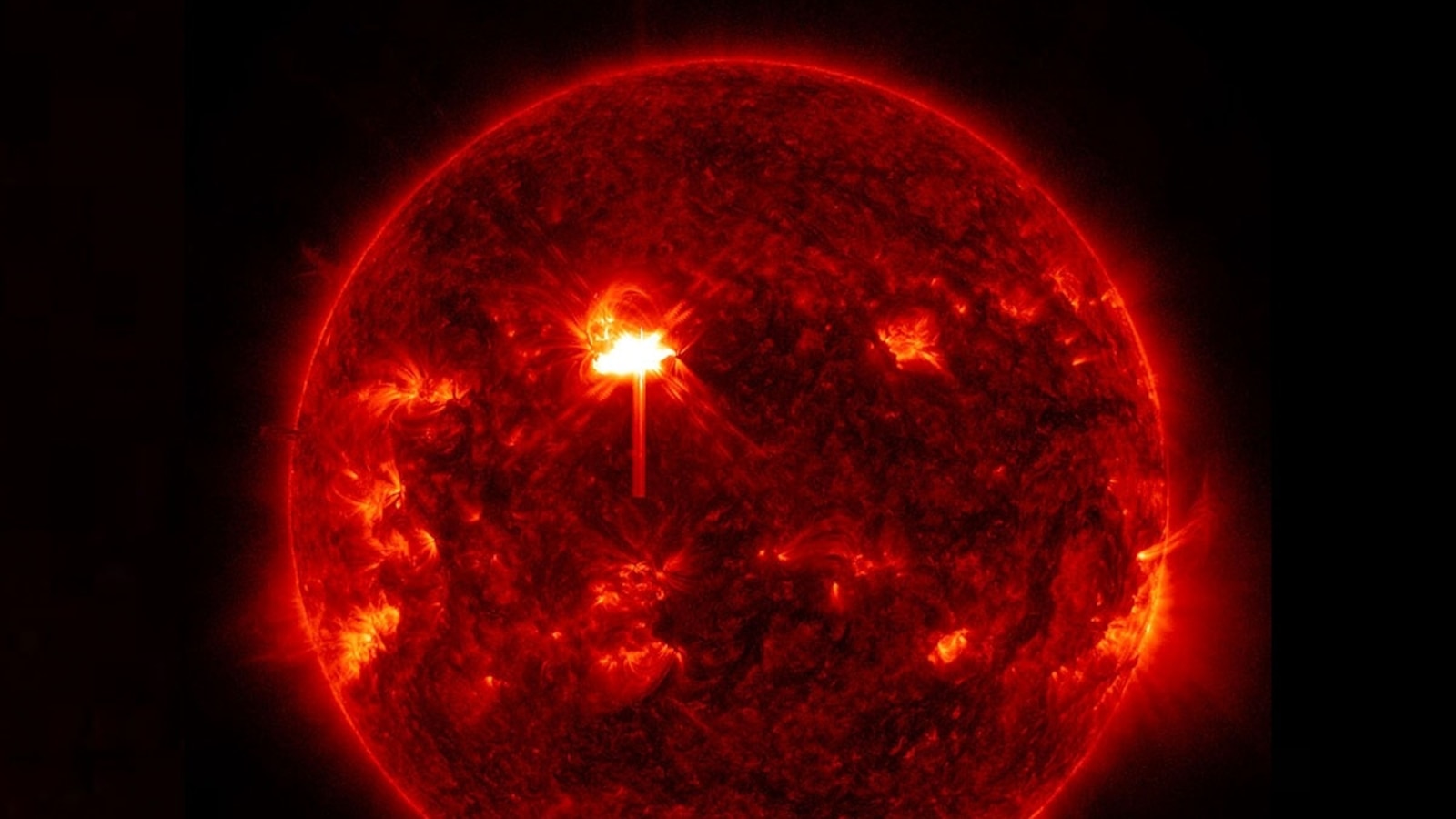

The sun emitted four X-class solar flares over the weekend and Monday (three on Sunday at 7:33 a.m., 6:37 p.m. and 7:36 p.m. ET, and one on Monday at 3:14 a.m. ET), including a massive X8.1 event — the strongest in several years, according to NASA. These high-energy outbursts can produce immediate high-frequency communications loss for minutes to hours, may precede coronal mass ejections that threaten satellites and infrastructure, and NOAA warns elevated solar and geomagnetic activity is likely to continue through 2026 following the October 2024 solar maximum.

Market structure: Frequent X‑class flares and elevated geomagnetic activity through 2026 (NOAA) shift economic winners toward space‑hardening vendors, defense primes and power‑grid equipment manufacturers. Direct beneficiaries: LMT, NOC, LHX, MAXR, ABB, GE — firms selling hardened satellites, radiation‑tolerant electronics, transformers and grid relays; losers include small-cap satellite service firms with single‑satellite reliance and insurers with underpriced space/geomagnetic exposure. Pricing power will favor suppliers of critical hardware as governments and utilities accelerate capex; replacement cycles could add a multi‑billion‑dollar procurement tailwind over 12–36 months. Risk assessment: Tail risks include a Carrington‑scale CME (low probability <1% annually) that could create multi‑week satellite outages and transformer damage, forcing emergency fiscal spending and insurance losses; operational risks to supply chains (semiconductor availability) could amplify costs by +10–25%. Immediate window: days–weeks for HF comms interruptions and localized outages; short term (months) for insurance and airline routing impacts; long term (quarters–years) for grid and space resilience capex. Hidden dependencies include reliance on a handful of transformer manufacturers and on Asia‑based electronics fabs. Trade implications: Favor 6–18 month overweight in defense/civil space hardware (LMT, NOC, LHX) and industrials (ABB, GE) with size discipline (1–3% positions), and buy 3–12 month OTM puts on utilities/insurers as tail hedges (e.g., XLU puts, or NEE/PCG single‑name hedges). Use pair trades: long MAXR (satellite rebuild demand) vs short small-cap satellite service names that lack diversification. Options: buy 3–6 month protection (straddles or deep OTM calls on LMT/LHX) around budget windows and expected CME arrivals. Contrarian angles: Markets underprice a sustained capex cycle — consensus treats events as noise; if geomagnetic activity persists, procurement cycles (transformers, rad‑hardened chips) could drive 10–20% EBITDA upgrades for niche suppliers over 12–24 months. The overdone panic trade would be outright shorting satellite equities; instead, prefer long suppliers and selective hedges because replacement demand and defense budgets create persistent tailwinds, while the immediate headline risk remains sporadic and often insured.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.00