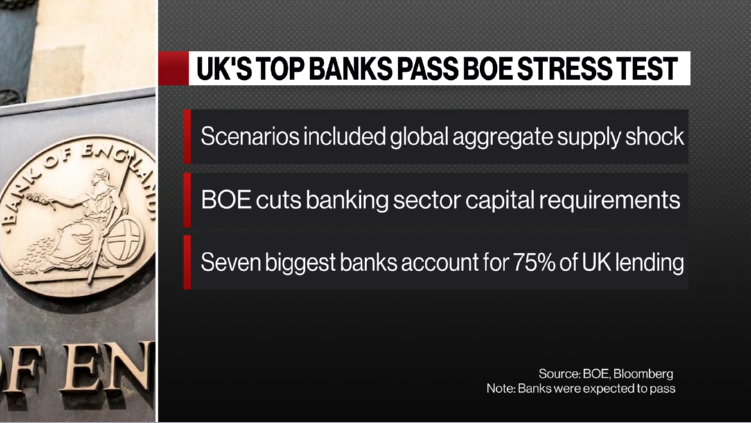

The Bank of England has signalled a lowering of its systemic UK banks' capital benchmark from 14% to 13%, a change it says will not take effect until 2027; banks currently hold around 17% CET1, suggesting reluctance to immediately release capital for lending or payouts. The regulator will launch targeted reviews and a new private markets stress test amid flagged risks—valuation concerns, private markets and potential housing bubbles—leaving near-term policy direction and actual capital relief for banks uncertain.

Market structure: Lowering the systemic CET1 target from 14% to ~13% (flowing in by 2027) is a structural tailwind to UK bank capital returns — banks already hold ~17% CET1 so incremental distribution could be 200–400bps of excess capital if boards are willing to return it via buybacks/dividends over 12–36 months. Retail and commercial banks with large deposit bases (LLOY.L, NWG.L, BARC.L) are the primary beneficiaries; wholesale/international banks (STAN.L, parts of HSBA.L) are less levered to UK regulatory easing and could see smaller near-term share gains. Risk assessment: Key tail risks include a private-markets shock (BoE launching a private market stress test this week), a UK housing repricing, or political clampdown on payouts — any one could force higher loss-absorbing buffers and reverse equity upside. Immediate (days–weeks): elevated headline volatility around the BoE press conference and private-market stress test; short-term (months): management capital-return guidance and regulatory consultation outcomes; long-term (2026–2028): realization of credit losses if credit growth accelerates into mispriced real estate. Trade implications: Favor overweight equity exposure to UK retail banks via direct longs (LLOY.L, NWG.L) size 2–3% portfolio, financed by underweight European universal banks (e.g., BNP.PA) to capture a ~200–400bp differential in capital redeployment potential over 12 months. Use options to skew risk: buy 6–9 month call spreads on BARC.L and LLOY.L (10–30% OTM buy/sell) sized 0.5–1% each to limit premium but capture upside into H1–H2 2026 when capital returns are likely signaled. Contrarian angle: Consensus assumes capital release converts straight to payouts; historical behavior shows banks hoard buffers — expect only a partial flow (25–50% of theoretical excess) in first 24 months, so markets may be overpricing near-term dividend upside. Catalysts that could reverse trades: stricter BoE consultations, adverse private-market stress-test results, or a UK recession that widens bank credit spreads by 100–200bps. Position accordingly with tight stop-losses and tranche entries keyed to regulatory milestones (BoE review outcomes early next year, private-market stress-test results this week).

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mixed

Sentiment Score

0.10