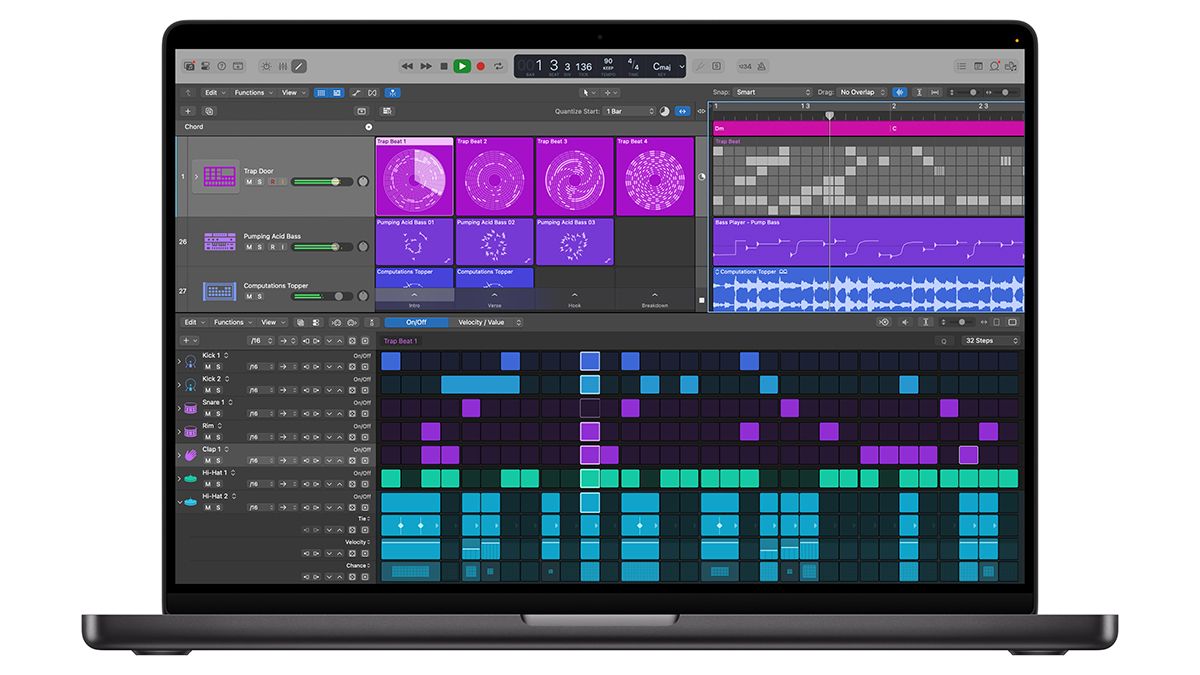

Apple is rolling out a Creator Studio subscription bundle (priced at $/£12.99 per month or $/£129 per year, with a reduced student monthly rate of $/£2.99) that groups Final Cut Pro, Logic Pro (Mac v12, iPad v3), Pixelmator Pro and other apps and introduces AI-driven features such as a Synth Player and Chord ID; the new Logic Pro versions ship on 28 January. The company frames these tools as assistive rather than replacing artists, and notes that after the bundle launch Logic Pro for iPad will only be available via the subscription for new users, a move that could modestly influence uptake of Apple’s creative software subscriptions.

Market structure: Apple’s Creator Studio bundling (launch 28-Jan) deepens Services stickiness and creates a low‑price point ($12.99/mo or $129/yr) that can drive measurable ARPU gains if adoption reaches even 0.5–2% of Apple’s active Mac/iPad user base over 12–24 months—this implies incremental revenue on the order of hundreds of millions to low‑single‑digit billions annually and improves ecosystem pricing power vs. niche DAW vendors (Avid). Third‑party plugin vendors and small DAW makers face downside from platform consolidation; large incumbents with cross‑platform reach benefit via distribution and potential hardware control (MIDI integrations). Risk assessment: Tail risks include regulatory action on AI content/copyright or artist pushback that could slow uptake—probability medium but impact high (could erase >50% of projected incremental revenue in 12 months). Operational risks: cannibalization of standalone iPad Logic subscribers (price arbitrage) and content moderation liabilities. Key catalysts: 28‑Jan release, WWDC and the next Apple earnings (within 3–6 months) when Services guidance could be updated. Trade implications: Direct equity exposure: AAPL benefits asymmetrically; consider modest overweight into a near‑term window around 28‑Jan and into the next 3–6 months as subscriber data and guidance emerge. Use options to size convexity: 3–6 month call spreads ~8–12% OTM to limit capital while capturing upside; hedge tail AI‑regulatory risk with cheap long‑dated puts ~9–12 months if conviction weakens. For relative value, AAPL vs AVID (long AAPL, short AVID) captures share shift in pro audio. Contrarian angles: Consensus underprices the stickiness value—if Creator Studio converts 1–2% of users it’s material to Services; conversely the market may underprice regulatory backlash (copyright litigation or platform bans like Bandcamp’s stance). Historical parallel: Apple’s bundling (Apple One) produced multi‑year Services lift despite initial cannibalization; but if artist coalitions or regulators force restrictions, the upside is capped. Act with asymmetric sizing and explicit hedges.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

mildly positive

Sentiment Score

0.25

Ticker Sentiment