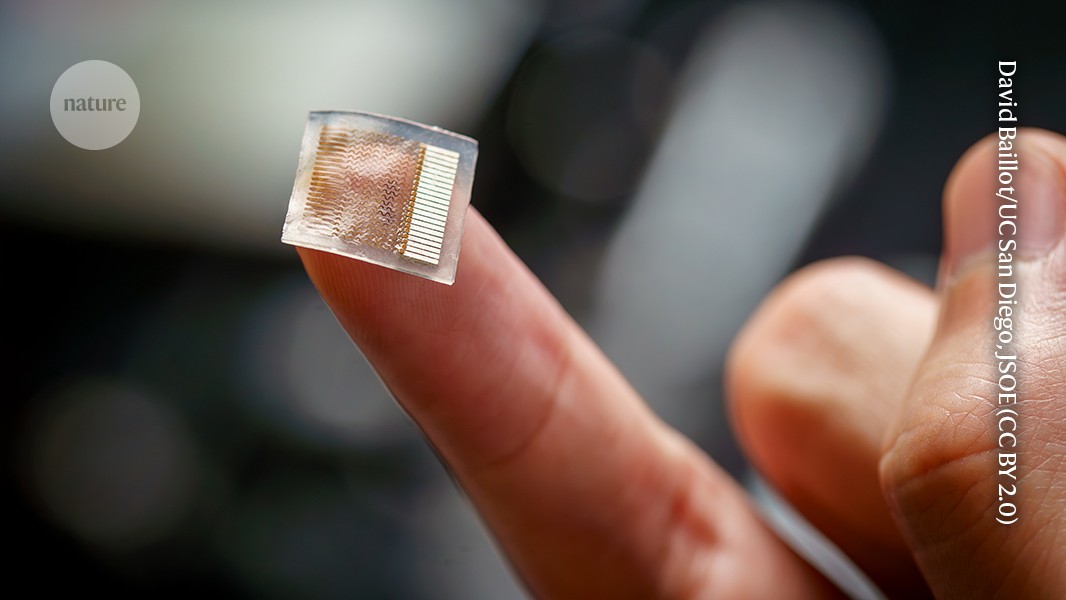

A Nature commentary proposes strategies to reduce the environmental impact of wearable health‑care devices, focusing on lifecycle analysis, material selection, repairability, and end‑of‑life recycling to address rising e‑waste. Citing sources including the Global E‑Waste Monitor 2024 and World Bank guidance, the piece highlights regulatory and supply‑chain risks and potential commercial opportunities for device manufacturers, recyclers and investors in circular‑economy solutions as sustainability requirements intensify.

Market structure: Regulatory and corporate ESG pressure favors large, trusted device makers (Apple AAPL, Abbott ABT, Dexcom DXCM) and scalable recyclers/servicers (Waste Management WM, Li-Cycle LICY). Small, low-margin consumer wearable brands and single-use health sensors face margin compression and higher TCO; expect 5–15% price premium for devices marketed as repairable/recyclable over 12–24 months. Recycled-metal demand for wearables could rise ~15–30% in 3 years, tightening supply of secondary feedstocks and improving pricing power for recyclers. Risk assessment: Tail risks include rapid regulatory mandates (EU ecodesign / US FTC rules) within 6–18 months that raise compliance costs >$5–15 per unit, forcing consolidation or bankruptcy among smaller OEMs. Short-term (days–weeks) volatility around regulatory announcements; medium (3–12 months) execution and supply-chain shifts; long-term (2–5 years) structural reweighting toward circular supply chains. Hidden dependencies: heavy reliance on Chinese contract manufacturers and on a small set of metal recyclers; disruption there amplifies shortages. Trade implications: Overweight regulated med-device and recycler exposures: AAPL (2–3% long), ABT/DXCM (1–2% each) and WM/LICY (1–2% each, smaller size for LICY). Use 9–18 month call spreads on ABT or AAPL to capture adoption of premium sustainable features; buy long-dated calls on LICY as a convex, event-driven stake tied to scaling milestones. Pair idea: long ABT or DXCM vs short small-cap consumer wearables ETF/peers to capture margin dispersion over 6–24 months. Contrarian angles: Market underprices recycling execution optionality and M&A value (Apple/Alphabet could vertically integrate recycling/repair), creating asymmetric upside for mid-cap recyclers if one proves scalable. Conversely, the consensus may overestimate near-term cost pass-through — if manufacturers absorb costs, demand may shift less, compressing recyclers’ near-term margins. Historical parallel: smartphone circularity rules created multi-year winners among recyclers and service providers; expect similar split outcomes here.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

neutral

Sentiment Score

0.00