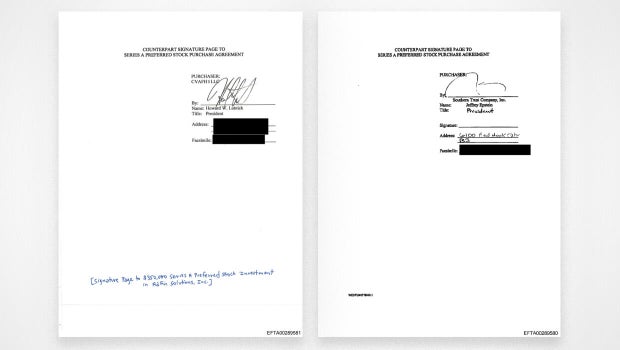

Documents from the Epstein files show U.S. Commerce Secretary Howard Lutnick and Jeffrey Epstein signed a Dec. 28, 2012 agreement to acquire stakes in ad-tech firm Adfin (nine shareholders listed), with Epstein signing for Southern Trust Company, Inc. and Lutnick for CVAFH I. Correspondence and emails indicate interactions from 2011–2014, Cantor Fitzgerald was a reported small minority investor via Cantor Ventures, and Lutnick denies wrongdoing and says interactions were limited; the revelations pose reputational and political risk but are unlikely to produce direct, material market impacts.

Market structure: The revelations are a reputational shock that primarily hurts opaque private-market/late-stage ad‑tech financings and small independent ad-tech vendors; expect discretionary re‑pricing of niche ad-tech startups by 5–15% over 3–12 months as LPs demand stronger governance. Winners are compliance/legal advisers and large “walled garden” platforms (AAPL, GOOGL) that can capture displaced ad dollars and provide stronger brand safety; expect modest upside of 5–12% for incumbents if market share shifts within 6–12 months. Risk assessment: Tail risk is a low‑probability (10–15%) but high‑impact cascade—Congressional hearings or regulatory probes could trigger short‑term policy friction that delays trade or appointments and squeezes investor confidence in private deals; material market moves would occur within days-to-weeks of new revelations, with lingering liquidity tightening for targeted sectors for quarters. Hidden dependency: many LP/GP relationships rely on personal networks; second‑order effect is reduced deal flow and higher due‑diligence costs (increase OPEX 10–30% for VC funds that tighten controls). Trade implications: Near term, volatility should spike around document releases/hearings—buy a small VIX call spread (30/40, 1‑month) sized 0.5% portfolio as tail hedge. Reallocate away from small ad‑tech names (trim TTD and small caps by 20–50% over 30 days) into AAPL and GOOGL (each add 0.5–1% positions, 6–12 month horizon). Keep a tactical short XLF (1–2% notional) only if political fallout forces a >2% drop in financials within 30–90 days. Contrarian angles: The market may underreact to governance tightening that will compress private‑market entry valuations by 10–25% over 12–24 months—this creates buyable distress in surviving ad‑tech assets; consider staging purchases at 6–12 month marks post‑funding slowdowns. Conversely, an overbroad political backlash could lead to regulatory overreach hurting legitimate deal‑making—avoid levered exposure to small managers and prefer cash‑rich incumbents and forensic/legal services during the next 90–180 days.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately negative

Sentiment Score

-0.35