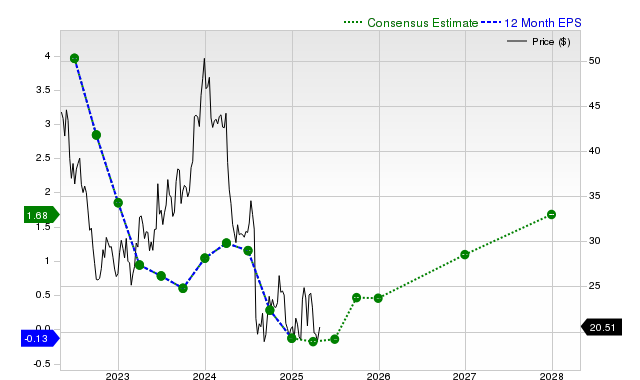

Intel (INTC) shares have significantly outperformed, gaining +16.1% over the past month, exceeding the S&P 500 and its industry. While the company recently reported revenue and EPS beats, analyst consensus estimates for both current and next fiscal year earnings have seen recent downward revisions, though next fiscal year revenue is projected to grow. Consequently, Zacks rates Intel a 'Hold' (Rank #3), indicating expected in-line market performance, and assigns a 'C' valuation grade, suggesting it trades at par with peers.

Intel Corporation (INTC) has demonstrated significant recent stock momentum, with a +16.1% return over the past month that outpaced the S&P 500 and matched its industry peers. This performance is backstopped by a recent earnings report where the company's revenue of $12.67 billion and EPS of $0.13 surpassed consensus estimates by +2.8% and +1200%, respectively. However, a more cautious forward-looking view is emerging, as sell-side analysts have revised earnings estimates downward for the current quarter (-1.4%), current fiscal year (-3.8%), and next fiscal year (-4.3%) within the last 30 days. This contrasts with expectations for a significant YoY EPS rebound of +315.4% this year and +162.3% next year. The revenue outlook is similarly mixed, with a projected decline of -7.5% in the current quarter and -4.3% for the current fiscal year, before an anticipated recovery to +4.1% growth next year. This combination of recent outperformance against a backdrop of weakening analyst sentiment and near-term revenue headwinds underpins the stock's Zacks Rank #3 (Hold) and a 'C' valuation grade, suggesting it is trading at par with peers and may perform in line with the broader market.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

Neutral

Sentiment Score

0.15

Ticker Sentiment