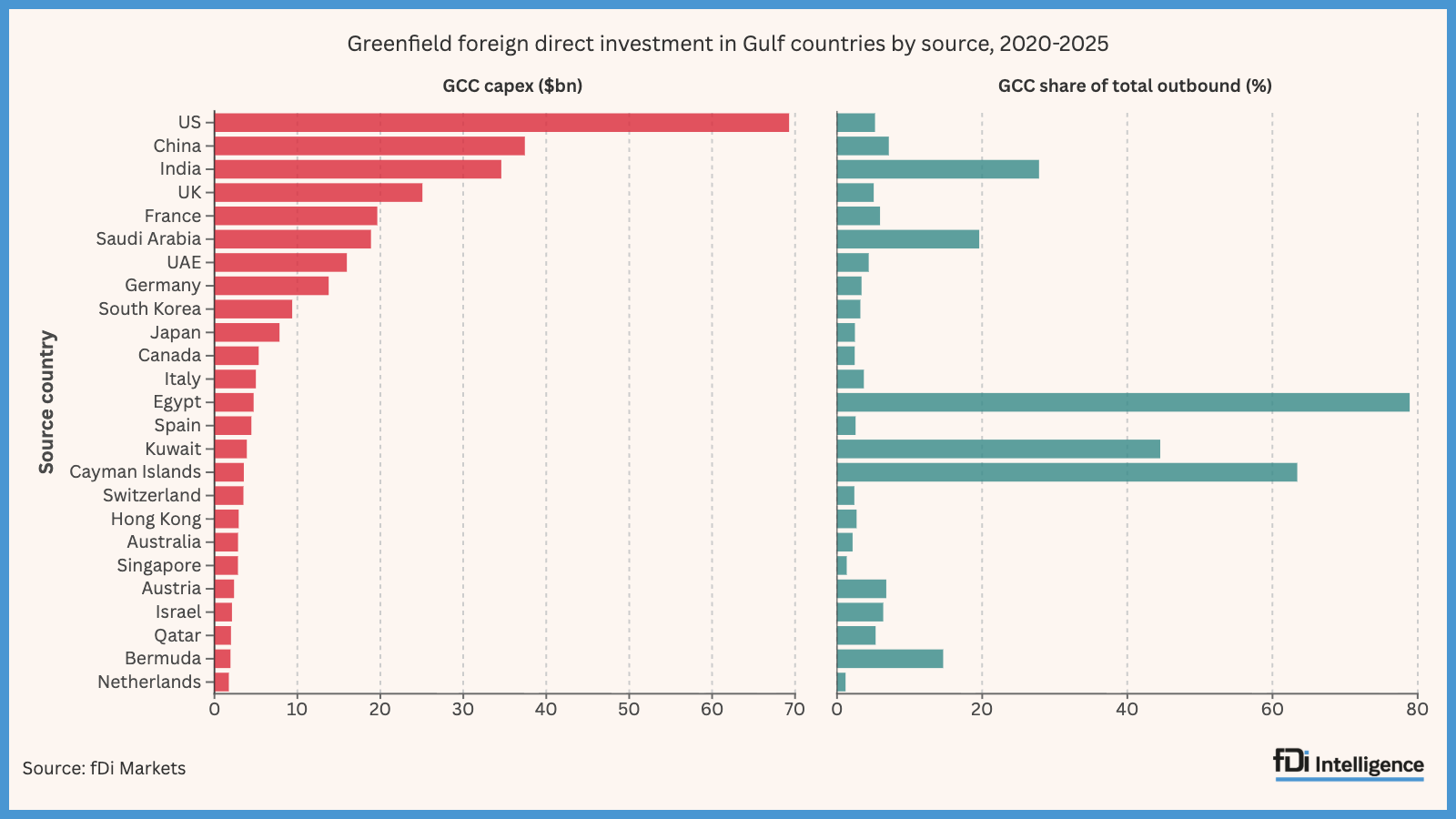

US companies pledged almost $70bn of greenfield FDI to the GCC (2020-2025) within a region that has seen more than $318bn of greenfield announcements over six years; Iran has launched >1,000 missiles and >3,000 drone attacks, damaging energy, data-centre and hotel assets. Brent crude is trading around $100/bbl and the Strait of Hormuz is effectively closed to most traffic, creating meaningful energy and supply-chain disruption. The conflict materially raises geopolitical risk to planned and existing FDI in the Gulf — corporates are recalibrating toward caution rather than wholesale withdrawal, weighing heightened security and operational risks.

Capital allocation into the Gulf is now a two-layer decision: project-level operational risk plus sovereign financing repricing. Expect near-term capex deferral rates to be driven more by insurance and lender margin repricing than by host-country incentives — a 10-30% jump in war-risk and political-risk premia at renewals will materially lift all-in project IRRs and push marginal projects into “delay” territory over the next 6–18 months.

Logistics and energy routing changes are the most immediate economic transmission mechanism. Intermittent diversion of deepwater cargo and hydrocarbons typically adds 7–14 days and $500–$2,000+ per container/tanker voyage; multiplied across volumes this raises production & distribution unit costs and compresses margins for just-in-time manufacturers, creating durable sourcing arbitrage opportunities for nearshore manufacturers in India, Eastern Mediterranean ports and Turkey over 12–36 months.

Insurance/reinsurance and project finance are choke points for FDI continuation. Reinsurers and specialty insurers will capture the bulk of the re-rating via higher premiums and tightened capacity — expect treaty rate momentum to show up in Q3–Q4 renewals. Conversely, sovereign borrowing costs and ECA support for host states will be the gating item for large infrastructure arrivals; a persistent risk premium could shave 2–6% off sovereign GDP-equivalent project returns over 2 years.

Catalysts that reverse the repricing are clear and short-dated: credible ceasefire negotiations or a rapid insurer capital raise (private or public backstop) will compress war-risk premia within 30–90 days. The asymmetric window is that premiums lift fast on episodic strikes but only normalize slowly as underwriting cycles move and lenders re-underwrite facilities.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

strongly negative

Sentiment Score

-0.60