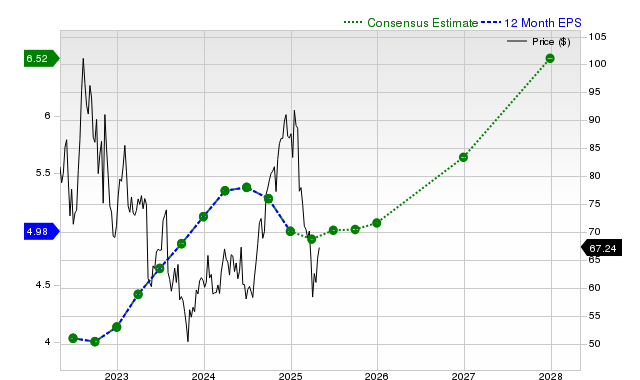

PayPal (PYPL) currently holds a Zacks Rank #2 (Buy) and a Value Style Score of 'A', indicating potential near-term outperformance and a discounted valuation relative to peers, despite its shares returning only +0.7% over the past month against the S&P 500's +4.8%. Analysts project robust earnings growth, with current fiscal year EPS estimated at $5.23 (+12.5% YoY), alongside revenue growth, with current fiscal year sales at $33.06 billion (+4% YoY). The digital payments firm has also consistently surpassed EPS estimates in the last four quarters, reinforcing the positive outlook derived from earnings estimate revisions.

Despite significant underperformance over the past month, where shares returned +0.7% against the S&P 500 composite's +4.8% gain, fundamental indicators for PayPal (PYPL) appear favorable. The stock holds a Zacks Rank #2 (Buy), primarily driven by positive earnings estimate revisions. Analysts project robust double-digit earnings growth, with the consensus estimate for the current fiscal year at $5.23 per share, a 12.5% year-over-year increase, and $5.79 for the next fiscal year, a 10.6% increase. This earnings optimism is supported by a strong history of beating consensus EPS estimates in each of the last four quarters, including a +7.69% surprise in the most recent report. However, projected revenue growth is more modest, with estimates pointing to a +4% change for the current year and +6% for the next. The company's valuation is a key highlight, earning a Zacks Value Style Score of 'A', which suggests the stock is trading at a discount relative to its peers. This combination of strong earnings momentum, a history of positive surprises, and an attractive valuation contrasts sharply with its recent market lag.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request a DemoOverall Sentiment

strongly positive

Sentiment Score

0.80

Ticker Sentiment