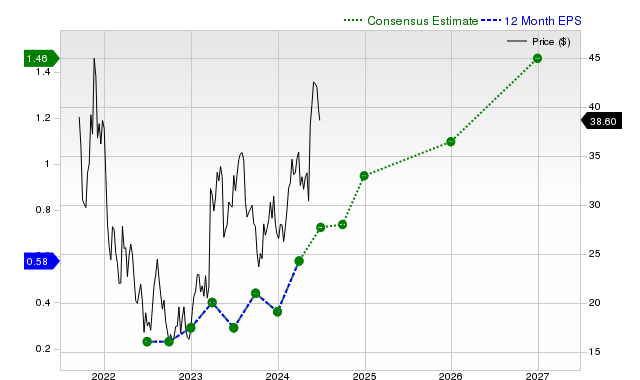

On Holding (ONON) has recently garnered market attention, with its shares returning +2.7% over the past month, trailing the S&P 500 and its industry. Despite this underperformance and an 'F' valuation grade indicating a premium to peers, Zacks assigns ONON a Rank #2 (Buy). This positive rating is driven by strong consensus revenue growth projections, such as +33.6% for the current quarter, and favorable near-term earnings estimate revisions, although next fiscal year's EPS estimates have seen a slight negative revision.

On Holding AG (ONON) presents a classic growth versus valuation dilemma for investors. The company's top-line momentum is significant, with last quarter's revenue growing 39% year-over-year and consensus estimates projecting continued strength of +33.6% for the current quarter and +32% for the current fiscal year. This robust growth narrative is bolstered by positive near-term earnings estimate revisions, with the current quarter's EPS expected to rise 50% YoY, contributing to a Zacks Rank #2 (Buy). However, this optimism is tempered by several key concerns. The company's profitability has been inconsistent, evidenced by an EPS miss of -4.17% in the last reported quarter and a track record of surpassing EPS estimates only once in the last four periods. Furthermore, while near-term estimates have risen, the consensus EPS estimate for the next fiscal year has been revised downward by 1.9% over the past month, signaling potential future headwinds. This is compounded by a significant valuation risk, as highlighted by a Zacks Value Style Score of 'F', indicating the stock is trading at a premium to its peers. The stock's recent underperformance, gaining only 2.7% against its industry's 7.1%, suggests the market may be weighing these risks against the strong growth story.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

moderately positive

Sentiment Score

0.40

Ticker Sentiment