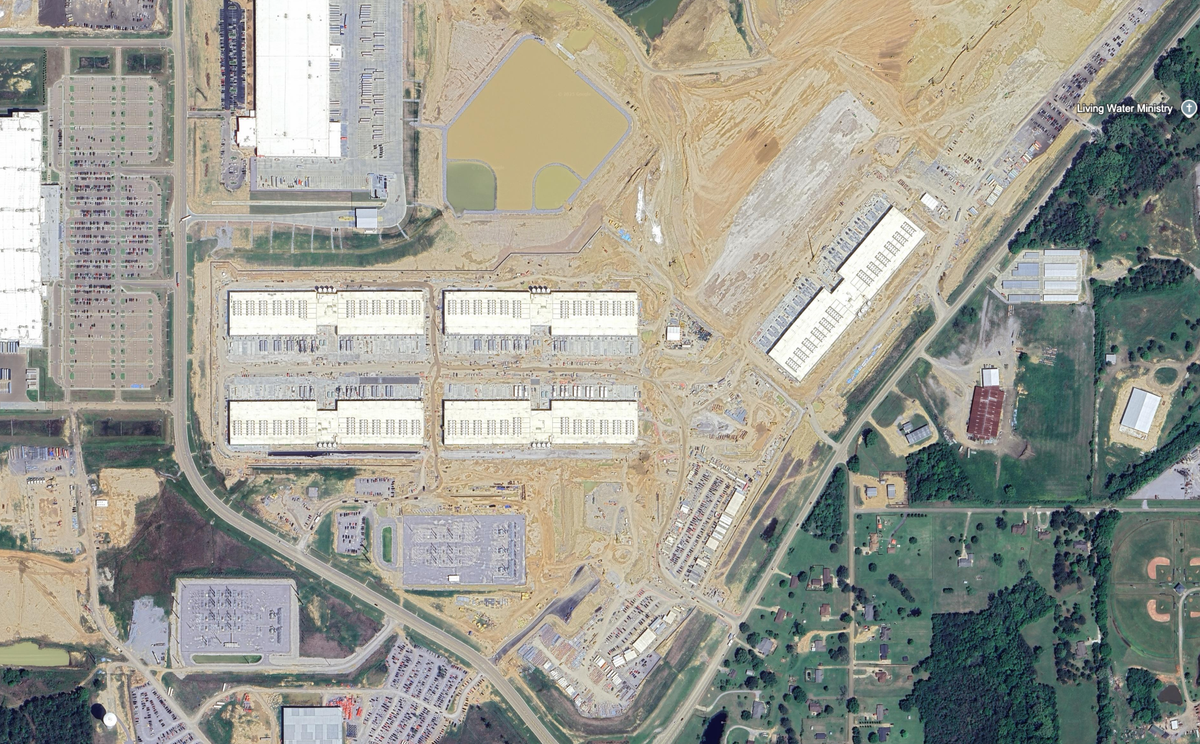

Epoch AI has created an open-source satellite-and-permits-based map of major U.S. datacenters, estimating metrics such as build cost and power usage (e.g., Meta’s Prometheus site at New Albany is tracked at $18 billion and ~691 MW; Epoch attributes xAI’s Colossus 2 to ~110,000 NVIDIA GB200 GPUs with gas turbine build-out across state lines). The effort — covering an estimated 15% of chipmaker-delivered AI compute as of November 2025 — provides near-real-time visibility into compute capacity, cooling infrastructure and permitting, with implications for hyperscaler capital deployment, regional energy demand, permitting/regulatory scrutiny, and ESG/water-use risk for utilities and real-estate/infrastructure investors.

Market structure: Big winners are NVIDIA (GPU pricing power), hyperscalers/cloud providers that monetize rented AI compute (ORCL, AMZN) and energy/infrastructure suppliers (natural gas generators, battery storage, cooling OEMs). Large single facilities (example: Meta ~691 MW, $18bn) imply sustained incremental electricity and metals demand — expect 200–700 MW per hyperscale campus driving multi-year demand for copper, transformers and peaker gas. Winners gain margin leverage; owners that self-fund (Meta) face high near-term capex and cash-flow pressure. Risks & timing: Near-term (days–weeks) headline risks include local permitting moratoria and export-control tweets that can move NVDA/ hyperscaler prints; medium-term (3–12 months) risk is GPU supply-chain shifts (TSMC/ASML constraints) and power-price spikes; long-term (1–3 years) tail risks include regulatory limits on water/power, carbon pricing, or asset stranding from moratoria. Hidden dependencies: grid transmission bottlenecks, offsite turbine builds (cross-state permitting), and secret leasing deals between AI firms and hyperscalers. Trade implications: Tactical: favor NVDA exposure to capture constrained GPU demand; hedge hyperscaler capex risk via short or downside protection on META and selective longs in ORCL/AMZN for hosting revenue. Cross-asset: long power and natural gas forwards for 3–9 months, consider utility/infrastructure equities for 12–36 month carry as local utilities capture new load. Catalysts to watch: NVDA earnings, major AI-hosting contracts, state permit approvals or moratoria within 30–90 days. Contrarian angles: Consensus underprices the probability of overbuild and price compression in colocation/cloud rents — past infrastructure booms (telco towers, 2010s data center cycles) produced multi-year flattening of returns after overcapacity. If GPU inventory metrics or shipment cadence show destocking (manufacturer sell-through down >20% QoQ) treat NVDA exposure as overbought and reduce; conversely, persistent >70% utilization reports across major datacenters justify adding exposure.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25

Ticker Sentiment