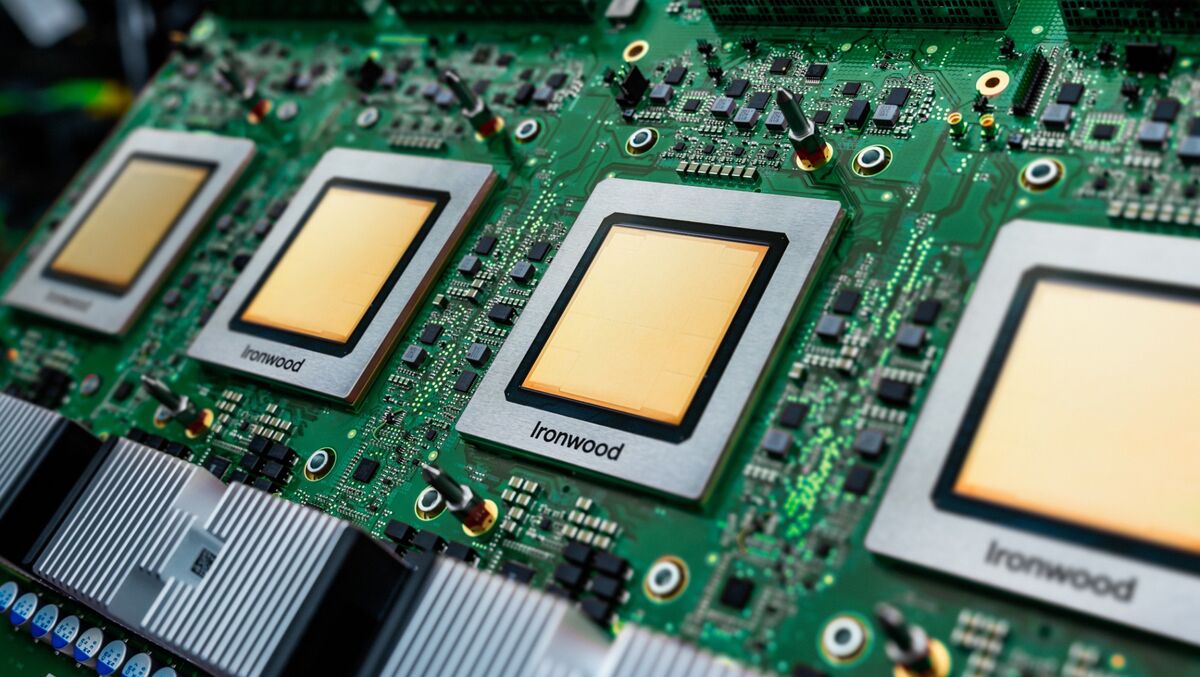

Google's tensor processing units (TPUs), introduced roughly a decade ago to accelerate search and later adapted for machine-learning workloads, have emerged as a credible alternative to Nvidia's dominant AI chips, fulfilling customer demand for more competition. The development highlights rising competitive pressure in the AI accelerator market from hyperscalers repurposing bespoke silicon, a trend that could over time constrain Nvidia's pricing power and spur further innovation among cloud providers and chip vendors.

Market structure: Alphabet (GOOGL) and its Google Cloud business are clear beneficiaries as TPUs lower unit compute costs and increase margin optionality; large cloud buyers (AMZN, MSFT) also benefit if they adopt similar accelerators. Nvidia (NVDA) and to a lesser extent AMD (AMD) face lower incremental pricing power for datacenter GPUs — expect potential displacement of 5–15% of GPU demand in 12–36 months and ASP pressure of ~5–20% on certain inference GPU SKUs if TPUs gain enterprise traction. Risk assessment: Tail risks include rapid open-sourcing of TPU tooling that accelerates adoption, or conversely Nvidia deepening software lock-in (CUDA) that limits TPU uptake; US/China export controls or foundry (TSMC) capacity shocks could swing outcomes. Immediate (days) moves will be headline-driven; short-term (weeks–months) depends on benchmarks and Google Cloud pricing; long-term (quarters–years) depends on ecosystem portability and total cost of ownership vs GPUs. Trade implications: Favor conviction-sized longs in cloud/IP owners and selective hedges on pure-play GPU exposure. Use 3–9 month options to express views (cheaply hedge tail risk) and rotate weights from hardware suppliers into cloud/software providers; monitor margins and ASPs as leading indicators. Contrarian angle: Markets may underweight the software/ecosystem friction — TPUs excel on specific models but migratory costs (tooling, retraining, ops) favor incumbents. Shorting NVDA outright is risky; prefer paired/optioned trades that cap downside if Nvidia defends share via price cuts or new software offerings.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.15