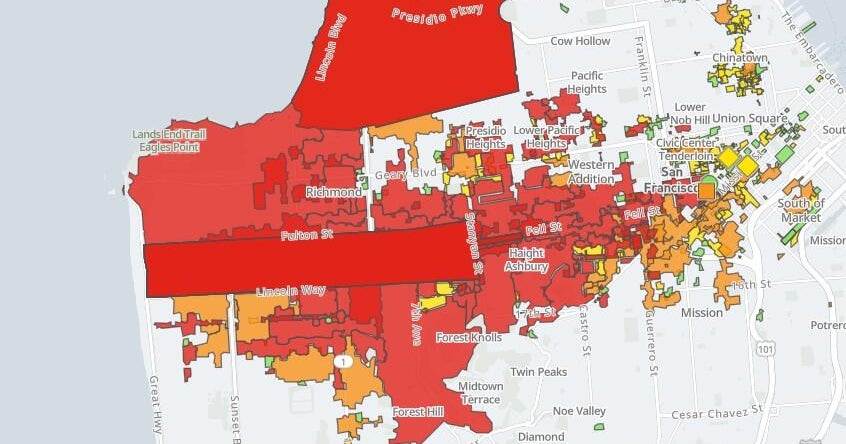

A widespread PG&E power outage left over 100,000 San Francisco customers — roughly 30% of the city — without electricity Saturday afternoon, affecting neighborhoods including the Presidio, Richmond, Sunset, Golden Gate Park and parts of downtown. BART closed Powell Street and Civic Center stations and the city warned that traffic signals may be out; PG&E estimated partial restorations around 3:45 p.m. for some areas and undetermined times for others, and has not identified a cause. The incident poses short-term operational and reputational risk for PG&E and could depress local economic activity and transit usage, but is unlikely to have material market-wide financial effects absent further developments.

Market structure: A San Francisco-wide outage is an idiosyncratic shock that directly hurts PG&E (PCG) operational credibility and downtown-dependent commercial landlords, while benefiting grid-resilience vendors, battery/storage suppliers and emergency services contractors. Expect a ~5-15% near-term uptick in procurement demand for grid hardware and storage RFPs in California over 12–24 months if outages cluster; municipal credit spreads for Bay Area issuers could widen 5–20 bps on rising perceived operational risk. Risk assessment: Tail risks include a multi-day outage, cascading transit shutdowns or a regulatory enforcement cycle that triggers fines/mandated capex (analogous to PG&E’s past wildfire liabilities, potentially $bn-scale). Immediate impact is hours–days (lost economic activity), short-term is weeks–months (litigation/regulatory headlines), long-term is quarters–years (mandated grid modernization and cost recovery fights). Hidden dependencies: downtown CRE valuations, insurance loss models and tech-worker density amplify second-order effects. Trade implications: Tactical: buy protection on PCG (1–3 month puts) and pair with a 6–12 month long in large regulated utilities (NEE, DUK) or grid-equipment names (ABB, SI) to capture relative safety; size small (0.5–2% portfolio each). Strategic: overweight energy storage exposure (TSLA battery business or AES) 1–3% for 12–36 months to capture mandated capex; reduce downtown-focused office/retail REITs (VNQ sub-allocations or direct names with >40% SF exposure) by 2–3%. Contrarian angles: The market may underprice forced utility capex — repeated outages drive predictable multi-year spending that benefits equipment suppliers more than utilities with weak balance sheets. Conversely, avoid overreacting to a single outage: if PCG share moves >10% without new regulatory action, that may be a mean-reversion trade. Historical parallel: isolated outages rarely move durable demand for electricity, but clusters do precipitate regulatory regimes and accelerated spending.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly negative

Sentiment Score

-0.25