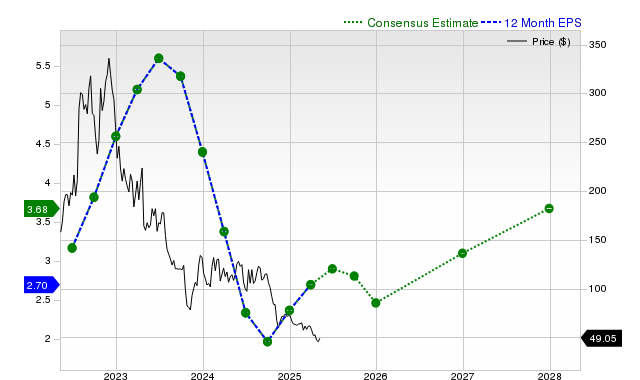

Enphase Energy posted a quarter with revenue of $410.43M (+7.8% YoY) and EPS $0.90 versus $0.65 a year ago, beating Zacks consensus revenue by 13.44% and EPS by 45.16%. Forward consensus shows a weaker near-term profile: current-quarter EPS $0.56 (-40.4% YoY) and revenue estimate $331.97M (-13.3% YoY), with fiscal-year EPS $2.79 (+17.7%) but next fiscal-year EPS $2.18 (-21.9%) and revenue sliding to $1.25B. Zacks assigns a Rank #3 (Hold) and a Value Style Score of C, implying the stock may perform in line with the market despite the recent quarter beat.

Market structure: ENPH’s recent beat but flat estimate revisions signal demand bifurcation — installers and residential retrofit winners (stable ASPs, storage-coupled sales) while pure panel suppliers and margin-sensitive peers lose if volumes slide. Competitive pressure from SolarEdge (SEDG) and low-cost Chinese string inverter makers keeps pricing power capped; expect share shifts toward vendors with bundled storage/monitoring (6–24 months). On supply/demand, consensus revenue cuts (-13.3% current-quarter estimate) imply inventory digestion or seasonality; a repeat miss would flip market from scarcity to oversupply in components (semis, MOSFETs) within 3–6 months. Cross-asset: a sector drawdown would raise equity vols (ENPH options vol spike >+30% realized), modestly widen high-yield spreads for green project finance and lift defensive utility names (NEE), while exerting downward pressure on copper/polysilicon over quarters if module demand drops materially. Risk assessment: Tail risks include a warranty/recall hit or new tariff/subsidy reversals that could cut FY+1 EPS >20% (high-impact, <10% prob); supply-chain chip shocks could compress margins 200–400bps short-term. Immediate (days) risk is IV-driven post-earnings swings; short-term (weeks/months) depends on installer order flow and incentive news; long-term (1–3 years) hinges on storage adoption and IRA-style subsidies. Hidden dependencies: channel concentration with top installers, battery partner deals, and timing of state incentives; second-order effects include installer insolvency cascading to receivables and revenue recognition. Key catalysts: next quarterly release and guidance (within 30–60 days), state-level incentive announcements, and SEDG product launches. Trade implications: Direct play — tactical small long in ENPH (2–3% portfolio) only on a disciplined pullback (>8% from today) with 15% stop and 30–40% 12-month target, else favor option structures. Pair trade — go long SEDG and short ENPH equal-dollar (1–2% each) to capture dispersion if installers favor optimizers over microinverters; close on 15% relative move or 6-month horizon. Options — buy 3-month put spread on ENPH (10%/20% OTM) to hedge core exposure or sell covered calls if holding through calm IV <40%; size to cap downside to 10–12% portfolio risk. Sector rotation — shift 2–4% from pure solar gadget names into regulated generators (NEE) and grid software/semis (ON) for lower beta exposure over 3–12 months. Contrarian angles: Consensus underweights the embedded value of Enphase’s software/storage roadmap; if Enphase converts 20–30% of installs to battery-coupled sales, lifetime revenue per customer could rise 10–25% (1–3 year payoff), a catalyst analysts may underappreciate. Conversely, the market may be underpricing short-term execution risk — unchanged estimates after a beat suggest analyst complacency and an opportunity to profit from downward revisions. Historical parallels: post-2018 solar inventory corrections rebounded within 6–12 months as installers restocked; if that pattern repeats, a disciplined long after a 15–25% drawdown could outperform. Unintended consequence: aggressive installer discounts to win volume would compress gross margins and accelerate consolidation, hurting smaller vendors and altering channel economics.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.05

Ticker Sentiment