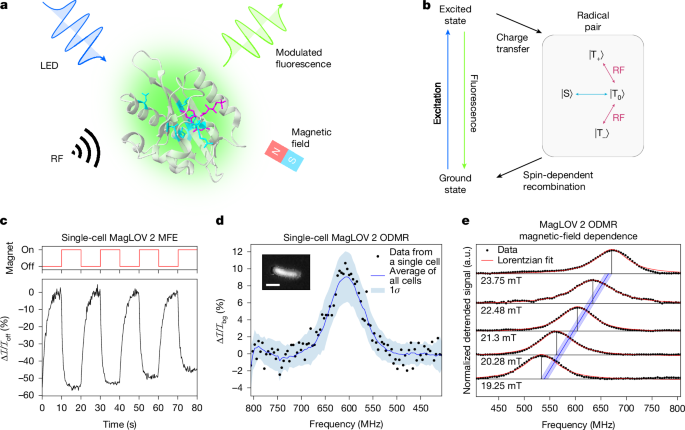

Researchers report engineered magneto-sensitive fluorescent proteins (MagLOV variants) that exhibit measurable optically detected magnetic resonance (ODMR) and large magnetic-field effects (MFE), including a −50% MFE for MagLOV 2 and single-cell ODMR contrast of ~10% with per-cell magnetic sensitivity η0 ≈ 26 μT Hz−1/2. Through directed evolution they produced variants (MagLOV 2 and MagLOV 2 fast) optimized for magnitude and saturation rate, demonstrated applications in lock‑in amplification, multiplexed cellular tagging, MRI-style spatial localization and microenvironment sensing (Gd3+ causes dose-dependent MFE attenuation). The findings present an actionable pathway for commercializable quantum‑biosensing tools and a startup tie (a cofounder disclosed), but near-term market impact is limited while engineering, validation and regulatory steps remain.

Market structure: Engineered magneto‑sensitive proteins (MagLOV) create a new demand vector for synthetic biology services, preclinical imaging hardware and niche MRI/optical instrument vendors. Immediate winners are DNA synthesis/engineering enablers (e.g., TWST) and specialist instrument makers (preclinical MRI/quantum-sensing: BRKR), while incumbent contrast‑agent franchises (gadolinum-dependent revenue) face modest long-term substitution risk. Expect a multi‑year shift: addressable market initially in research tools ($100sM–low $B) with potential clinical TAM only if in‑vivo safety/translation succeeds (3–7+ years). Risk assessment: Key tail risks are regulatory/bioethics action or reproducibility failure (low probability, high impact) and IP/competing patents; operational scale‑up to mammalian systems is uncertain. Time horizons: negligible public‑market price impact in days; short term (3–12 months) revolves around replication, VC deals and IP filings; long term (12–48 months) is commercialization and device integration. Watch milestones: independent replication in mammalian tissue, major patent grants, and any FDA guidance on magnetogenetics. Trade implications: Favor selective exposure to enablers of directed evolution and preclinical imaging while avoiding pure contrast‑agent plays. Use concentrated, staged allocations with option hedges because adoption is binary and lumpy; expect upside if research‑tool annual revenue growth accelerates by 15–25% within 12–24 months. Cross‑asset: small positive for specialized equipment capex (buy skew), negligible macro FX/commodities impact; credit spreads for large diversified healthcare names unlikely to move materially. Contrarian angle: Consensus will overrate near‑term clinical impact and underprice long lead times; commercialization is paced by biology not novelty. Therefore prefer VC/strategic incubation and equipment plays over clinical biotechs claiming immediate therapy impact. Potential unintended consequence: fragmented IP and safety scares could temporarily depress small‑cap biotech valuations — create buying opportunities after validated in‑vivo demonstrations (12–24 month signal).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment