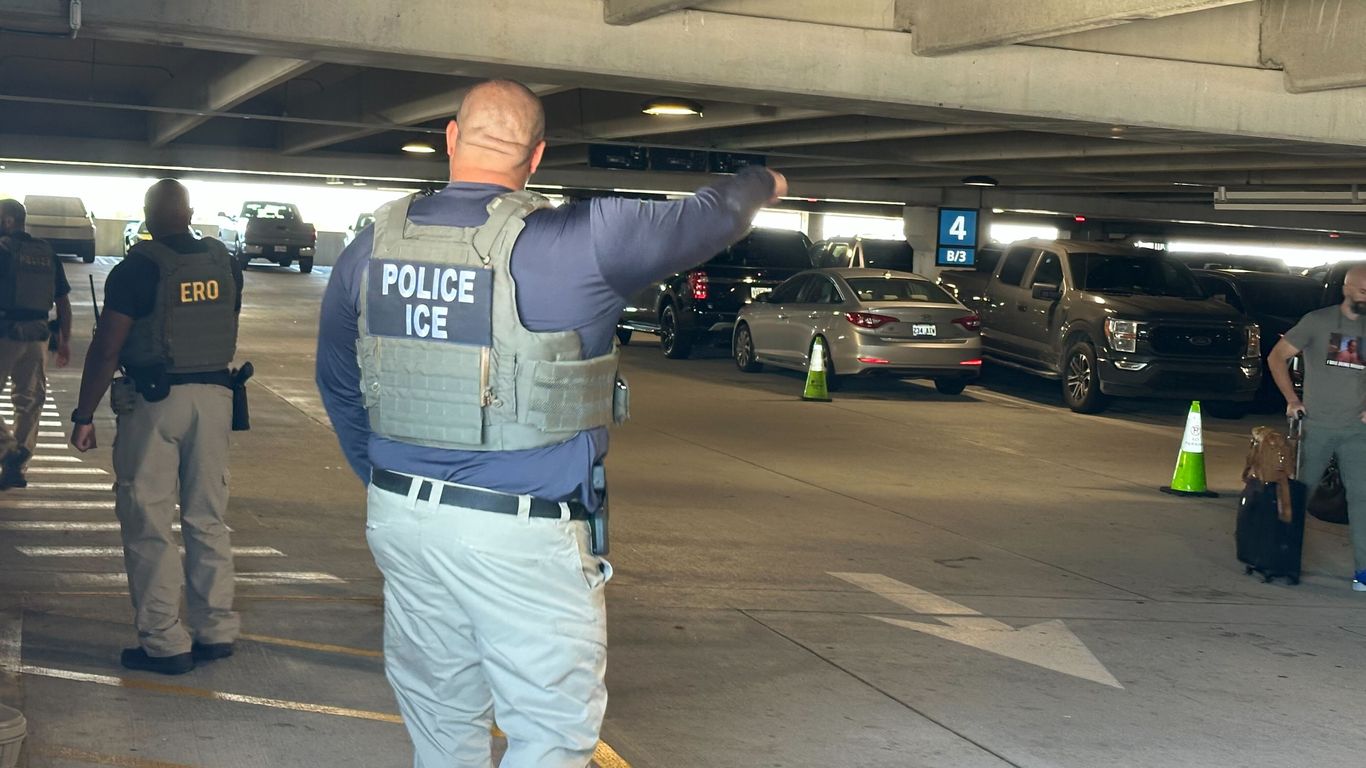

More than 40% of TSA agents at Louis Armstrong New Orleans International Airport called out sick amid a partial federal shutdown, prompting ICE deployments to assist checkpoint operations and causing multi-hour security-line backups. Separately, New Orleans faces a near-term fiscal squeeze — city officials warn it could run out of cash as early as next month, with last-resort options including tapping a $35M rainy-day fund, taking additional emergency loans, and expanding furloughs/layoffs; disputed SWBNO repair cost estimates and a recent water-main break add operational and political risk.

This episode is a microcosm of a larger fragility: when frontline public services run unpaid or underfunded, marginal interventions (temporary DHS deployments, emergency contractors) create asymmetric winners — defense/government contractors and screening-equipment vendors — and concentrated losers: local service-providers, hospitality and night/weekend cash flows at affected airports, and the municipal treasury. If similar staffing shocks spread beyond a handful of hubs over a multi-week window, expect systemic operational disruptions that amplify airline unit revenue volatility (a plausible 3–7% hit to near-term passenger revenue if >10 major airports see sustained disruptions), not because demand collapses but because realized capacity and on-time performance deteriorate.

On the municipal side, the water-infrastructure and liquidity squeeze creates a short-to-intermediate creditcycle stress event: constrained operating cash + near-term loan amortizations make New Orleans a candidate for near-term credit-negative headlines, special assessments or emergency borrowings, and potentially concessions to state oversight that reprice political risk for local credits. That dynamic compresses local liquidity and pushes procurement into stop-start mode — good for large engineering contractors with balance sheets (multi-year backlog optionality), bad for small suppliers and for long-duration muni holders concentrated in the area.

Timing and catalysts to watch: (1) TSA staffing metrics and national sickout breadth over the next 7–21 days (binary catalyst for airlines), (2) City Council votes or state-level intervention and any loan draws in the next 30–90 days (catalyst for muni spreads), and (3) announcements of federal emergency funding or DHS procurement of screening tech over 3–12 months (catalyst for contractors/suppliers). The tradeable edge is asymmetry — short-duration, event-driven plays around airlines and muni credit stress versus option-like, multi-quarter exposure to screening/engineering contractors that are likely to capture delayed but larger spend.

AI-powered research, real-time alerts, and portfolio analytics for institutional investors.

Request DemoOverall Sentiment

mildly negative

Sentiment Score

-0.35