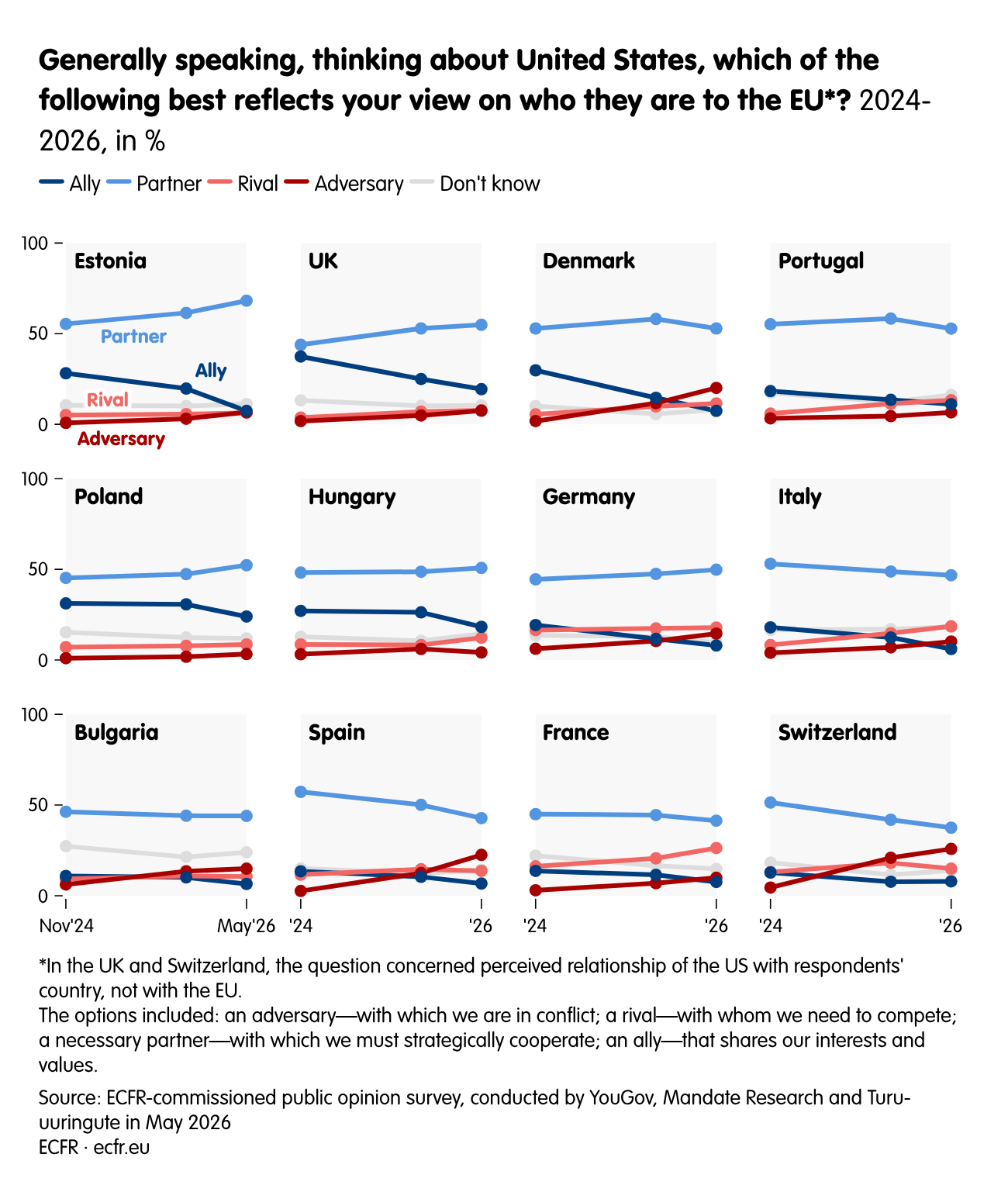

An ECFR poll of 19,481 respondents across 15 European countries shows only 11% now view the US as an ally, down from 16% six months ago and 22% in November 2024, while most Europeans support higher defense spending and greater self-reliance. Public backing remains strong for Ukraine, but voters are wary of EU accession now and largely oppose sending troops, and they also reject renewed Russian fossil-fuel imports despite higher energy prices. The findings support a push toward European strategic autonomy, defense common debt, and renewable energy, with meaningful implications for policy and elections across Europe.

The market-relevant takeaway is not simply “Europe spends more on defense,” but that the political constraint set is shifting toward financing autonomy via common debt and domestic procurement. That is a direct relative tailwind for European primes, ammunition, electronics, cyber, and infrastructure-enablement names versus US suppliers, because the next euro of incremental spend is more likely to be ring-fenced for sovereign capability rather than imported hardware. The second-order winner is likely the entire European industrial base tied to defense localization, since procurement rules and industrial-policy optics will favor local content over pure cost efficiency. The bigger medium-term implication is that the public is giving policymakers cover to do two unpopular things simultaneously: front-load defense capex and accelerate energy re-shoring. That combination is structurally bullish for European utilities with renewables pipelines, grid equipment, LNG import infrastructure, and transmission buildout, but it is negative for any residual Russian-linked energy exposure and for firms dependent on cheap imported fossil inputs. The key nuance is that this is a demand-pull for sovereignty, not a blanket risk-on vote; it supports capex cycles, not consumer demand. The main fragility is timing. The poll says voters accept the direction, but their tolerance is conditional on near-term macro relief; if the energy shock worsens, the same electorate may punish incumbents before strategic spending matures. That creates a 3-9 month window where the trade is more about policy signaling and budget commitments than realized earnings, and the real catalyst will be autumn/winter energy prices plus election rhetoric. A reversal likely requires either a Trump moderation narrative or a rapid de-escalation in energy markets; absent that, the consensus underestimates how much policy can move from rhetoric to procurement once fiscal rules are politically loosened.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

neutral

Sentiment Score

0.10

Ticker Sentiment