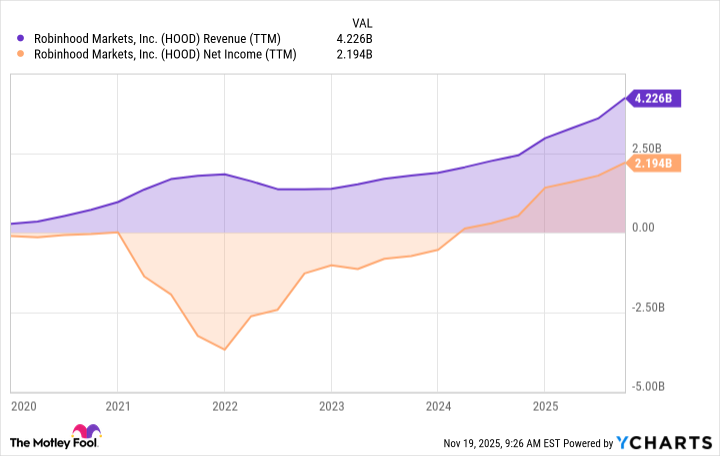

Robinhood has staged a marked turnaround, expanding total platform assets from $102 billion at the start of 2024 to $343 billion by October and reporting quarterly revenue of $1.27 billion and EPS of $0.61 (slightly ahead of consensus) as transaction revenue jumped 129% to $730 million (crypto +300%, options +50%, equities +132%), ARPU rose 82% to $191 and net interest income grew 66% to $456 million. Management is diversifying monetization beyond PFOF via its Gold subscription, scaling prediction markets (now over $100 million annualized and, per Bernstein, tracking toward a $300 million run-rate) and filing a Robinhood Ventures Fund I to give retail access to private companies and potentially private AI investments while seeking international approvals. The stock trades at roughly 47x this year’s projected EPS, reflecting lofty growth expectations; the company’s multi-product expansion presents meaningful upside but also execution and regulatory risk, suggesting the name is better as a growth sleeve within a diversified portfolio rather than a sole long-term bet.

Robinhood has executed a pronounced operational turnaround: total platform assets surged from $102 billion at the start of 2024 to $343 billion by the end of October, and recent quarterly results beat consensus with $1.27 billion in revenue and $0.61 EPS. The stock’s dramatic past appreciation (about $8 two years ago to $115 today) underscores investor enthusiasm but is historical and not a guide to future returns. The current revenue mix shows meaningful diversification and monetization leverage: transaction revenue jumped 129% to $730 million (crypto +300%, options +50%, equities +132%), ARPU increased 82% to $191, and net interest income rose 66% to $456 million; Gold subscriptions supply recurring revenue. Management is also scaling new revenue channels—prediction markets exceeded $100 million annualized and Bernstein notes a path toward a $300 million run-rate—while filing Robinhood Ventures Fund I to open private-market access to retail and pursuing international approvals. Valuation and risk profile are clear: the shares trade at about 47x this year’s projected EPS and the note calculates a ~26% CAGR is needed to convert $10,000 into $1 million over 20 years, implying high growth expectations priced in. The company’s upside depends on execution of new products and regulatory outcomes, making the name suitable for a growth sleeve rather than a concentrated core holding.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Overall Sentiment

moderately positive

Sentiment Score

0.45

Ticker Sentiment